Hard currency refers to a stable and widely accepted currency with strong international demand, such as the US dollar, euro, or Japanese yen. Soft currency lacks stability and is prone to depreciation, often used within a limited local market and subject to high inflation or government controls. Discover more about how these currency categories impact global trade and investment strategies.

Main Difference

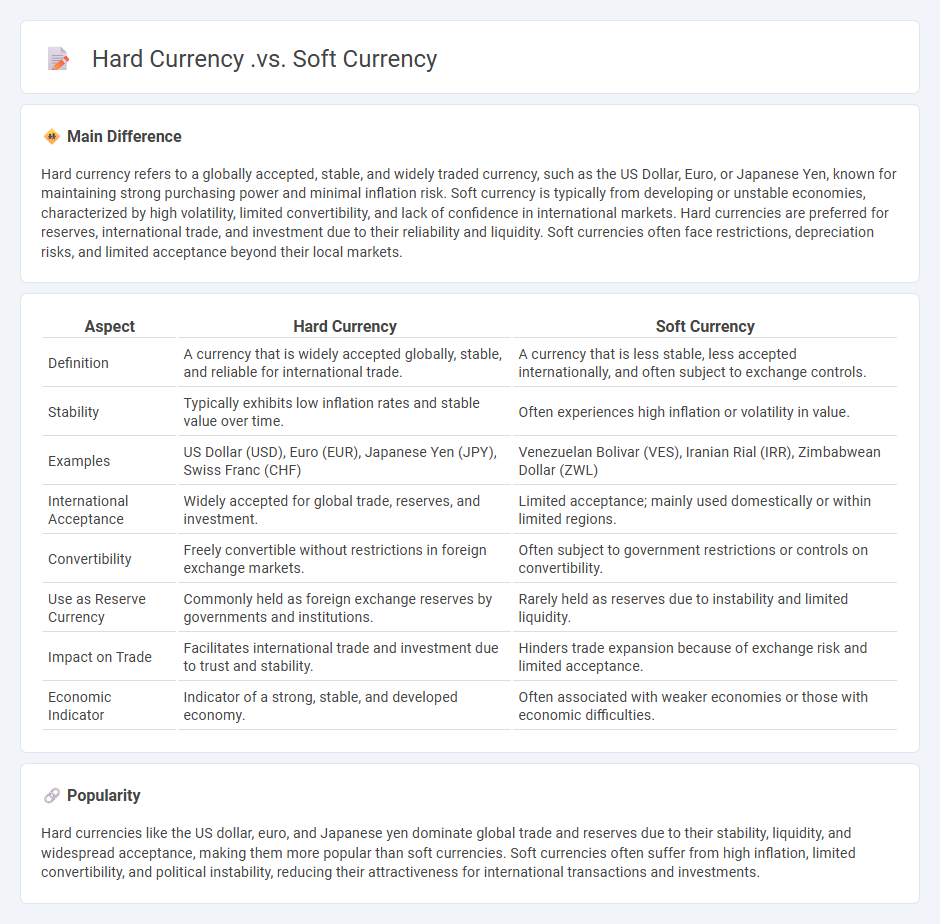

Hard currency refers to a globally accepted, stable, and widely traded currency, such as the US Dollar, Euro, or Japanese Yen, known for maintaining strong purchasing power and minimal inflation risk. Soft currency is typically from developing or unstable economies, characterized by high volatility, limited convertibility, and lack of confidence in international markets. Hard currencies are preferred for reserves, international trade, and investment due to their reliability and liquidity. Soft currencies often face restrictions, depreciation risks, and limited acceptance beyond their local markets.

Connection

Hard currency, characterized by stability and wide acceptability in global markets, directly influences the exchange rates of soft currency, which is often less stable and subject to higher volatility. Investors tend to prefer holding hard currencies like the US dollar, euro, or Japanese yen, leading to increased demand and stronger valuation compared to soft currencies from emerging or developing economies. This dynamic creates a dependency where fluctuations in hard currency markets can significantly affect the liquidity and exchange policies of soft currencies.

Comparison Table

| Aspect | Hard Currency | Soft Currency |

|---|---|---|

| Definition | A currency that is widely accepted globally, stable, and reliable for international trade. | A currency that is less stable, less accepted internationally, and often subject to exchange controls. |

| Stability | Typically exhibits low inflation rates and stable value over time. | Often experiences high inflation or volatility in value. |

| Examples | US Dollar (USD), Euro (EUR), Japanese Yen (JPY), Swiss Franc (CHF) | Venezuelan Bolivar (VES), Iranian Rial (IRR), Zimbabwean Dollar (ZWL) |

| International Acceptance | Widely accepted for global trade, reserves, and investment. | Limited acceptance; mainly used domestically or within limited regions. |

| Convertibility | Freely convertible without restrictions in foreign exchange markets. | Often subject to government restrictions or controls on convertibility. |

| Use as Reserve Currency | Commonly held as foreign exchange reserves by governments and institutions. | Rarely held as reserves due to instability and limited liquidity. |

| Impact on Trade | Facilitates international trade and investment due to trust and stability. | Hinders trade expansion because of exchange risk and limited acceptance. |

| Economic Indicator | Indicator of a strong, stable, and developed economy. | Often associated with weaker economies or those with economic difficulties. |

