Tontines and annuities are financial products designed to provide income, often for retirement planning, but function through distinct mechanisms. A tontine pools participants' contributions into a single fund, redistributing shares of the surviving members' interest upon each death, while an annuity offers a fixed or variable stream of payments in exchange for an initial lump sum. Explore the detailed differences between tontines and annuities to determine which suits your financial goals.

Main Difference

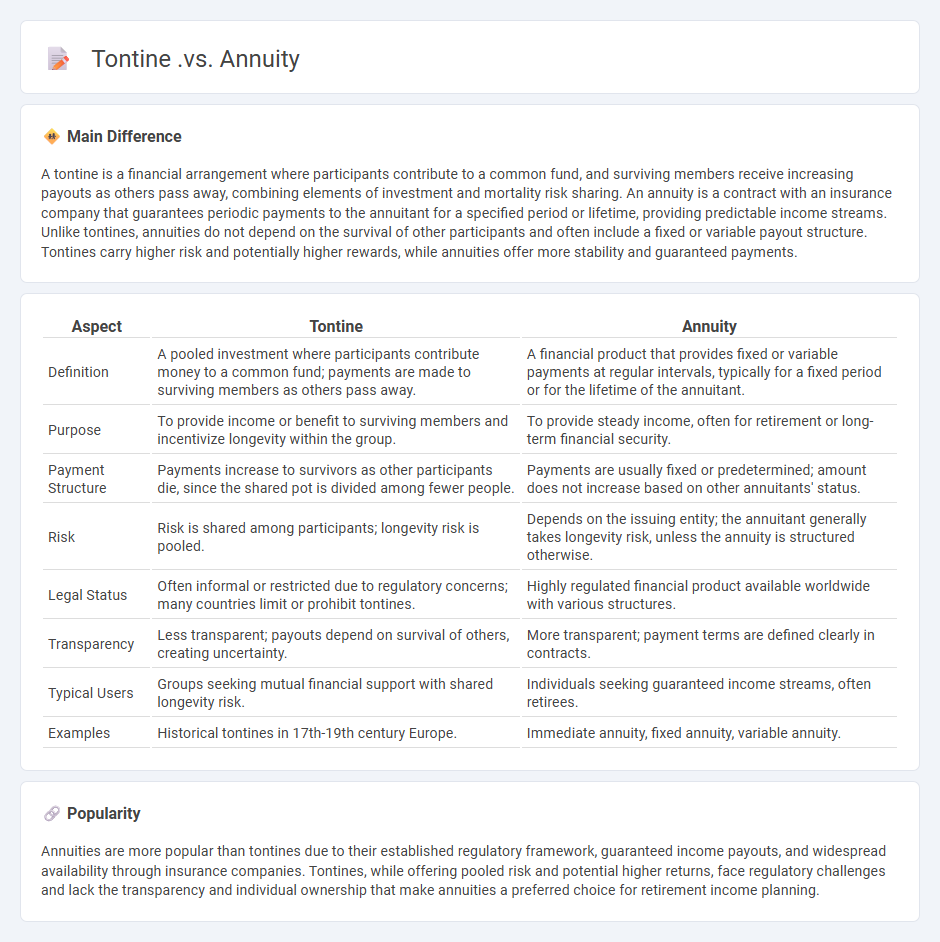

A tontine is a financial arrangement where participants contribute to a common fund, and surviving members receive increasing payouts as others pass away, combining elements of investment and mortality risk sharing. An annuity is a contract with an insurance company that guarantees periodic payments to the annuitant for a specified period or lifetime, providing predictable income streams. Unlike tontines, annuities do not depend on the survival of other participants and often include a fixed or variable payout structure. Tontines carry higher risk and potentially higher rewards, while annuities offer more stability and guaranteed payments.

Connection

Tontines and annuities are financial instruments designed to provide income over time, often used for retirement planning. A tontine pools contributions from participants, who receive payments that increase as members pass away, while an annuity guarantees a fixed or variable income stream based on a contract with an insurer. Both mechanisms manage lifespan risk by distributing payments contingent on survival, blending elements of insurance and investment.

