Ramsey taxation aims to minimize economic distortions by optimally setting tax rates based on consumers' price elasticities, promoting efficiency in revenue generation. Lump-sum taxation involves fixed taxes unrelated to economic behavior, ensuring equity and simplicity but potentially disregarding income distribution fairness. Explore how these contrasting approaches impact fiscal policy and economic welfare.

Main Difference

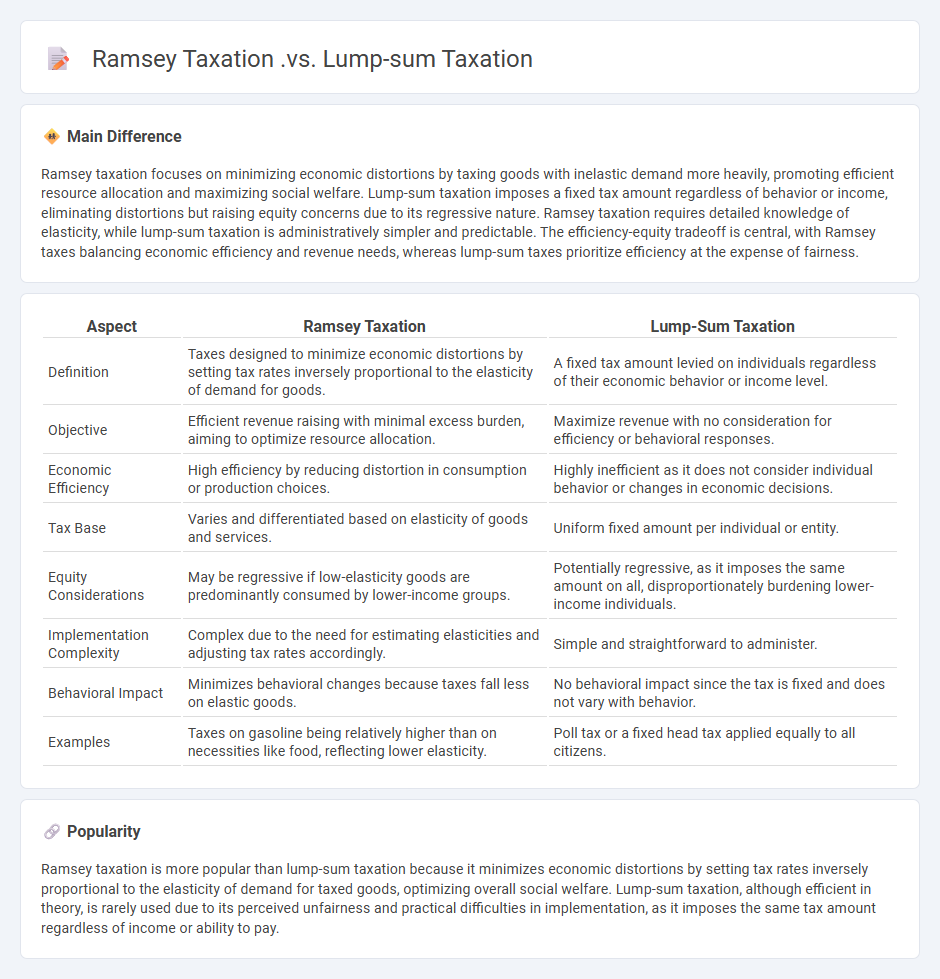

Ramsey taxation focuses on minimizing economic distortions by taxing goods with inelastic demand more heavily, promoting efficient resource allocation and maximizing social welfare. Lump-sum taxation imposes a fixed tax amount regardless of behavior or income, eliminating distortions but raising equity concerns due to its regressive nature. Ramsey taxation requires detailed knowledge of elasticity, while lump-sum taxation is administratively simpler and predictable. The efficiency-equity tradeoff is central, with Ramsey taxes balancing economic efficiency and revenue needs, whereas lump-sum taxes prioritize efficiency at the expense of fairness.

Connection

Ramsey taxation aims to minimize excess burdens by setting optimal commodity tax rates based on elasticities of demand, producing efficient resource allocation. Lump-sum taxation, in contrast, provides a non-distortionary revenue source since it does not influence individual behavior or market decisions. Combining Ramsey taxation principles with lump-sum taxes can achieve revenue goals while minimizing economic distortions and efficiency losses.

Comparison Table

| Aspect | Ramsey Taxation | Lump-Sum Taxation |

|---|---|---|

| Definition | Taxes designed to minimize economic distortions by setting tax rates inversely proportional to the elasticity of demand for goods. | A fixed tax amount levied on individuals regardless of their economic behavior or income level. |

| Objective | Efficient revenue raising with minimal excess burden, aiming to optimize resource allocation. | Maximize revenue with no consideration for efficiency or behavioral responses. |

| Economic Efficiency | High efficiency by reducing distortion in consumption or production choices. | Highly inefficient as it does not consider individual behavior or changes in economic decisions. |

| Tax Base | Varies and differentiated based on elasticity of goods and services. | Uniform fixed amount per individual or entity. |

| Equity Considerations | May be regressive if low-elasticity goods are predominantly consumed by lower-income groups. | Potentially regressive, as it imposes the same amount on all, disproportionately burdening lower-income individuals. |

| Implementation Complexity | Complex due to the need for estimating elasticities and adjusting tax rates accordingly. | Simple and straightforward to administer. |

| Behavioral Impact | Minimizes behavioral changes because taxes fall less on elastic goods. | No behavioral impact since the tax is fixed and does not vary with behavior. |

| Examples | Taxes on gasoline being relatively higher than on necessities like food, reflecting lower elasticity. | Poll tax or a fixed head tax applied equally to all citizens. |

