Securitization transforms illiquid assets into marketable securities by pooling various financial assets such as mortgages or loans, enhancing liquidity and risk distribution. Tranching segments these pooled securities into different layers or tranches, each with distinct risk and return profiles, catering to investors with varying risk appetites. Explore the mechanisms and benefits of securitization and tranching to understand their impact on modern finance.

Main Difference

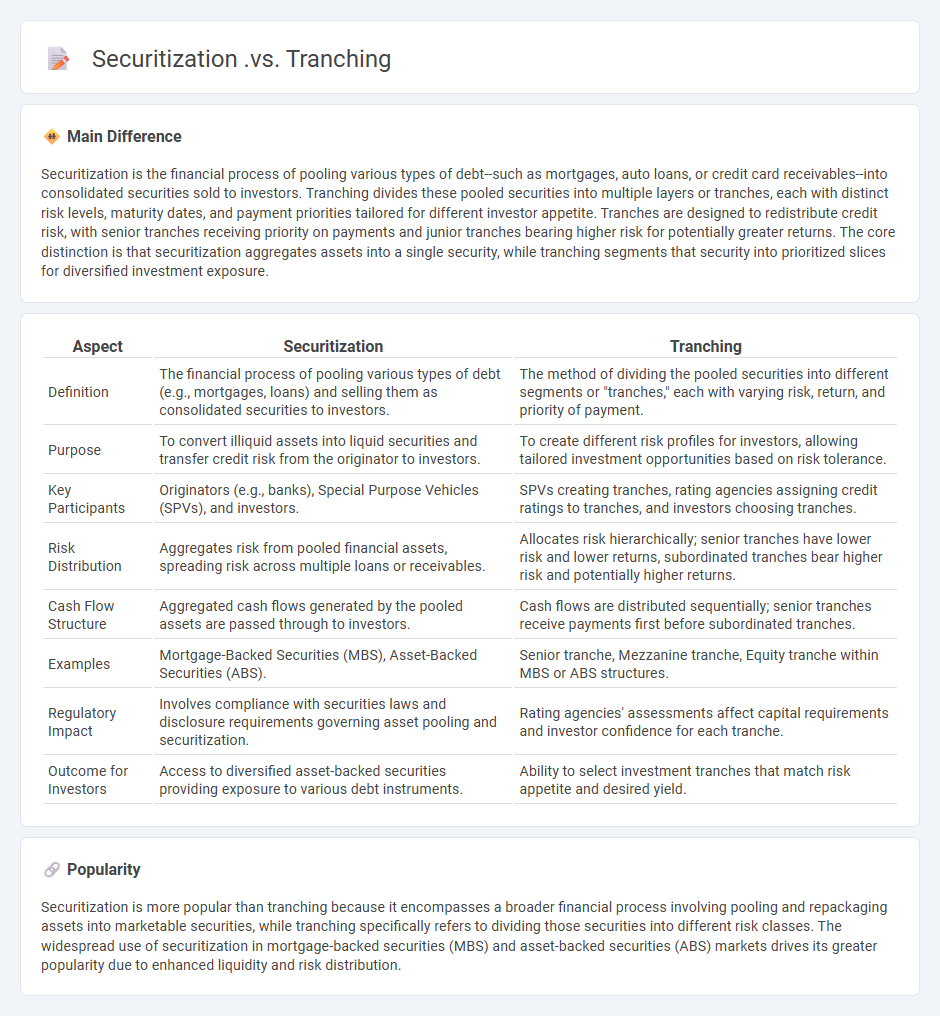

Securitization is the financial process of pooling various types of debt--such as mortgages, auto loans, or credit card receivables--into consolidated securities sold to investors. Tranching divides these pooled securities into multiple layers or tranches, each with distinct risk levels, maturity dates, and payment priorities tailored for different investor appetite. Tranches are designed to redistribute credit risk, with senior tranches receiving priority on payments and junior tranches bearing higher risk for potentially greater returns. The core distinction is that securitization aggregates assets into a single security, while tranching segments that security into prioritized slices for diversified investment exposure.

