Basel III and Dodd-Frank represent critical regulatory frameworks designed to strengthen the global financial system by enhancing bank capital requirements and reducing systemic risks. Basel III focuses on international banking standards established by the Basel Committee on Banking Supervision, emphasizing liquidity coverage ratios and leverage limits. Explore the key differences and impacts of Basel III versus Dodd-Frank to understand their roles in financial stability and regulatory compliance.

Main Difference

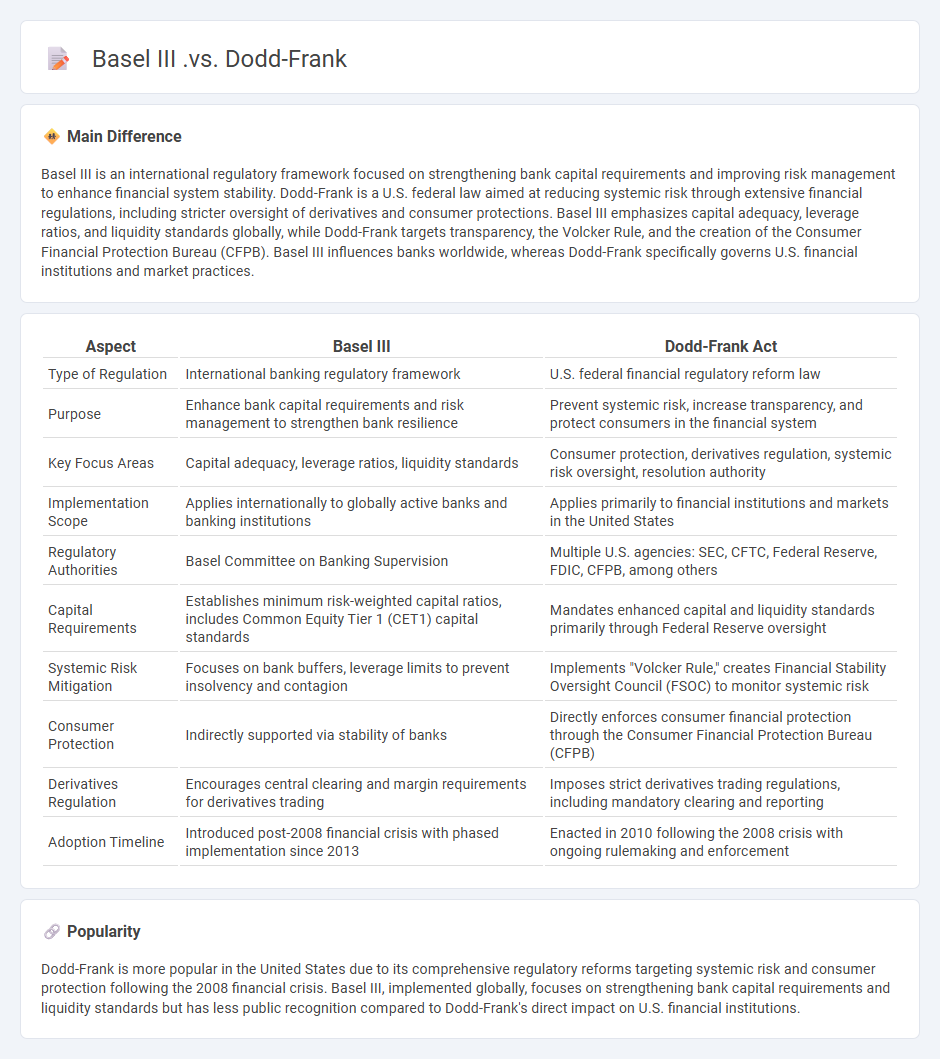

Basel III is an international regulatory framework focused on strengthening bank capital requirements and improving risk management to enhance financial system stability. Dodd-Frank is a U.S. federal law aimed at reducing systemic risk through extensive financial regulations, including stricter oversight of derivatives and consumer protections. Basel III emphasizes capital adequacy, leverage ratios, and liquidity standards globally, while Dodd-Frank targets transparency, the Volcker Rule, and the creation of the Consumer Financial Protection Bureau (CFPB). Basel III influences banks worldwide, whereas Dodd-Frank specifically governs U.S. financial institutions and market practices.

