Money market focuses on short-term debt instruments and liquidity management, including Treasury bills, commercial paper, and certificates of deposit. Capital market involves long-term investment securities such as stocks and bonds, facilitating capital formation for businesses and governments. Explore further to understand their distinct roles in financial markets.

Main Difference

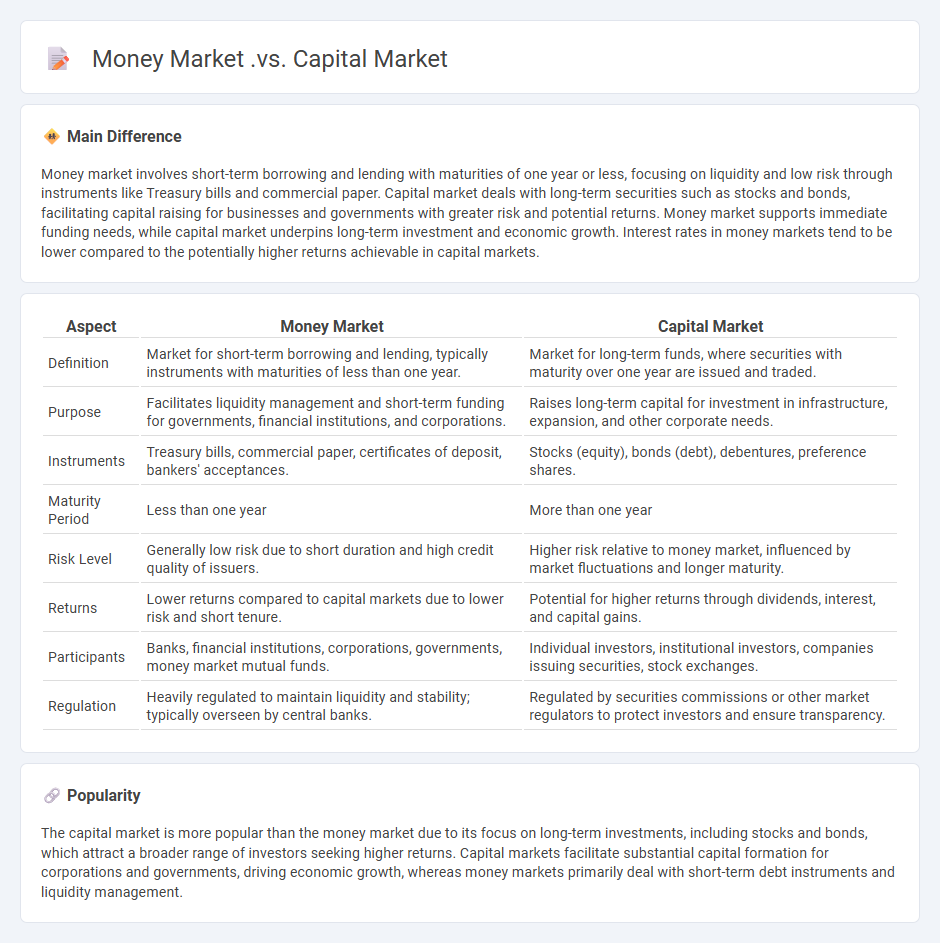

Money market involves short-term borrowing and lending with maturities of one year or less, focusing on liquidity and low risk through instruments like Treasury bills and commercial paper. Capital market deals with long-term securities such as stocks and bonds, facilitating capital raising for businesses and governments with greater risk and potential returns. Money market supports immediate funding needs, while capital market underpins long-term investment and economic growth. Interest rates in money markets tend to be lower compared to the potentially higher returns achievable in capital markets.

Connection

The money market and capital market are interconnected through the flow of short-term and long-term funds, where the money market provides liquidity and funding for short durations, while the capital market facilitates investment in long-term securities like stocks and bonds. Institutions and investors often move funds between these markets based on liquidity needs, risk tolerance, and investment horizons, ensuring efficient capital allocation. Central banks and financial intermediaries play crucial roles in maintaining this connection by regulating interest rates and providing credit across both markets.