Efficiency

Efficiency in economics measures how well resources are utilized to maximize output and satisfy needs with minimal waste. It encompasses allocative efficiency, where resources are distributed to produce the most valued goods and services, and productive efficiency, which occurs when goods are produced at the lowest possible cost. Technical efficiency highlights the use of the best production methods and technology, while dynamic efficiency focuses on innovation and adaptability over time. Understanding these concepts aids policymakers and businesses in optimizing economic performance and growth.

Equity

Equity in economics refers to the fairness and justice in the distribution of wealth, income, and resources across society. It emphasizes reducing disparities by implementing progressive taxation, social welfare programs, and equal access to education and healthcare. Economic equity aims to balance opportunities so individuals can achieve similar outcomes regardless of their starting position. Policymakers often measure equity using indicators such as the Gini coefficient and poverty rates to guide redistributive strategies.

Distortionary Taxes

Distortionary taxes alter economic behavior by changing relative prices, leading to inefficiencies in resource allocation. These taxes, such as income taxes and sales taxes, can reduce labor supply, savings, and investment by distorting individuals' and firms' decisions. Empirical studies show that high marginal tax rates often decrease work incentives and economic growth. Optimal tax theory seeks to balance revenue needs with minimizing distortions to maximize social welfare.

Marginal Rates

Marginal rates in economics measure the change in one variable relative to a change in another, providing critical insights into decision-making processes and resource allocation. Marginal cost quantifies the expense incurred by producing one additional unit of a good, while marginal revenue represents the additional income from selling that extra unit. Understanding marginal rates enables firms to determine optimal production levels to maximize profit by equating marginal cost and marginal revenue. These concepts are fundamental in microeconomic theory, influencing pricing strategies and competitive market behavior.

Revenue Neutrality

Revenue neutrality in economics refers to a fiscal policy approach where changes in taxation are offset by adjustments in other taxes or government spending to maintain the overall revenue level. This principle ensures that tax reforms, such as introducing a carbon tax, do not increase or decrease total government revenue, supporting economic stability. Governments use revenue-neutral policies to encourage specific behaviors, like reducing carbon emissions, without expanding budget deficits or triggering inflation. Effective implementation requires accurate forecasting and balanced adjustments to avoid unintended economic consequences.

Source and External Links

An Inverse-Ramsey Tax Rule - Ramsey taxation involves distortionary commodity taxes that create excess burden and thus a utility loss greater than lump-sum taxes, which have no excess burden and impose the same cost regardless of behavior, making lump-sum taxation generally more efficient if feasible.

Lecture 1: Ramsey Theory - Ramsey taxation relies on linear taxes and assumes a population of identical agents, ruling out lump-sum taxes because they are often considered unfair; lump-sum taxes charge the same amount regardless of income or behavior, thus avoiding economic distortions but raising equity concerns.

In Praise of Frank Ramsey's Contribution to the Theory of Optimal Taxation - Ramsey taxation minimizes distortion by taxing goods with low price elasticities more heavily but can lead to regressive outcomes, whereas lump-sum taxes generate no deadweight loss and are ideal if everyone were identical; however, lump-sum taxes are often replaced due to equity concerns and feasibility constraints.

FAQs

What is taxation in economics?

Taxation in economics is the compulsory financial charge imposed by governments on individuals or entities to fund public expenditures and redistribute resources.

What is Ramsey taxation?

Ramsey taxation is an economic principle that advocates levying taxes on goods with inelastic demand to minimize overall welfare loss while raising necessary government revenue.

What is lump-sum taxation?

Lump-sum taxation is a fixed tax amount imposed uniformly on all individuals regardless of income or economic behavior.

How do Ramsey taxes differ from lump-sum taxes?

Ramsey taxes minimize social welfare loss by taxing goods with inelastic demand, while lump-sum taxes impose a fixed amount regardless of behavior, causing no distortion but potentially less equity.

What are the advantages of Ramsey taxation?

Ramsey taxation minimizes economic distortions by taxing goods with inelastic demand, increases overall welfare by optimizing tax efficiency, and maximizes government revenue while reducing excess burden on consumers and producers.

What are the limitations of lump-sum taxation?

Lump-sum taxation is limited by its perceived unfairness as it imposes the same tax amount on all individuals regardless of income, lacks flexibility to address income disparities, cannot be adjusted for changes in taxpayers' ability to pay, and may reduce political feasibility due to public opposition.

Why do economists compare Ramsey and lump-sum taxation?

Economists compare Ramsey and lump-sum taxation to evaluate efficiency trade-offs, where Ramsey taxation minimizes deadweight loss by distorting taxes optimally, while lump-sum taxation achieves equity without economic distortions but is often impractical due to information constraints.