Connection

Basel III and Dodd-Frank are connected through their shared goal of strengthening financial system stability and reducing systemic risk. Basel III, developed by the Basel Committee on Banking Supervision, sets international regulatory standards for bank capital adequacy, stress testing, and liquidity requirements, while Dodd-Frank is a U.S. federal law focused on comprehensive financial reform and consumer protection. Both frameworks emphasize enhanced transparency, risk management, and oversight of financial institutions to prevent future financial crises.

Comparison Table

| Aspect | Basel III | Dodd-Frank Act |

|---|---|---|

| Type of Regulation | International banking regulatory framework | U.S. federal financial regulatory reform law |

| Purpose | Enhance bank capital requirements and risk management to strengthen bank resilience | Prevent systemic risk, increase transparency, and protect consumers in the financial system |

| Key Focus Areas | Capital adequacy, leverage ratios, liquidity standards | Consumer protection, derivatives regulation, systemic risk oversight, resolution authority |

| Implementation Scope | Applies internationally to globally active banks and banking institutions | Applies primarily to financial institutions and markets in the United States |

| Regulatory Authorities | Basel Committee on Banking Supervision | Multiple U.S. agencies: SEC, CFTC, Federal Reserve, FDIC, CFPB, among others |

| Capital Requirements | Establishes minimum risk-weighted capital ratios, includes Common Equity Tier 1 (CET1) capital standards | Mandates enhanced capital and liquidity standards primarily through Federal Reserve oversight |

| Systemic Risk Mitigation | Focuses on bank buffers, leverage limits to prevent insolvency and contagion | Implements "Volcker Rule," creates Financial Stability Oversight Council (FSOC) to monitor systemic risk |

| Consumer Protection | Indirectly supported via stability of banks | Directly enforces consumer financial protection through the Consumer Financial Protection Bureau (CFPB) |

| Derivatives Regulation | Encourages central clearing and margin requirements for derivatives trading | Imposes strict derivatives trading regulations, including mandatory clearing and reporting |

| Adoption Timeline | Introduced post-2008 financial crisis with phased implementation since 2013 | Enacted in 2010 following the 2008 crisis with ongoing rulemaking and enforcement |

Capital Requirements

Capital requirements represent the mandatory minimum amount of equity and reserves that financial institutions must hold to absorb potential losses and ensure stability. Regulatory frameworks such as Basel III set specific capital ratios, including Common Equity Tier 1 (CET1) at 4.5% and a total capital ratio of 8%, to mitigate risks in banking. Adequate capital buffers support confidence in the financial system by protecting depositors and maintaining operational continuity during economic downturns. Compliance with capital requirements directly influences a bank's lending capacity and risk management strategies.

Liquidity Standards

Liquidity standards in finance define minimum requirements for financial institutions to maintain sufficient liquid assets that can be quickly converted to cash to meet short-term obligations. Regulatory frameworks, such as Basel III, establish key metrics like the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) to promote stability and reduce systemic risk. Banks must hold high-quality liquid assets (HQLA) representing at least 100% of expected net cash outflows over a 30-day stress period. These standards strengthen the resilience of financial institutions during periods of market stress and improve confidence in the banking system.

Systemic Risk Oversight

Systemic risk oversight involves monitoring and managing risks that threaten the stability of the entire financial system, including banks, insurance companies, and capital markets. Regulatory bodies such as the Financial Stability Oversight Council (FSOC) in the United States and the European Systemic Risk Board (ESRB) are key institutions responsible for identifying and mitigating systemic risks. Stress testing, macroprudential policies, and inter-agency coordination help prevent financial crises stemming from interconnected exposures and contagion effects. Effective oversight relies on real-time data analysis, risk indicators, and close supervision of systemically important financial institutions (SIFIs).

