The Capital Asset Pricing Model (CAPM) and Arbitrage Pricing Theory (APT) are foundational frameworks in financial economics for asset pricing and risk assessment. CAPM emphasizes a single-factor approach based on market risk, while APT incorporates multiple macroeconomic factors to explain asset returns more comprehensively. Explore the key differences and practical applications of CAPM and APT to enhance investment strategies.

Main Difference

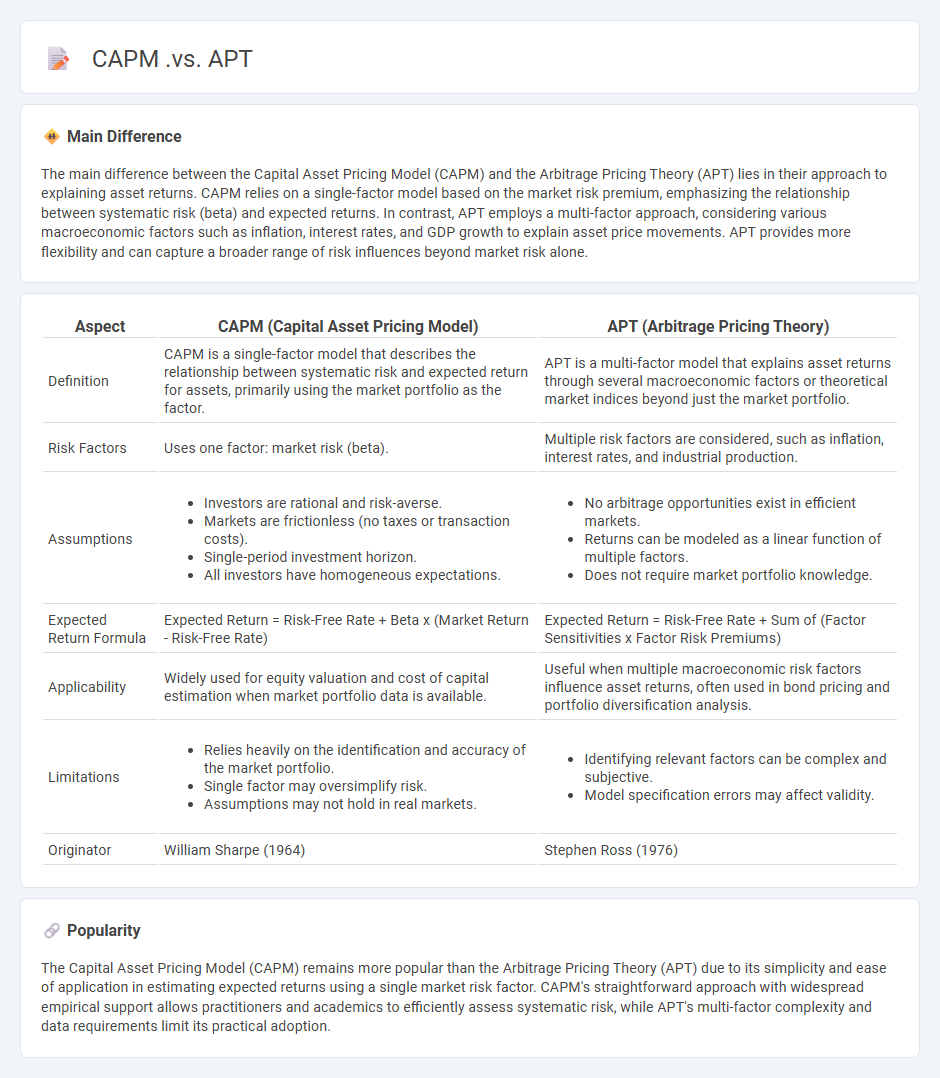

The main difference between the Capital Asset Pricing Model (CAPM) and the Arbitrage Pricing Theory (APT) lies in their approach to explaining asset returns. CAPM relies on a single-factor model based on the market risk premium, emphasizing the relationship between systematic risk (beta) and expected returns. In contrast, APT employs a multi-factor approach, considering various macroeconomic factors such as inflation, interest rates, and GDP growth to explain asset price movements. APT provides more flexibility and can capture a broader range of risk influences beyond market risk alone.

Connection

The Capital Asset Pricing Model (CAPM) and Arbitrage Pricing Theory (APT) both explain asset returns through risk factors, but CAPM relies on a single market risk factor while APT incorporates multiple macroeconomic risk factors. Both models assume investors are rational and markets are efficient, yet APT provides more flexibility by allowing various sources of systematic risk beyond just market risk. Empirical testing often shows APT's multifactor approach captures asset return variations better than CAPM's single-factor framework.

