Origination fees are upfront charges lenders impose for processing a new loan application, typically calculated as a percentage of the loan amount. Commitment fees are periodic fees paid to secure a lender's promise to provide funds, often applied on the unused portion of a credit line. Explore the differences and implications of origination and commitment fees to better manage borrowing costs.

Main Difference

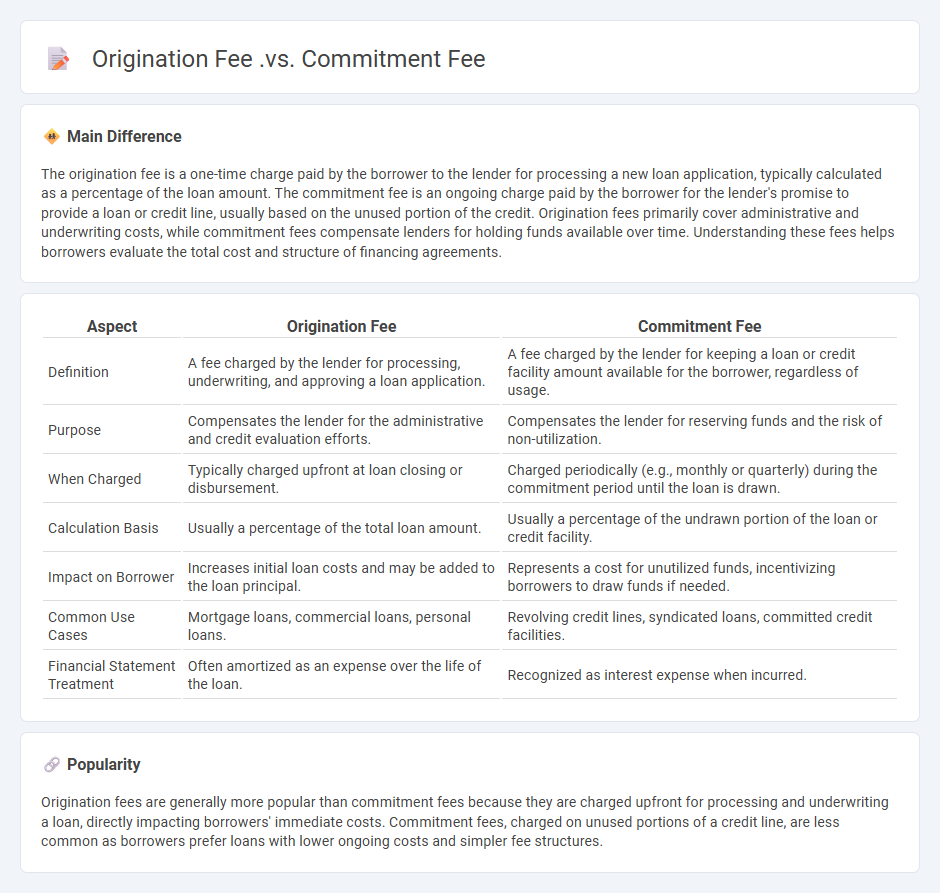

The origination fee is a one-time charge paid by the borrower to the lender for processing a new loan application, typically calculated as a percentage of the loan amount. The commitment fee is an ongoing charge paid by the borrower for the lender's promise to provide a loan or credit line, usually based on the unused portion of the credit. Origination fees primarily cover administrative and underwriting costs, while commitment fees compensate lenders for holding funds available over time. Understanding these fees helps borrowers evaluate the total cost and structure of financing agreements.

Connection

Origination fees and commitment fees are both charges related to loan agreements, reflecting costs borne by the borrower. The origination fee is a one-time charge for processing and underwriting the loan, typically a percentage of the loan amount, whereas the commitment fee is paid on the unused portion of a credit line to compensate the lender for setting aside funds. Both fees impact the overall cost of borrowing and are often detailed in the loan agreement to manage lender risk and borrower obligations.

Comparison Table

| Aspect | Origination Fee | Commitment Fee |

|---|---|---|

| Definition | A fee charged by the lender for processing, underwriting, and approving a loan application. | A fee charged by the lender for keeping a loan or credit facility amount available for the borrower, regardless of usage. |

| Purpose | Compensates the lender for the administrative and credit evaluation efforts. | Compensates the lender for reserving funds and the risk of non-utilization. |

| When Charged | Typically charged upfront at loan closing or disbursement. | Charged periodically (e.g., monthly or quarterly) during the commitment period until the loan is drawn. |

| Calculation Basis | Usually a percentage of the total loan amount. | Usually a percentage of the undrawn portion of the loan or credit facility. |

| Impact on Borrower | Increases initial loan costs and may be added to the loan principal. | Represents a cost for unutilized funds, incentivizing borrowers to draw funds if needed. |

| Common Use Cases | Mortgage loans, commercial loans, personal loans. | Revolving credit lines, syndicated loans, committed credit facilities. |

| Financial Statement Treatment | Often amortized as an expense over the life of the loan. | Recognized as interest expense when incurred. |

