Tobin's Q measures a firm's market value relative to the replacement cost of its assets, indicating investment attractiveness and growth potential. The Modigliani-Miller Theorem asserts that under perfect market conditions, a firm's value is unaffected by its capital structure, emphasizing the irrelevance of debt-equity choices. Explore deeper insights into how these concepts shape corporate finance strategies and investment decisions.

Main Difference

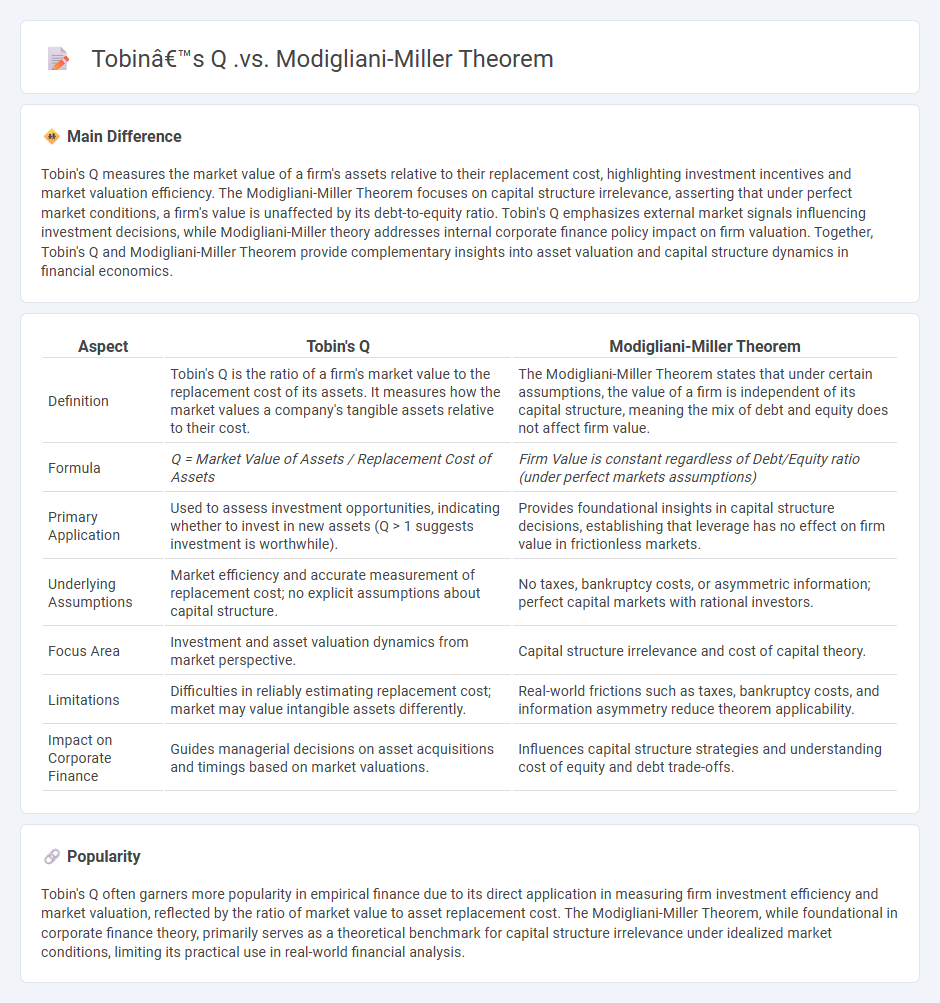

Tobin's Q measures the market value of a firm's assets relative to their replacement cost, highlighting investment incentives and market valuation efficiency. The Modigliani-Miller Theorem focuses on capital structure irrelevance, asserting that under perfect market conditions, a firm's value is unaffected by its debt-to-equity ratio. Tobin's Q emphasizes external market signals influencing investment decisions, while Modigliani-Miller theory addresses internal corporate finance policy impact on firm valuation. Together, Tobin's Q and Modigliani-Miller Theorem provide complementary insights into asset valuation and capital structure dynamics in financial economics.

Connection

Tobin's Q measures the market value of a firm's assets relative to their replacement cost, reflecting investment incentives under market valuation. The Modigliani-Miller Theorem posits that in perfect markets, a firm's value is unaffected by its capital structure, implying investment decisions depend on real asset profitability rather than financing methods. Together, Tobin's Q and the Modigliani-Miller Theorem connect by highlighting that firm valuation and investment hinge on asset efficiency and market conditions, rather than leverage or financing choices.

Comparison Table

| Aspect | Tobin's Q | Modigliani-Miller Theorem |

|---|---|---|

| Definition | Tobin's Q is the ratio of a firm's market value to the replacement cost of its assets. It measures how the market values a company's tangible assets relative to their cost. | The Modigliani-Miller Theorem states that under certain assumptions, the value of a firm is independent of its capital structure, meaning the mix of debt and equity does not affect firm value. |

| Formula | Q = Market Value of Assets / Replacement Cost of Assets | Firm Value is constant regardless of Debt/Equity ratio (under perfect markets assumptions) |

| Primary Application | Used to assess investment opportunities, indicating whether to invest in new assets (Q > 1 suggests investment is worthwhile). | Provides foundational insights in capital structure decisions, establishing that leverage has no effect on firm value in frictionless markets. |

| Underlying Assumptions | Market efficiency and accurate measurement of replacement cost; no explicit assumptions about capital structure. | No taxes, bankruptcy costs, or asymmetric information; perfect capital markets with rational investors. |

| Focus Area | Investment and asset valuation dynamics from market perspective. | Capital structure irrelevance and cost of capital theory. |

| Limitations | Difficulties in reliably estimating replacement cost; market may value intangible assets differently. | Real-world frictions such as taxes, bankruptcy costs, and information asymmetry reduce theorem applicability. |

| Impact on Corporate Finance | Guides managerial decisions on asset acquisitions and timings based on market valuations. | Influences capital structure strategies and understanding cost of equity and debt trade-offs. |