Exchange Rate Stability

Exchange rate stability refers to maintaining consistent currency value relative to others, minimizing volatility that disrupts international trade and investment. Central banks often intervene in foreign exchange markets and implement monetary policies to keep exchange rates within targeted bands. Stable exchange rates encourage investor confidence, reduce transaction costs, and promote economic growth by facilitating predictable import and export pricing. Countries like Switzerland and Singapore have historically prioritized exchange rate stability to support their open economies and financial sectors.

Global Acceptability

Global acceptability in finance refers to the widespread recognition and use of financial instruments, currencies, and payment methods across international markets. The US dollar remains the most globally accepted currency, facilitating trade, investment, and foreign exchange reserves in over 80% of global transactions. International credit cards like Visa and MasterCard are accepted in more than 200 countries, enabling seamless cross-border payments. Financial technologies such as SWIFT and blockchain platforms enhance the global interoperability and trust of financial systems.

Inflation Resistance

Inflation resistance in finance refers to the ability of an asset or investment to maintain or increase its value during periods of rising inflation. Real assets such as real estate, commodities, and Treasury Inflation-Protected Securities (TIPS) commonly exhibit strong inflation resistance due to their intrinsic value or inflation-linked returns. Stocks of companies with pricing power and essential goods often outperform during inflationary periods as they can pass increased costs to consumers. Diversified portfolios that include inflation-resistant assets help investors preserve purchasing power and mitigate erosion of real returns.

Economic Confidence

Economic confidence reflects consumer and investor sentiment about the overall health and future prospects of the economy. Key indicators include the Consumer Confidence Index (CCI) and the Economic Sentiment Indicator (ESI), which track optimism on employment, income, and market stability. High economic confidence typically correlates with increased spending, investment, and economic growth, while low confidence may indicate potential downturns or recessions. Policymakers and financial analysts closely monitor these metrics to gauge economic momentum and guide fiscal or monetary interventions.

Convertibility

Convertibility in finance refers to the ability to exchange one currency or financial instrument for another without restrictions. It is a key characteristic of freely traded currencies in the foreign exchange market, impacting global trade and investment flows. Full convertibility allows investors and businesses to move capital across borders with minimal regulatory barriers, enhancing liquidity and market efficiency. Countries with partially or non-convertible currencies often impose controls to manage exchange rates and protect their economies from volatile capital movements.

Source and External Links

Hard Currency and Soft Currency| Meaning and Example - Hard currency is stable, widely accepted globally, and from economically secure countries, while soft currency is volatile, less accepted worldwide, and from less stable economies.

Hard Currency - Overview, Factors, Examples, Comparison - Hard currency is reliable, globally traded, and issued by developed nations, whereas soft currency is unstable, less convertible, and mostly used domestically.

Hard currency - Hard currencies act as a stable store of value during crises and are preferred for international transactions, while soft currencies are subject to rapid depreciation and often restricted by capital controls.

FAQs

What is a hard currency?

A hard currency is a globally accepted, stable, and reliable currency used in international trade and finance, such as the US dollar, euro, or Japanese yen.

What is a soft currency?

A soft currency is a currency that is not widely accepted for international trade and is subject to exchange rate instability and government restrictions.

How does hard currency differ from soft currency?

Hard currency is a globally accepted, stable, and widely traded currency such as the US dollar or euro, whereas soft currency is less stable, less widely accepted, and subject to exchange restrictions and depreciation.

Which countries use hard currencies?

Countries using hard currencies include the United States (US Dollar), Eurozone nations (Euro), Japan (Japanese Yen), United Kingdom (British Pound Sterling), Switzerland (Swiss Franc), Canada (Canadian Dollar), Australia (Australian Dollar), and Singapore (Singapore Dollar).

What causes a currency to be considered soft?

A currency is considered soft when it lacks global acceptance, experiences high volatility, faces limited convertibility, and is subject to government restrictions or economic instability.

Why do investors prefer hard currency?

Investors prefer hard currency because it maintains stable value, offers high liquidity, and is widely accepted internationally, reducing exchange rate risk and economic uncertainty.

How do exchange rates affect hard and soft currencies?

Exchange rates influence hard currencies by determining their global purchasing power and stability, while soft currencies experience greater volatility and reduced international acceptance due to fluctuating exchange rates.