Loan Origination

Loan origination encompasses the entire process of applying for and obtaining a loan, including credit evaluation, underwriting, and approval. Financial institutions employ algorithms and credit scoring models, such as FICO scores, to assess borrower risk and determine loan terms. Digital loan origination platforms streamline workflows by automating document collection, compliance checks, and funding disbursement. The global loan origination market was valued at approximately USD 3 billion in 2023, with increasing adoption of AI and machine learning technologies enhancing accuracy and efficiency.

Commitment Period

The commitment period in finance refers to the time frame during which a lender agrees to provide funds to a borrower or obligor, often seen in loan agreements and credit facilities. It typically begins when the credit facility is approved and extends until the borrower either draws the funds or the period expires, usually lasting from several months to a few years. During this period, the lender is legally bound to honor the agreed credit amount, facilitating liquidity and financial planning for the borrower. Financial institutions like banks and investment firms use commitment periods to manage risk and allocate capital efficiently.

Upfront Charge

An upfront charge in finance refers to a fee paid at the beginning of a transaction, often associated with investment funds or loan agreements. This charge is typically expressed as a percentage of the total investment or loan amount and covers administrative costs or commissions. Mutual funds and unit trusts frequently impose upfront charges ranging from 0% to 5%, impacting the net amount invested. Evaluating upfront charges is crucial for investors to understand the true cost and potential returns of their financial products.

Unused Credit Line

An unused credit line represents the portion of a revolving credit facility or credit card limit that remains available for borrowing but has not yet been utilized by the borrower. Lenders calculate unused credit lines to assess credit utilization ratios, which directly impact credit scores and borrowing capacity. Maintaining a low utilization rate, typically below 30%, can improve credit ratings and facilitate access to lower interest rates. Financial institutions manage unused credit exposure to gauge risk and allocate capital effectively.

Fee Structure

The fee structure in finance refers to the detailed breakdown of charges applicable for various financial services, including management fees, advisory fees, and performance-based fees. Asset management firms typically charge an annual fee ranging from 0.5% to 2% of assets under management (AUM), influencing investor costs and net returns. Understanding fee structures is essential for transparent client relationships and regulatory compliance, with entities like the SEC enforcing disclosure requirements under the Investment Advisers Act of 1940. Fee structures directly impact investment performance evaluation and client decision-making within wealth management and financial advisory sectors.

Source and External Links

Commitment Fee vs: Origination Fee: Demystifying Lending Charges - Commitment fees compensate lenders for reserving funds for the borrower, while origination fees cover the lender's loan processing costs such as underwriting and document preparation, generally ranging from 0.5% to 1% of the loan amount.

What Is an Origination Fee? - Experian - Origination fees are one-time upfront charges that cover the cost of processing a loan application, which can be paid upfront, at closing, or added to the loan balance, affecting the loan proceeds and monthly payments.

Understanding Origination Fees and Discount Points in Mortgage Loans - Origination fees specifically cover administrative costs like underwriting and loan document preparation, whereas commitment fees are charged to compensate the lender for holding the credit line and ensuring borrower commitment to the loan.

FAQs

What is an origination fee?

An origination fee is a one-time charge by a lender for processing a loan application, typically expressed as a percentage of the loan amount.

What is a commitment fee?

A commitment fee is a charge paid by a borrower to a lender for reserving a portion of the loan amount, ensuring the funds are available when needed.

How does an origination fee differ from a commitment fee?

An origination fee is a one-time charge by a lender for processing a loan application, typically a percentage of the loan amount, while a commitment fee is an ongoing charge on the unused portion of a loan or credit line during the commitment period.

When is an origination fee charged?

An origination fee is charged at the loan closing or disbursement to cover the lender's processing and underwriting costs.

When is a commitment fee applied?

A commitment fee is applied when a lender agrees to hold funds available for a borrower, typically on a revolving credit line or loan commitment, during the period the funds are unutilized.

Why do lenders charge origination and commitment fees?

Lenders charge origination fees to cover administrative costs and assess loan risk, while commitment fees compensate for reserving loan funds until disbursement.

How do origination and commitment fees impact loan costs?

Origination and commitment fees increase the total loan costs by adding upfront charges that borrowers must pay, which raise the effective interest rate and reduce the net amount received from the loan.