Callable bonds grant issuers the right to redeem the bond before maturity, often at a premium, allowing them to refinance debt if interest rates drop. Putable bonds give investors the option to sell the bond back to the issuer before maturity, providing protection against rising interest rates or credit deterioration. Explore the detailed differences and strategic uses of callable and putable bonds to optimize your fixed-income portfolio.

Main Difference

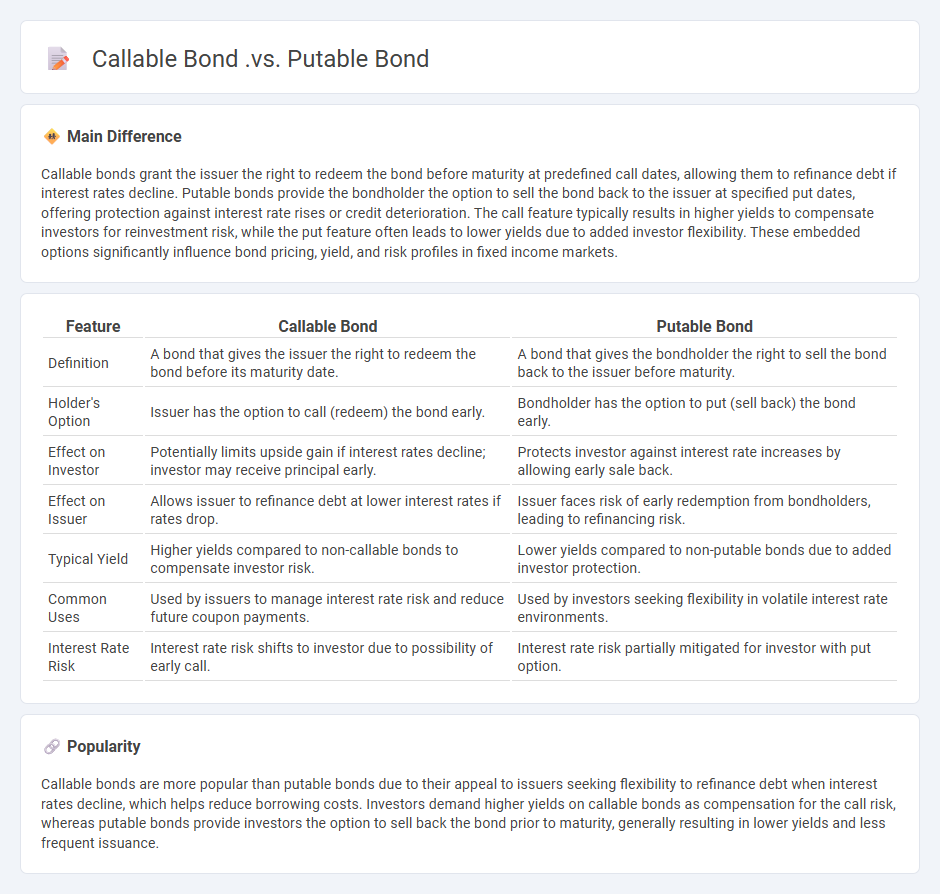

Callable bonds grant the issuer the right to redeem the bond before maturity at predefined call dates, allowing them to refinance debt if interest rates decline. Putable bonds provide the bondholder the option to sell the bond back to the issuer at specified put dates, offering protection against interest rate rises or credit deterioration. The call feature typically results in higher yields to compensate investors for reinvestment risk, while the put feature often leads to lower yields due to added investor flexibility. These embedded options significantly influence bond pricing, yield, and risk profiles in fixed income markets.

Connection

Callable bonds and putable bonds share the feature of embedded options that provide flexibility to issuers or investors; callable bonds grant issuers the right to redeem before maturity, while putable bonds allow investors to sell back to the issuer. These options affect the bond's pricing, yield, and risk profile by influencing expected cash flows and interest rate sensitivity. Understanding the interplay of call and put options is crucial for accurate valuation and investment strategy in fixed income markets.