Comparison Table

| Aspect | Tontine | Annuity |

|---|---|---|

| Definition | A pooled investment where participants contribute money to a common fund; payments are made to surviving members as others pass away. | A financial product that provides fixed or variable payments at regular intervals, typically for a fixed period or for the lifetime of the annuitant. |

| Purpose | To provide income or benefit to surviving members and incentivize longevity within the group. | To provide steady income, often for retirement or long-term financial security. |

| Payment Structure | Payments increase to survivors as other participants die, since the shared pot is divided among fewer people. | Payments are usually fixed or predetermined; amount does not increase based on other annuitants' status. |

| Risk | Risk is shared among participants; longevity risk is pooled. | Depends on the issuing entity; the annuitant generally takes longevity risk, unless the annuity is structured otherwise. |

| Legal Status | Often informal or restricted due to regulatory concerns; many countries limit or prohibit tontines. | Highly regulated financial product available worldwide with various structures. |

| Transparency | Less transparent; payouts depend on survival of others, creating uncertainty. | More transparent; payment terms are defined clearly in contracts. |

| Typical Users | Groups seeking mutual financial support with shared longevity risk. | Individuals seeking guaranteed income streams, often retirees. |

| Examples | Historical tontines in 17th-19th century Europe. | Immediate annuity, fixed annuity, variable annuity. |

Pooled Risk

Pooled risk in finance refers to the aggregation of individual risks to reduce the overall impact of uncertainty on investments or liabilities. By combining multiple risk exposures, insurers, asset managers, and financial institutions achieve diversification, minimizing the probability of large losses for any single participant. This practice is fundamental in insurance underwriting and mutual funds, where risk sharing stabilizes returns and enhances predictability. Statistical techniques such as the law of large numbers support pooled risk effectiveness by leveraging large sample sizes to smooth out variability.

Lifetime Income

Lifetime income represents the total amount of money an individual earns over their entire working life, encompassing wages, salaries, bonuses, and investment returns. It plays a critical role in financial planning, retirement readiness, and wealth accumulation strategies. Accurate lifetime income projections utilize actuarial data, inflation rates, and projected earning growth to ensure sustainable cash flow. Understanding the impact of Social Security benefits, pension plans, and annuity options further optimizes lifetime income management for long-term financial security.

Mortality Credits

Mortality credits refer to the financial gains earned by survivors in pooled annuity or life insurance products due to the mortality of other participants. These credits enhance the expected return for surviving policyholders by redistributing the unclaimed benefits of deceased members. Mortality credits play a crucial role in retirement finance, particularly in products like variable annuities and longevity insurance, where they help mitigate longevity risk. Understanding mortality credits is essential for actuaries and financial planners designing sustainable lifetime income strategies.

Guaranteed Payments

Guaranteed payments in finance refer to fixed amounts paid to partners in a partnership regardless of the partnership's profitability. These payments are considered ordinary income for recipients and are deductible business expenses for the partnership. Guaranteed payments ensure partners receive compensation for services or capital contributed, independent of profit distribution. The IRS treats them distinctly from profit shares, impacting tax reporting and liability.

Flexibility

Flexibility in finance refers to the ability of individuals or organizations to adapt their financial strategies and decisions in response to changing market conditions, economic environments, or unforeseen expenses. It involves maintaining liquidity, diversifying investments, and having access to credit to quickly seize opportunities or mitigate risks. Companies with flexible capital structures can adjust debt and equity ratios to optimize cost of capital and support growth initiatives. Financial flexibility enhances resilience, enabling smoother navigation through economic downturns and volatility in asset prices.

Source and External Links

Tontine vs. Annuity: Which Is Better? - Both provide lifetime income but differ in structure: annuities offer fixed payments guaranteed by insurers, whereas tontines pool payments and increase survivor payouts as participants die, shifting longevity risk among members.

Annuities Versus Tontines in the 21st Century - Annuities provide predictable lifetime income but are costly due to capital and longevity risk, while tontines are less capital-intensive, with payments increasing over time as survivors share the pool, making them simpler and cheaper to administer.

Could Tontines Be an Alternative to Annuities? - Annuities insure against longevity risk at a higher cost, whereas tontines pass longevity risk to members and require only an administrator, potentially making tontines less expensive but with less payment certainty.

FAQs

What is a tontine?

A tontine is a financial arrangement where participants contribute to a common fund, and surviving members receive increasing shares as others die, combining elements of investment and insurance.

What is an annuity?

An annuity is a financial product that provides a series of fixed payments made at regular intervals, often used as a steady income stream during retirement.

How does a tontine differ from an annuity?

A tontine pools participants' contributions, distributing benefits only to surviving members, while an annuity provides fixed periodic payments to an individual regardless of others' lifespans.

What are the benefits of a tontine?

A tontine offers benefits such as pooled capital growth, reduced investment risk, tax advantages, and a unique survivor benefit that increases payouts to remaining participants as others pass away.

What are the risks of a tontine?

The risks of a tontine include longevity risk for early death participants, lack of liquidity, potential mismanagement of funds, legal and regulatory uncertainties, and the possibility of unequal payouts due to survivor benefits.

Who should consider an annuity?

Individuals seeking guaranteed income during retirement, those aiming to manage longevity risk, and people wanting to supplement other retirement savings should consider an annuity.

How are payments distributed in a tontine and an annuity?

Payments in a tontine are distributed among surviving members, increasing as participants die, while annuity payments are fixed or variable amounts paid periodically to an individual for a specified term or lifetime.