Comparison Table

| Aspect | Money Market | Capital Market |

|---|---|---|

| Definition | Market for short-term borrowing and lending, typically instruments with maturities of less than one year. | Market for long-term funds, where securities with maturity over one year are issued and traded. |

| Purpose | Facilitates liquidity management and short-term funding for governments, financial institutions, and corporations. | Raises long-term capital for investment in infrastructure, expansion, and other corporate needs. |

| Instruments | Treasury bills, commercial paper, certificates of deposit, bankers' acceptances. | Stocks (equity), bonds (debt), debentures, preference shares. |

| Maturity Period | Less than one year | More than one year |

| Risk Level | Generally low risk due to short duration and high credit quality of issuers. | Higher risk relative to money market, influenced by market fluctuations and longer maturity. |

| Returns | Lower returns compared to capital markets due to lower risk and short tenure. | Potential for higher returns through dividends, interest, and capital gains. |

| Participants | Banks, financial institutions, corporations, governments, money market mutual funds. | Individual investors, institutional investors, companies issuing securities, stock exchanges. |

| Regulation | Heavily regulated to maintain liquidity and stability; typically overseen by central banks. | Regulated by securities commissions or other market regulators to protect investors and ensure transparency. |

Maturity Period

The maturity period in finance refers to the length of time until a financial instrument, such as a bond or a loan, reaches its due date for repayment. This period determines when the principal amount must be repaid to the investor or lender along with any accrued interest. Maturity periods vary widely, ranging from short-term instruments like Treasury bills with maturities of one year or less to long-term bonds that can mature in 10, 20, or even 30 years. The maturity period impacts investment strategies, interest rate risk, and the valuation of fixed-income securities.

Instruments

Financial instruments represent contracts that create financial assets for one party and liabilities or equity for another, facilitating the allocation of capital and risk management. Common types include equities, bonds, derivatives such as options and futures, and money market instruments like Treasury bills. These instruments underpin trading in capital markets, with global equity markets valued at approximately $120 trillion and the derivatives market exceeding $600 trillion notional value. Their effective use supports portfolio diversification, liquidity provision, and price discovery within financial systems.

Risk Level

Risk level in finance measures the potential variability or loss an investment might experience over a specified period. It is typically quantified using metrics such as standard deviation, beta, and Value at Risk (VaR), which assess volatility, market sensitivity, and potential loss thresholds, respectively. High-risk investments often offer higher expected returns but come with increased uncertainty, while low-risk options provide stability with lower yields. Understanding risk levels allows investors to align portfolios with their financial goals and risk tolerance.

Market Participants

Market participants encompass a diverse range of entities actively involved in financial markets, including individual investors, institutional investors, brokers, dealers, market makers, and regulatory bodies. These participants facilitate liquidity, price discovery, and efficient capital allocation by engaging in buying and selling securities, commodities, and other financial instruments across stock exchanges and over-the-counter markets. Institutional investors such as mutual funds, pension funds, and hedge funds often hold significant market power due to their substantial assets under management, influencing market trends and volatility. Regulatory agencies like the U.S. Securities and Exchange Commission (SEC) enforce compliance and transparency to maintain market integrity and protect investor interests.

Regulatory Authority

Regulatory authorities in finance, such as the U.S. Securities and Exchange Commission (SEC) and the Financial Conduct Authority (FCA) in the UK, enforce compliance with financial laws and protect investors. These bodies oversee market activities, ensuring transparency, fair trading, and the prevention of fraud and manipulation. They implement regulations like the Dodd-Frank Act and MiFID II to enhance financial stability and market integrity. Their role is critical in maintaining confidence in capital markets and safeguarding economic interests.

Source and External Links

## Money Market vs Capital Market ResourcesMoney Markets vs Capital Markets - This article provides a guide for investors, highlighting the differences between money markets and capital markets, including liquidity, risk, and investment instruments.

Money Market vs Capital Market - Explains the key differences between the two markets, focusing on their purposes, financial instruments, and risk profiles.

Difference Between Money Market and Capital Market - Outlines the main distinctions between money markets, which focus on short-term financing, and capital markets, which are for long-term investments.

FAQs

What is a money market?

A money market is a sector of the financial market where short-term debt securities with high liquidity and low risk, such as Treasury bills, commercial paper, and certificates of deposit, are traded.

What is a capital market?

A capital market is a financial market where long-term securities such as stocks and bonds are bought and sold to raise capital for businesses and governments.

What is the difference between money market and capital market?

The money market deals with short-term debt instruments maturing within one year, such as Treasury bills and commercial paper, while the capital market handles long-term securities like stocks and bonds with maturities over one year.

What are the main instruments used in the money market?

The main instruments used in the money market are Treasury bills, commercial paper, certificates of deposit, repurchase agreements, and bankers' acceptances.

What are the key instruments found in the capital market?

Key instruments in the capital market include stocks, bonds, debentures, mutual funds, and derivatives.

Who are the main participants in the money market and capital market?

Main participants in the money market include commercial banks, central banks, financial institutions, and corporations. Main participants in the capital market are individual investors, institutional investors, investment banks, corporations, and government entities.

Why are money markets and capital markets important for the economy?

Money markets provide short-term liquidity for businesses and governments, ensuring efficient cash flow management, while capital markets facilitate long-term investment by allowing companies to raise funds for expansion and innovation, driving economic growth and stability.