Comparison Table

| Feature | Callable Bond | Putable Bond |

|---|---|---|

| Definition | A bond that gives the issuer the right to redeem the bond before its maturity date. | A bond that gives the bondholder the right to sell the bond back to the issuer before maturity. |

| Holder's Option | Issuer has the option to call (redeem) the bond early. | Bondholder has the option to put (sell back) the bond early. |

| Effect on Investor | Potentially limits upside gain if interest rates decline; investor may receive principal early. | Protects investor against interest rate increases by allowing early sale back. |

| Effect on Issuer | Allows issuer to refinance debt at lower interest rates if rates drop. | Issuer faces risk of early redemption from bondholders, leading to refinancing risk. |

| Typical Yield | Higher yields compared to non-callable bonds to compensate investor risk. | Lower yields compared to non-putable bonds due to added investor protection. |

| Common Uses | Used by issuers to manage interest rate risk and reduce future coupon payments. | Used by investors seeking flexibility in volatile interest rate environments. |

| Interest Rate Risk | Interest rate risk shifts to investor due to possibility of early call. | Interest rate risk partially mitigated for investor with put option. |

Callable Bond

Callable bonds allow issuers to redeem the bond before its maturity date, often at a predetermined call price. These bonds typically offer higher yields to compensate investors for the call risk, which is the risk of the bond being called away when interest rates decline. Call provisions benefit issuers by providing flexibility to refinance debt at lower rates, but they create uncertainty for investors regarding the bond's cash flows. The call feature's valuation requires adjusting the bond's price to reflect potential early redemption, influencing investment strategies in fixed-income portfolios.

Putable Bond

A putable bond is a type of bond that grants the holder the right to force the issuer to repurchase the bond before its maturity date at a predetermined price. This feature protects investors against rising interest rates and credit deterioration by providing liquidity and reducing interest rate risk. The put option increases the bond's value, often resulting in a lower yield compared to non-putable bonds. Putable bonds are commonly issued by corporations and governments seeking to attract risk-averse investors.

Early Redemption

Early redemption allows bondholders or borrowers to repay a debt before its scheduled maturity date, often subject to specific terms and conditions outlined in the bond indenture or loan agreement. This practice can mitigate interest expenses for issuers during declining interest rate environments or provide liquidity advantages for investors. Commonly associated with callable bonds, early redemption features may include a premium payment, known as a call premium, to compensate the lender for the early termination of the agreement. Regulatory frameworks from entities such as the U.S. Securities and Exchange Commission (SEC) govern disclosure requirements related to early redemption terms.

Investor Protection

Investor protection encompasses legal frameworks and regulatory measures designed to safeguard investors from fraud, misrepresentation, and malpractice in financial markets. Key entities involved include the Securities and Exchange Commission (SEC) in the United States and the Financial Conduct Authority (FCA) in the UK, which enforce transparency and fair trading practices. Investor protection mechanisms such as disclosure requirements, mandatory auditing, and fiduciary responsibilities help maintain market integrity and boost investor confidence. Effective protection reduces systemic risk and promotes capital formation by ensuring equitable market participation.

Interest Rate Risk

Interest rate risk in finance refers to the potential for investment losses due to fluctuations in interest rates. This risk primarily affects fixed-income securities such as bonds, where rising interest rates lead to falling bond prices. Financial institutions manage this risk through strategies like duration matching and interest rate swaps. Understanding the impact of central bank policies on market interest rates is critical for effective risk management.

Source and External Links

Callable and Puttable Bonds: Meaning and Advantages - This webpage compares callable bonds, which allow issuers to redeem early, with puttable bonds, which grant bondholders the same option, highlighting differences in redemption rights and interest rates.

Callable and Putable Bonds - This document explains that callable bonds offer issuers flexibility to repay early, often to refinance at lower rates, while puttable bonds provide bondholders with liquidity options.

Putable Bond | Definition + Examples - This webpage defines puttable bonds as giving bondholders the option to force early repayment, contrasting with callable bonds where issuers have this option.

FAQs

What is a bond?

A bond is a fixed-income financial instrument representing a loan made by an investor to a borrower, typically corporate or governmental, with a defined interest rate and maturity date.

What is a callable bond?

A callable bond is a debt security that allows the issuer to redeem the bond before its maturity date at a specified call price.

What is a putable bond?

A putable bond is a fixed-income security that grants the bondholder the right to sell the bond back to the issuer at a predetermined price before maturity.

How does a callable bond work?

A callable bond allows the issuer to repay the principal before maturity at a predetermined call price, typically after a specified call protection period, enabling the issuer to refinance debt if interest rates decline.

How does a putable bond work?

A putable bond allows the bondholder to sell the bond back to the issuer at a specified price before maturity, providing protection against interest rate increases or issuer credit deterioration.

What are the main differences between callable and putable bonds?

Callable bonds allow issuers to redeem them before maturity, limiting upside for investors, while putable bonds give holders the right to sell back to the issuer early, offering downside protection.

Why do investors choose callable or putable bonds?

Investors choose callable bonds to potentially benefit from higher yields as compensation for issuer call risk and choose putable bonds to gain the option to sell the bond back to the issuer early, reducing interest rate and credit risk.