The Constant Growth Dividend Discount Model (DDM) assumes dividends increase at a fixed rate indefinitely, providing a straightforward valuation method for stable companies. In contrast, the Multi-Stage DDM accommodates varying growth rates over different periods, capturing transitional phases of business expansion or decline. Explore the nuances between these models to enhance your dividend valuation strategies.

Main Difference

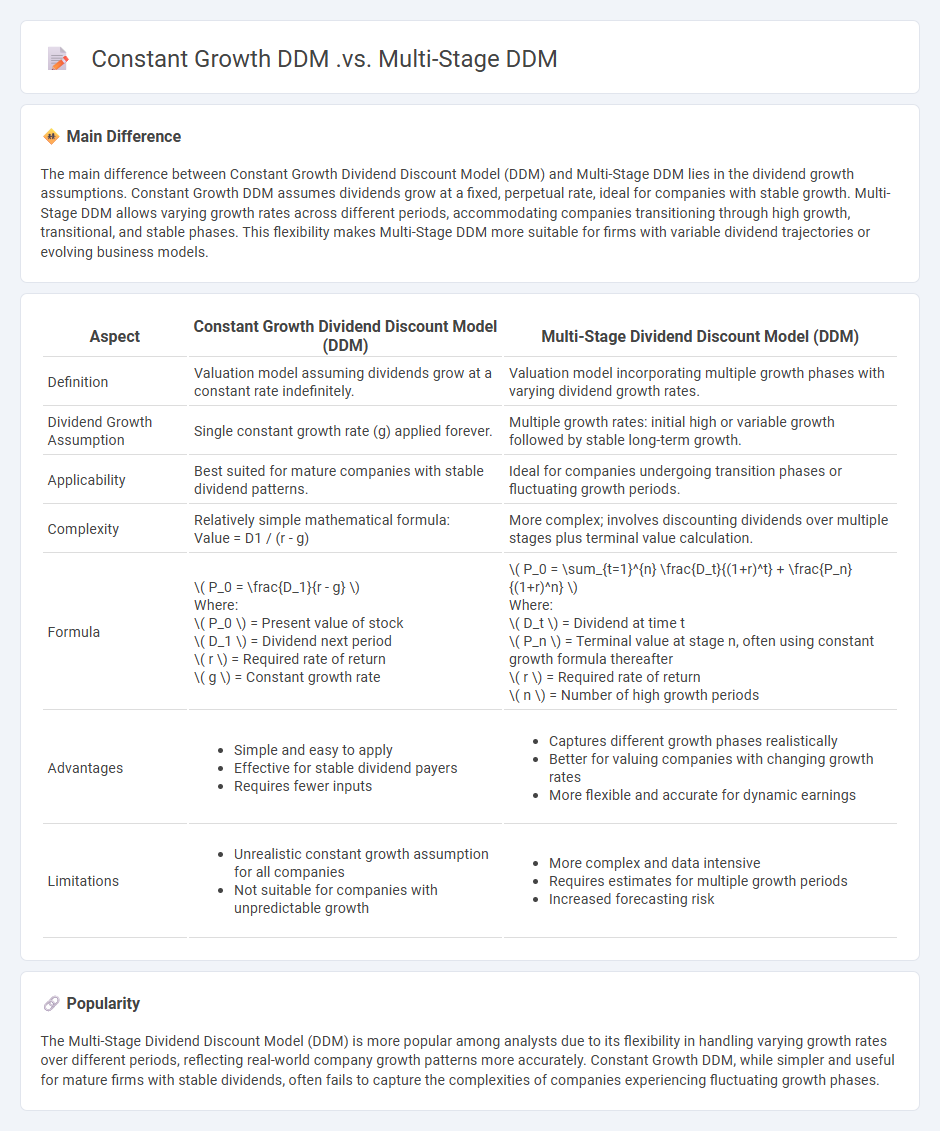

The main difference between Constant Growth Dividend Discount Model (DDM) and Multi-Stage DDM lies in the dividend growth assumptions. Constant Growth DDM assumes dividends grow at a fixed, perpetual rate, ideal for companies with stable growth. Multi-Stage DDM allows varying growth rates across different periods, accommodating companies transitioning through high growth, transitional, and stable phases. This flexibility makes Multi-Stage DDM more suitable for firms with variable dividend trajectories or evolving business models.

Connection

Constant Growth Dividend Discount Model (DDM) assumes a fixed dividend growth rate indefinitely, ideal for mature companies with stable dividend patterns. Multi-Stage DDM integrates multiple growth phases, combining an initial high-growth period followed by a constant growth phase, accommodating varying growth rates over time. Both models share the core principle of valuing stock based on the present value of expected dividends but differ in their assumptions about dividend growth trajectories.

