A Pay-in-Kind (PIK) Security allows issuers to defer interest payments by issuing additional securities instead of cash, often used in high-yield financing to preserve liquidity. Payment-in-Kind Loans operate similarly by permitting borrowers to pay interest with additional debt rather than cash, frequently utilized in leveraged buyouts and growth capital scenarios. Explore the nuances and strategic implications of Pay-in-Kind financing options to make informed investment decisions.

Main Difference

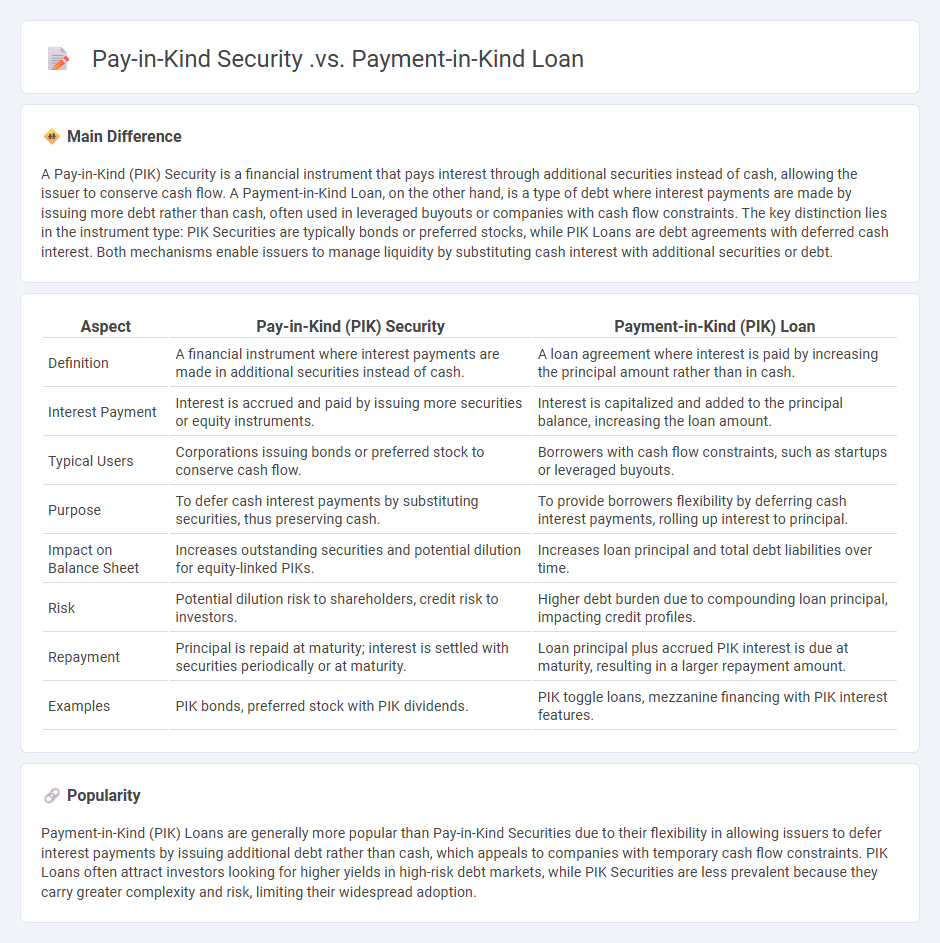

A Pay-in-Kind (PIK) Security is a financial instrument that pays interest through additional securities instead of cash, allowing the issuer to conserve cash flow. A Payment-in-Kind Loan, on the other hand, is a type of debt where interest payments are made by issuing more debt rather than cash, often used in leveraged buyouts or companies with cash flow constraints. The key distinction lies in the instrument type: PIK Securities are typically bonds or preferred stocks, while PIK Loans are debt agreements with deferred cash interest. Both mechanisms enable issuers to manage liquidity by substituting cash interest with additional securities or debt.

Connection

Pay-in-Kind (PIK) securities and Payment-in-Kind loans are interconnected financial instruments where interest or dividends are paid not in cash but by issuing additional securities or increasing the principal amount. PIK loans allow borrowers to conserve cash flow by delaying cash interest payments, while investors receive compensation through accrued interest added to the loan balance. This structure aligns the interests of lenders and borrowers in situations of cash-flow constraints, often seen in leveraged buyouts and restructuring scenarios.

Comparison Table

| Aspect | Pay-in-Kind (PIK) Security | Payment-in-Kind (PIK) Loan |

|---|---|---|

| Definition | A financial instrument where interest payments are made in additional securities instead of cash. | A loan agreement where interest is paid by increasing the principal amount rather than in cash. |

| Interest Payment | Interest is accrued and paid by issuing more securities or equity instruments. | Interest is capitalized and added to the principal balance, increasing the loan amount. |

| Typical Users | Corporations issuing bonds or preferred stock to conserve cash flow. | Borrowers with cash flow constraints, such as startups or leveraged buyouts. |

| Purpose | To defer cash interest payments by substituting securities, thus preserving cash. | To provide borrowers flexibility by deferring cash interest payments, rolling up interest to principal. |

| Impact on Balance Sheet | Increases outstanding securities and potential dilution for equity-linked PIKs. | Increases loan principal and total debt liabilities over time. |

| Risk | Potential dilution risk to shareholders, credit risk to investors. | Higher debt burden due to compounding loan principal, impacting credit profiles. |

| Repayment | Principal is repaid at maturity; interest is settled with securities periodically or at maturity. | Loan principal plus accrued PIK interest is due at maturity, resulting in a larger repayment amount. |

| Examples | PIK bonds, preferred stock with PIK dividends. | PIK toggle loans, mezzanine financing with PIK interest features. |