Stress Testing

Stress testing in finance evaluates the resilience of financial institutions, portfolios, or markets under extreme but plausible adverse conditions. It involves simulating scenarios like economic recessions, market crashes, or interest rate spikes to measure potential losses and vulnerabilities. Regulatory frameworks such as Basel III mandate banks to perform stress tests regularly to ensure capital adequacy and risk management. Results guide risk mitigation strategies and improve systemic stability in the global financial system.

Regulatory Scope

Regulatory scope in finance defines the range of activities, institutions, and transactions subject to oversight by financial regulatory authorities such as the SEC, FCA, and the Federal Reserve. It encompasses various sectors including banking, securities markets, insurance, and asset management to ensure transparency, market integrity, and consumer protection. Compliance requirements extend to anti-money laundering (AML), capital adequacy under Basel III, and reporting standards like IFRS and GAAP. Regulatory scope continues to evolve in response to technological advances, financial innovation, and systemic risk management.

Source and External Links

The Tale of Two Regulations -- Dodd-Frank Act and Basel III - Basel III and Dodd-Frank differ notably in credit risk treatment and regulatory reliance on credit ratings, with Dodd-Frank requiring securitized asset originators to retain 5% credit risk while Basel III does not, and Dodd-Frank imposing stricter rules on credit rating agencies unlike Basel III which depends heavily on them.

Dodd-Frank and Basel III: Implementation in the U.S. - Diaz Reus - Both regulations aim to strengthen financial stability post-crisis, but differ in leverage requirements, systemic liquidity provisions, and use of credit ratings, with Dodd-Frank prohibiting credit rating references in federal rules and Basel III relying on them for liquidity coverage.

The Dodd-Frank Act and Basel III - Asian Development Bank - The Dodd-Frank Act includes macroprudential measures such as stress tests and systemic risk investigations that Basel III lacks, which is criticized as flawed for macroprudential regulation, offering lessons for emerging markets in balancing finance sector reforms.

FAQs

What is the purpose of Basel III?

Basel III aims to strengthen bank capital requirements, improve risk management, and enhance financial system stability.

What is the purpose of Dodd-Frank?

Dodd-Frank aims to promote financial stability by improving accountability and transparency in the financial system, protecting consumers from abusive practices, and ending bailouts of failing financial firms.

How do Basel III and Dodd-Frank differ in scope?

Basel III is an international regulatory framework focused on strengthening bank capital requirements and risk management, while Dodd-Frank is a U.S. federal law aimed at comprehensive financial reform, targeting systemic risk, consumer protection, and financial stability.

What are the key capital requirements in Basel III?

Basel III requires banks to maintain a minimum Common Equity Tier 1 (CET1) capital ratio of 4.5%, a Tier 1 capital ratio of 6%, and a total capital ratio of 8%, along with a Capital Conservation Buffer of 2.5%, a Countercyclical Buffer of up to 2.5%, and a leverage ratio minimum of 3%.

How does Dodd-Frank address systemic risk?

Dodd-Frank addresses systemic risk by establishing the Financial Stability Oversight Council (FSOC) to identify and monitor systemic threats, imposing stricter regulations on systemically important financial institutions (SIFIs), enhancing transparency through the Volcker Rule limiting proprietary trading, and creating the Orderly Liquidation Authority to manage failing firms without destabilizing the financial system.

Which institutions are affected by Basel III and Dodd-Frank?

Basel III affects internationally active banks and banking organizations, while Dodd-Frank targets U.S. financial institutions including banks, bank holding companies, and non-bank financial entities subject to regulatory supervision.

How do Basel III and Dodd-Frank impact global banking practices?

Basel III enhances global banking practices by enforcing stricter capital requirements, liquidity standards, and leverage ratios, while Dodd-Frank strengthens U.S. financial system stability through comprehensive regulation of derivatives, increased transparency, and reinforced consumer protections.