Market Valuation

Market valuation represents the total value assigned to a company's outstanding shares, often calculated as market capitalization by multiplying the current stock price by the total number of shares outstanding. This metric reflects investor perception, company performance, and market conditions, making it a critical indicator in finance for investment analysis and corporate strategy. Market valuation fluctuates with stock price movements influenced by earnings reports, economic data, and geopolitical events. Accurate valuation is essential for mergers and acquisitions, portfolio management, and financial reporting.

Capital Structure Irrelevance

Capital structure irrelevance theory, developed by Modigliani and Miller in 1958, posits that a firm's value is unaffected by its debt-to-equity ratio in perfect capital markets. This principle assumes no taxes, bankruptcy costs, or asymmetric information, implying that financing decisions do not influence the overall cost of capital. Empirical evidence shows deviations in real markets due to taxes and financial distress, yet the theory remains foundational in corporate finance for understanding the impact of leverage on firm valuation. Capital structure irrelevance helps isolate operating performance from financing effects in financial analysis and valuation models.

Asset Replacement Cost

Asset replacement cost in finance refers to the current expense required to replace an existing asset with a new one of similar function and utility. This valuation method considers the price of materials, labor, and any associated costs necessary for acquiring and installing the asset at present market rates. Companies use asset replacement cost for insurance purposes, financial reporting, and capital budgeting decisions to ensure sufficient funding for future asset acquisition. Accurate calculation helps maintain asset value on balance sheets and supports effective risk management strategies.

Leverage Impact

Leverage impact in finance refers to the use of borrowed capital to amplify investment returns, increasing both potential gains and risks. Companies with high leverage ratios often experience greater volatility in earnings and cash flow due to fixed interest obligations on debt. Financial institutions monitor leverage carefully to maintain optimal capital structure and comply with regulatory requirements such as Basel III standards. Effective leverage management enhances shareholder value but requires balancing debt costs against operational performance metrics.

Investment Decisions

Investment decisions in finance involve analyzing risk, return, and market conditions to allocate capital effectively. Evaluating financial instruments such as stocks, bonds, and derivatives requires understanding quantitative metrics like net present value (NPV), internal rate of return (IRR), and beta coefficients. Institutional investors, including pension funds and mutual funds, utilize portfolio theory and asset allocation strategies to optimize diversification and maximize long-term returns. Regulatory frameworks from entities like the SEC influence compliance and risk management in decision-making processes.

Source and External Links

Q Ratio - How To Calculate Tobin's Q, Examples - Tobin's Q is a ratio developed by James Tobin that compares a company's market value to the replacement cost of its assets, indicating whether the company's market value exceeds its asset value and potentially attracting competition if greater than 1.

Tobin's q, Economic Rents, and the Optimal Stock of Capital - Under Modigliani-Miller theorem conditions, Tobin's q represents the ratio of enterprise value to replacement cost, with the firm's value being the present value of net revenues discounted by its cost of capital, highlighting that the theorem assumes no influence from capital structure on firm value while Tobin's q relates market valuation to asset replacement.

Tobin's Q Definition, Formula & Examples - Study.com - Tobin's Q measures the market value relative to book or replacement value of assets, capturing whether a firm is over- or undervalued in the market, whereas Modigliani-Miller theorem is a foundational capital structure theory asserting the irrelevance of financing decisions on firm value under perfect market conditions.

FAQs

What is Tobin’s Q?

Tobin's Q is the ratio of a firm's market value to the replacement cost of its assets, used to assess investment attractiveness and market valuation.

What is the Modigliani-Miller Theorem?

The Modigliani-Miller Theorem states that, under perfect market conditions without taxes, bankruptcy costs, or asymmetric information, a firm's value is unaffected by its capital structure, meaning debt or equity financing does not influence the overall market value.

How does Tobin’s Q differ from the Modigliani-Miller Theorem?

Tobin's Q measures the market value of a firm's assets relative to their replacement cost, indicating investment incentives, while the Modigliani-Miller Theorem asserts that under perfect markets, a firm's capital structure does not affect its overall value.

What factors influence Tobin’s Q?

Tobin's Q is influenced by factors such as market valuation of assets, replacement cost of physical assets, firm profitability, growth opportunities, interest rates, and investor sentiment.

What assumptions underpin the Modigliani-Miller Theorem?

The Modigliani-Miller Theorem assumes perfect capital markets with no taxes, no transaction costs, no bankruptcy costs, symmetric information, and where investors and firms can borrow at the same risk-free rate.

How is Tobin’s Q used in corporate finance?

Tobin's Q measures a firm's market value divided by the replacement cost of its assets, used in corporate finance to assess investment decisions, guide capital allocation, and predict firm growth by indicating whether market valuation justifies new asset investments.

How does capital structure affect firm value according to both theories?

According to Modigliani-Miller theory, capital structure is irrelevant to firm value in perfect markets; trade-off theory states firm value is maximized by balancing tax benefits of debt against bankruptcy costs.