Homogeneous expectations assume that all economic agents share identical beliefs about future outcomes, leading to uniform decision-making processes and market predictions. Heterogeneous expectations recognize that agents hold diverse beliefs influenced by varying information, experience, and cognitive biases, which contributes to market dynamics and unpredictability. Explore how these contrasting expectation models impact economic theory and real-world market behavior.

Main Difference

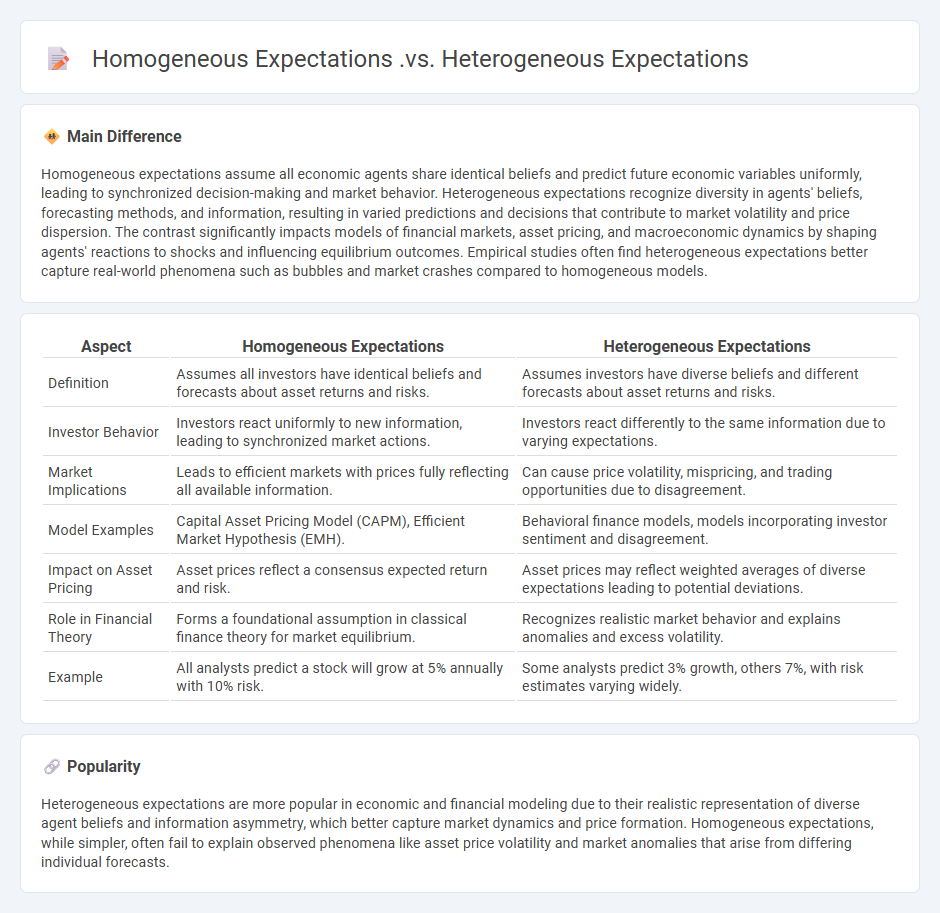

Homogeneous expectations assume all economic agents share identical beliefs and predict future economic variables uniformly, leading to synchronized decision-making and market behavior. Heterogeneous expectations recognize diversity in agents' beliefs, forecasting methods, and information, resulting in varied predictions and decisions that contribute to market volatility and price dispersion. The contrast significantly impacts models of financial markets, asset pricing, and macroeconomic dynamics by shaping agents' reactions to shocks and influencing equilibrium outcomes. Empirical studies often find heterogeneous expectations better capture real-world phenomena such as bubbles and market crashes compared to homogeneous models.

Connection

Homogeneous expectations occur when all market participants share the same beliefs about future outcomes, resulting in uniform predictions and actions. Heterogeneous expectations arise from differing beliefs and information among agents, leading to diverse forecasts and behaviors. The interaction between these expectation types shapes market dynamics, influencing asset price volatility and trading volume.

Comparison Table

| Aspect | Homogeneous Expectations | Heterogeneous Expectations |

|---|---|---|

| Definition | Assumes all investors have identical beliefs and forecasts about asset returns and risks. | Assumes investors have diverse beliefs and different forecasts about asset returns and risks. |

| Investor Behavior | Investors react uniformly to new information, leading to synchronized market actions. | Investors react differently to the same information due to varying expectations. |

| Market Implications | Leads to efficient markets with prices fully reflecting all available information. | Can cause price volatility, mispricing, and trading opportunities due to disagreement. |

| Model Examples | Capital Asset Pricing Model (CAPM), Efficient Market Hypothesis (EMH). | Behavioral finance models, models incorporating investor sentiment and disagreement. |

| Impact on Asset Pricing | Asset prices reflect a consensus expected return and risk. | Asset prices may reflect weighted averages of diverse expectations leading to potential deviations. |

| Role in Financial Theory | Forms a foundational assumption in classical finance theory for market equilibrium. | Recognizes realistic market behavior and explains anomalies and excess volatility. |

| Example | All analysts predict a stock will grow at 5% annually with 10% risk. | Some analysts predict 3% growth, others 7%, with risk estimates varying widely. |