Comparison Table

| Aspect | Constant Growth Dividend Discount Model (DDM) | Multi-Stage Dividend Discount Model (DDM) |

|---|---|---|

| Definition | Valuation model assuming dividends grow at a constant rate indefinitely. | Valuation model incorporating multiple growth phases with varying dividend growth rates. |

| Dividend Growth Assumption | Single constant growth rate (g) applied forever. | Multiple growth rates: initial high or variable growth followed by stable long-term growth. |

| Applicability | Best suited for mature companies with stable dividend patterns. | Ideal for companies undergoing transition phases or fluctuating growth periods. |

| Complexity | Relatively simple mathematical formula: Value = D1 / (r - g) |

More complex; involves discounting dividends over multiple stages plus terminal value calculation. |

| Formula |

\( P_0 = \frac{D_1}{r - g} \) Where: \( P_0 \) = Present value of stock \( D_1 \) = Dividend next period \( r \) = Required rate of return \( g \) = Constant growth rate |

\( P_0 = \sum_{t=1}^{n} \frac{D_t}{(1+r)^t} + \frac{P_n}{(1+r)^n} \) Where: \( D_t \) = Dividend at time t \( P_n \) = Terminal value at stage n, often using constant growth formula thereafter \( r \) = Required rate of return \( n \) = Number of high growth periods |

| Advantages |

|

|

| Limitations |

|

|

Dividend Discount Model (DDM)

The Dividend Discount Model (DDM) is a valuation method used to estimate the intrinsic value of a stock based on the present value of its expected future dividends. It applies the formula \( P = \frac{D_1}{r - g} \), where \( P \) represents the stock price, \( D_1 \) the dividend next year, \( r \) the required rate of return, and \( g \) the dividend growth rate. This model is particularly useful for companies with stable, predictable dividend payout patterns, such as utilities and established consumer goods firms. Analysts often rely on DDM to assess investment opportunities by focusing on dividend sustainability and growth projections.

Constant Growth Rate

Constant Growth Rate refers to a financial model where dividends or earnings increase at a fixed, steady rate over time. This concept is commonly applied in the Gordon Growth Model to value stocks based on projected future dividends. Investors use this rate to estimate the present value of an asset, assuming stable growth. Typical constant growth rates vary by industry but often align closely with long-term economic growth rates, such as the average U.S. GDP growth of about 2-3%.

Multi-Stage Growth Model

The Multi-Stage Growth Model in finance provides a framework for valuing companies with varying growth rates over different periods, reflecting realistic business cycles. It typically involves multiple phases, starting with a high growth rate that gradually tapers into stable, long-term growth, aligning with the company's lifecycle and market conditions. This model extends the Gordon Growth Model by incorporating discrete growth stages, allowing analysts to capture changing cash flow dynamics and investor expectations. Applications are common in equity valuation, especially for firms transitioning from rapid expansion to maturity.

Terminal Value

Terminal value represents the estimated value of a business or project beyond the explicit forecast period, capturing future cash flows into perpetuity. It plays a crucial role in discounted cash flow (DCF) analysis by accounting for the majority of a firm's total valuation, often exceeding 50% of the enterprise value. Common methods to calculate terminal value include the Gordon Growth Model, which assumes a perpetual growth rate, and the Exit Multiple Approach, which applies industry-standard multiples to projected financial metrics. Accurate estimation of terminal value depends on realistic growth assumptions and appropriate discount rates aligned with market conditions and company risk profiles.

Valuation Accuracy

Valuation accuracy in finance critically influences investment decisions, risk assessment, and corporate strategy by providing precise estimates of an asset's fair market value. Methods such as discounted cash flow (DCF), comparable company analysis, and precedent transactions are widely used, each with inherent assumptions affecting reliability. Financial analysts emphasize adjusting valuation models to reflect current market conditions and company-specific factors, enhancing predictive validity. Accurate valuations contribute to optimal capital allocation, merger and acquisition pricing, and regulatory compliance across sectors.

Source and External Links

Ultimate Dividend Discount Model Guide - This guide provides an overview of the constant growth model and multi-stage models, focusing on their applicability to different growth scenarios.

Dividend Discount Model - Offers insights into both constant growth models like the Gordon Growth Model and multi-stage DDMs, discussing their differences and uses.

Gordon growth model vs multi-stage dividend discount model - Compares the Gordon Growth Model with multi-stage models, highlighting their suitability for different company growth phases.

FAQs

What is the Dividend Discount Model?

The Dividend Discount Model (DDM) is a valuation method that calculates a stock's intrinsic value by discounting expected future dividend payments to their present value.

What is the Constant Growth DDM?

The Constant Growth Dividend Discount Model (DDM) values a stock by calculating the present value of an infinite series of dividends growing at a constant rate using the formula: Price = Dividend per share / (Discount rate - Growth rate).

What is the Multi-Stage DDM?

Multi-Stage DDM is a decision-making model that extends the Drift Diffusion Model by incorporating multiple evidence accumulation stages to capture complex cognitive processes in tasks with varying difficulty or changing stimuli.

How do Constant Growth and Multi-Stage DDM differ?

Constant Growth DDM assumes dividends grow at a fixed rate indefinitely, while Multi-Stage DDM incorporates multiple phases with varying dividend growth rates before stabilizing.

When is Constant Growth DDM most appropriate?

Constant Growth DDM is most appropriate for valuing companies with dividends expected to grow at a stable, constant rate indefinitely.

When should you use Multi-Stage DDM?

Use Multi-Stage Discounted Dividend Model (DDM) when a company's dividend growth rate is expected to change over different periods, such as high initial growth followed by stable long-term growth.

What are the advantages and limitations of each model?

Advantages of Decision Trees: easy to interpret, handle both categorical and numerical data, require little data preprocessing; limitations: prone to overfitting, unstable with small data changes. Advantages of Random Forests: reduce overfitting, handle large datasets well, provide feature importance; limitations: less interpretable, computationally intensive. Advantages of Support Vector Machines (SVM): effective in high-dimensional spaces, robust to overfitting with proper kernel; limitations: not well-suited for large datasets, sensitive to parameter tuning. Advantages of Neural Networks: excel at learning complex patterns, adaptable to various data types; limitations: require large datasets, computationally expensive, less interpretable.