Comparison Table

| Aspect | CAPM (Capital Asset Pricing Model) | APT (Arbitrage Pricing Theory) |

|---|---|---|

| Definition | CAPM is a single-factor model that describes the relationship between systematic risk and expected return for assets, primarily using the market portfolio as the factor. | APT is a multi-factor model that explains asset returns through several macroeconomic factors or theoretical market indices beyond just the market portfolio. |

| Risk Factors | Uses one factor: market risk (beta). | Multiple risk factors are considered, such as inflation, interest rates, and industrial production. |

| Assumptions |

|

|

| Expected Return Formula | Expected Return = Risk-Free Rate + Beta x (Market Return - Risk-Free Rate) | Expected Return = Risk-Free Rate + Sum of (Factor Sensitivities x Factor Risk Premiums) |

| Applicability | Widely used for equity valuation and cost of capital estimation when market portfolio data is available. | Useful when multiple macroeconomic risk factors influence asset returns, often used in bond pricing and portfolio diversification analysis. |

| Limitations |

|

|

| Originator | William Sharpe (1964) | Stephen Ross (1976) |

Risk Factors

Risk factors in finance encompass market volatility, credit risk, liquidity risk, and operational risk that impact investment returns and business stability. Market volatility refers to fluctuations in asset prices influenced by economic indicators, geopolitical events, and investor sentiment. Credit risk involves the possibility of a borrower defaulting on debt obligations, assessed through credit ratings and financial health analysis. Liquidity risk arises when assets cannot be quickly converted to cash without significant value loss, often affecting trading strategies and capital adequacy.

Market Portfolio

The market portfolio in finance represents a theoretical portfolio consisting of all available assets weighted by their market capitalizations, capturing the entire investable market. It serves as a benchmark for evaluating the performance and risk of individual securities under the Capital Asset Pricing Model (CAPM). Empirical approximations of the market portfolio often use broad-based indices like the MSCI World Index or the S&P 500. Investors assume that diversification within the market portfolio minimizes unsystematic risk, leaving only systematic risk relevant for pricing assets.

Arbitrage Opportunities

Arbitrage opportunities in finance refer to the practice of exploiting price discrepancies of identical or similar financial instruments across different markets to achieve risk-free profits. These opportunities arise due to market inefficiencies and can exist in various asset classes including stocks, bonds, currencies, and commodities. Advanced algorithms and high-frequency trading systems are commonly used to identify and execute arbitrage strategies rapidly, minimizing the risk of detection and market correction. Despite their potential for profit, arbitrage opportunities tend to be short-lived as market forces quickly restore price equilibrium.

Systematic Risk

Systematic risk, often referred to as market risk, encompasses the inherent uncertainties affecting the entire financial market or a broad segment, driven by macroeconomic factors such as interest rate changes, inflation, recessions, and geopolitical events. Unlike unsystematic risk, which impacts individual stocks or sectors, systematic risk cannot be eliminated through diversification. Key indicators include the beta coefficient, measuring a security's sensitivity to market movements, and the Capital Asset Pricing Model (CAPM), which quantifies expected return relative to systematic risk. Investors and portfolio managers must account for systematic risk to optimize asset allocation and risk management strategies in equity, bond, and derivative markets.

Model Assumptions

Model assumptions in finance establish the foundational premises for constructing mathematical models that forecast market behavior, asset prices, or risk management outcomes. Common assumptions include market efficiency, rational investor behavior, and normally distributed returns, which simplify complex financial realities for analytical tractability. These assumptions influence model accuracy and applicability, impacting valuation methods, portfolio optimization, and derivative pricing. Understanding their limitations is crucial for interpreting model outputs and adjusting strategies in fluctuating market conditions.

Source and External Links

Comparison Of Capm And Apt - CAPM uses a single factor (market risk) to estimate expected returns, while APT considers multiple macroeconomic factors, making it more nuanced and applicable to diversified portfolios with fewer assumptions about market efficiency.

Arbitrage Price Theory vs. Capital Asset Pricing - CAPM relies on one beta and assumes a linear relationship with market risk, whereas APT uses several factors with corresponding betas but requires users to identify relevant risk factors themselves, making APT more complex but potentially more accurate in medium to long term contexts.

CAPM vs APT. Which One Is Right for You? - APT extends CAPM by incorporating multiple factors affecting asset returns rather than just market sensitivity, making APT more flexible and accurate when additional factors explain returns, while CAPM remains simpler with a focus on market beta.

FAQs

What is the CAPM?

The Capital Asset Pricing Model (CAPM) is a financial model that calculates the expected return of an asset based on its systematic risk, measured by beta, the risk-free rate, and the expected market return.

What is the APT?

An APT (Advanced Persistent Threat) is a prolonged and targeted cyberattack in which an intruder gains unauthorized access to a network to steal data or surveil systems while remaining undetected.

How does CAPM differ from APT?

CAPM uses a single market risk factor to explain asset returns, assuming a linear relationship between expected return and beta, while APT employs multiple factors to capture various systematic risks without specifying exact factors, offering more flexibility in modeling asset returns.

What are the main assumptions of CAPM?

The main assumptions of CAPM are investors are rational and risk-averse, markets are frictionless with no taxes or transaction costs, all investors have homogeneous expectations, there is a single-period investment horizon, assets are infinitely divisible, investors can borrow and lend at a risk-free rate, and all investors hold diversified portfolios on the efficient frontier.

What are the main assumptions of APT?

The main assumptions of the Arbitrage Pricing Theory (APT) are: asset returns are influenced by multiple systematic risk factors, investors hold diversified portfolios eliminating unsystematic risk, arbitrage opportunities are quickly exploited eliminating mispricings, and the relationship between asset returns and factors is linear.

When should APT be used instead of CAPM?

APT should be used instead of CAPM when multiple macroeconomic factors impact asset returns, offering a more flexible and multifactor approach to risk assessment compared to CAPM's single market beta model.

What are the limitations of CAPM and APT?

CAPM assumes a single market factor and market efficiency, ignoring multiple risk sources and market anomalies; APT requires multiple factors but lacks a standardized set, making factor selection subjective and model implementation complex.