Interest Payment Structure

Interest payment structure in finance defines the schedule and manner in which interest on a loan or investment is paid. Common structures include fixed-rate payments, where interest remains constant over the loan term, and variable or floating rates, which adjust based on benchmark indices like LIBOR or SOFR. Amortizing loans require periodic payments covering both principal and interest, while bullet loans delay principal repayment until maturity, paying interest periodically. Understanding the payment structure is critical for assessing cash flow impact and total cost of borrowing.

Debt Instrument Type

Debt instruments are financial tools used by entities to raise capital through borrowing, exemplified by bonds, debentures, notes, and commercial paper. These instruments represent a contractual obligation where the issuer promises to repay the principal along with interest on specified dates, often serving as a critical source of funding for governments, corporations, and financial institutions. The terms of debt instruments vary, including fixed or floating interest rates, maturity dates, and collateral backing, which influence their risk profile and market value. Investors utilize these instruments to generate steady income streams while assessing credit risk and market conditions impacting prices and yields.

Maturity and Repayment

Loan maturity defines the period from issuance until the principal amount must be fully repaid, often ranging from short-term (less than one year) to long-term (over ten years). Repayment schedules vary based on loan type, including amortized payments, interest-only periods, or bullet repayments, directly impacting cash flow management. Fixed maturity loans provide predictable end dates for financial planning, while revolving credit facilities offer flexible repayment options without a set maturity. Understanding maturity and repayment terms is critical for managing debt obligations and optimizing capital structure in corporate finance.

Risk Profile

A risk profile in finance evaluates an investor's willingness and ability to endure potential losses in their investment portfolio. It considers factors such as age, financial goals, investment timeframe, and income stability to categorize investors into conservative, moderate, or aggressive risk tolerance levels. Financial advisors use risk profiles to tailor asset allocation strategies, balancing equities, fixed income, and alternative investments accordingly. Accurate risk profiling enhances portfolio resilience and aligns investment decisions with individual financial objectives.

Investor Considerations

Investors prioritize risk assessment, return on investment, and market conditions when making financial decisions. Portfolio diversification and asset allocation strategies are critical to managing volatility and achieving long-term growth. Understanding regulatory frameworks and tax implications helps optimize investment outcomes. Access to timely financial data and analysis supports informed decision-making processes.

Source and External Links

## Set 1What is Pay In Kind Interest in Mezzanine Debt? - This article explains how Pay-In-Kind (PIK) interest works in mezzanine debt, where interest is paid by increasing the principal amount of the security.

## Set 2Payment-in-Kind (PIK) - Practical Law - This describes PIK as a feature where interest is added to the principal balance of a loan, rather than being paid in cash.

## Set 3Payment in Kind (PIK): Meaning, Advantages, How it Works - This article discusses Payment in Kind as a method of paying interest or dividends in a non-cash form, often by issuing more securities.

FAQs

What is a Pay-in-Kind security?

A Pay-in-Kind (PIK) security is a type of bond or loan that allows the issuer to pay interest with additional securities or equity instead of cash.

What is a Payment-in-Kind loan?

A Payment-in-Kind (PIK) loan allows borrowers to pay interest with additional debt or equity instead of cash, increasing the loan principal over time.

How do Pay-in-Kind securities differ from Payment-in-Kind loans?

Pay-in-Kind (PIK) securities pay interest through additional securities instead of cash, while Payment-in-Kind loans allow borrowers to defer cash interest payments by adding owed interest to the principal balance.

What are the main features of a Pay-in-Kind security?

Pay-in-Kind (PIK) securities allow issuers to pay interest or dividends with additional securities instead of cash, feature deferred cash payments, typically have higher interest rates to compensate for increased risk, and often include provisions for compounding unpaid interest.

What are the advantages and risks of Payment-in-Kind loans?

Payment-in-Kind (PIK) loans offer advantages such as increased cash flow flexibility by allowing interest payments in additional debt rather than cash, preserving operational liquidity for borrowers. Risks include higher overall debt levels due to accrued interest compounding, increased default risk from stretched repayment obligations, and potential challenges in valuation and refinancing because of complex payment structures.

In what situations are Pay-in-Kind securities typically used?

Pay-in-Kind (PIK) securities are typically used in leveraged buyouts, distressed companies seeking to conserve cash, and by firms aiming to defer interest payments during periods of limited liquidity.

How does interest payment work for Pay-in-Kind securities and loans?

Pay-in-Kind (PIK) securities and loans pay interest by issuing additional securities or increasing the principal amount instead of cash, allowing the borrower to defer cash interest payments until maturity or a later date.