Risk Assessment

Risk assessment in finance involves identifying, analyzing, and quantifying potential financial losses associated with investments, loans, or market fluctuations. Techniques such as Value at Risk (VaR), stress testing, and scenario analysis enable institutions to estimate the probability and impact of adverse events on portfolios. Regulatory frameworks like Basel III mandate rigorous risk assessment to ensure capital adequacy and financial stability. Effective risk assessment helps investors and financial managers optimize returns while mitigating exposure to credit, market, operational, and liquidity risks.

Market Efficiency

Market efficiency in finance refers to the extent to which asset prices fully reflect all available information, allowing markets to allocate resources optimally. The Efficient Market Hypothesis (EMH) classifies market efficiency into three forms: weak, semi-strong, and strong, each representing different levels of information integration. Empirical studies show that stock prices generally adjust rapidly to public news, supporting semi-strong efficiency in developed markets like the NYSE and NASDAQ. However, anomalies such as market bubbles and behavioral biases challenge the absolute validity of efficiency across all asset classes.

Information Interpretation

Information interpretation in finance involves analyzing financial data, market trends, and economic indicators to make informed investment decisions. It requires understanding balance sheets, income statements, and cash flow reports to evaluate a company's financial health accurately. Techniques such as ratio analysis, trend analysis, and forecasting models enhance the assessment of risk and profitability. Effective interpretation supports portfolio management, risk assessment, and strategic planning within financial markets.

Asset Pricing

Asset pricing models in finance analyze how securities are valued based on risk, return, and market conditions. The Capital Asset Pricing Model (CAPM) and Arbitrage Pricing Theory (APT) are foundational frameworks linking expected returns to systematic risk factors. Empirical asset pricing tests use historical data to evaluate the validity and predictive power of these models across equity, bond, and derivative markets. Advances in behavioral finance and machine learning are increasingly integrated to improve pricing accuracy and capture market anomalies.

Investor Beliefs

Investor beliefs significantly influence financial markets by shaping expectations about asset returns, risk, and market dynamics. Behavioral finance research identifies biases such as overconfidence, loss aversion, and herding behavior that distort investor perceptions and decision-making. Empirical studies show that heterogeneous beliefs contribute to price volatility and trading volume, affecting market efficiency. Understanding these psychological factors is essential for developing models that predict asset price movements and portfolio choices.

Source and External Links

The Danger of Assuming Homogeneous Expectations - Homogeneous expectations assume investors have the same forecasts and preferences, leading to unrealistic market price behavior, whereas heterogeneous expectations, with diverse investor beliefs, create more realistic price dynamics and reduce market inefficiencies.

Homogeneous Expectations - Overview, Framework, Advantages - Homogeneous expectations posit that all investors are rational and share identical views on asset returns and risks, while heterogeneous expectations acknowledge variations in investor perceptions, which better reflect real-world market interactions and asset pricing.

The Danger of Assuming Homogeneous Expectations - jstor - Even a small degree of heterogeneous expectations among investors significantly impacts risky asset prices, contrasting with models assuming homogeneous expectations that tend to generate market inefficiencies and less realistic outcomes.

FAQs

What are expectations in economics and finance?

Expectations in economics and finance refer to the beliefs or forecasts that individuals and markets form about future economic variables, such as inflation rates, interest rates, stock prices, or GDP growth, which influence their decision-making and behavior.

What is the meaning of homogeneous expectations?

Homogeneous expectations mean all investors have the same beliefs about future asset returns, risks, and market conditions, leading to identical forecasts and investment decisions.

What is the meaning of heterogeneous expectations?

Heterogeneous expectations refer to diverse beliefs or predictions held by different individuals or groups about future events or outcomes within the same market or environment.

How do homogeneous and heterogeneous expectations affect market outcomes?

Homogeneous expectations lead to synchronized investor behavior, causing market prices to reflect common information efficiently and potentially increasing market volatility. Heterogeneous expectations create diverse investor beliefs, resulting in varied trading strategies that enhance market liquidity and price discovery but may also induce price dispersion and temporary mispricings.

What are advantages and disadvantages of homogeneous expectations?

Homogeneous expectations enhance market efficiency by aligning investor beliefs, reducing information asymmetry, and facilitating price discovery. However, they can lead to market herding, reduced diversification of opinions, increased systemic risk, and potential asset bubbles.

What are the implications of heterogeneous expectations in asset pricing?

Heterogeneous expectations in asset pricing lead to increased market volatility, liquidity variations, and potential mispricing due to diverse investor beliefs influencing demand and supply dynamics.

Why are heterogeneous expectations important in behavioral finance?

Heterogeneous expectations in behavioral finance are important because they explain diverse investor behavior, market anomalies, and price volatility by reflecting differences in information, cognitive biases, and risk perceptions among market participants.