Connection

Securitization involves pooling various financial assets and converting them into marketable securities, which are then divided into tranches representing different levels of risk and return. Tranching is the process that segments these securities based on credit quality and payment priority, enabling investors to select exposure according to their risk appetite. This structure enhances liquidity and risk distribution in the financial markets by catering to diverse investor demands.

Comparison Table

| Aspect | Securitization | Tranching |

|---|---|---|

| Definition | The financial process of pooling various types of debt (e.g., mortgages, loans) and selling them as consolidated securities to investors. | The method of dividing the pooled securities into different segments or "tranches," each with varying risk, return, and priority of payment. |

| Purpose | To convert illiquid assets into liquid securities and transfer credit risk from the originator to investors. | To create different risk profiles for investors, allowing tailored investment opportunities based on risk tolerance. |

| Key Participants | Originators (e.g., banks), Special Purpose Vehicles (SPVs), and investors. | SPVs creating tranches, rating agencies assigning credit ratings to tranches, and investors choosing tranches. |

| Risk Distribution | Aggregates risk from pooled financial assets, spreading risk across multiple loans or receivables. | Allocates risk hierarchically; senior tranches have lower risk and lower returns, subordinated tranches bear higher risk and potentially higher returns. |

| Cash Flow Structure | Aggregated cash flows generated by the pooled assets are passed through to investors. | Cash flows are distributed sequentially; senior tranches receive payments first before subordinated tranches. |

| Examples | Mortgage-Backed Securities (MBS), Asset-Backed Securities (ABS). | Senior tranche, Mezzanine tranche, Equity tranche within MBS or ABS structures. |

| Regulatory Impact | Involves compliance with securities laws and disclosure requirements governing asset pooling and securitization. | Rating agencies' assessments affect capital requirements and investor confidence for each tranche. |

| Outcome for Investors | Access to diversified asset-backed securities providing exposure to various debt instruments. | Ability to select investment tranches that match risk appetite and desired yield. |

Asset Pooling

Asset pooling in finance involves combining multiple financial assets into a single portfolio to diversify risk and enhance returns. Commonly used in mutual funds, exchange-traded funds (ETFs), and pension funds, this strategy allows investors to access a broader range of securities with lower individual exposure. By aggregating assets like stocks, bonds, or real estate, asset pooling facilitates better risk management and improved liquidity. The method leverages economies of scale, reducing transaction costs and enhancing investment efficiency.

Risk Distribution

Risk distribution in finance involves spreading exposure across various asset classes, sectors, and geographic regions to minimize the impact of adverse events on a portfolio. Diversification strategies include allocating investments in stocks, bonds, real estate, and alternative assets to balance risk and return. Quantitative models like Value at Risk (VaR) and stress testing assess the potential losses under different scenarios, helping optimize risk allocation. Effective risk distribution enhances portfolio resilience and supports long-term financial stability.

Credit Enhancement

Credit enhancement improves the credit profile of financial instruments by reducing the risk of default and increasing investor confidence. Techniques include collateralization, third-party guarantees, and reserve funds, which help secure better credit ratings from agencies such as Moody's and Standard & Poor's. This process enables issuers to achieve lower borrowing costs and broader market access. Structured finance products, such as mortgage-backed securities, often rely on credit enhancement to attract investment.

Payment Waterfall

Payment waterfall structures allocate cash flow priority among multiple classes of creditors and stakeholders in finance, ensuring systematic distribution according to predefined seniority. This hierarchical framework directs incoming payments first toward senior debt obligations, followed by mezzanine instruments, and finally equity holders, minimizing default risk and optimizing capital recovery. Commonly used in structured finance, project financing, and securitizations, payment waterfalls enhance transparency and predictability of returns for investors. Precise modeling of payment waterfalls supports effective risk management and compliance with contractual covenants.

Security Classes

Security classes in finance categorize financial instruments based on risk, return, and ownership rights, including equity securities, debt securities, and hybrid securities. Equity securities, such as common and preferred stocks, represent ownership stakes and typically offer dividend payments along with capital appreciation potential. Debt securities encompass bonds, debentures, and notes, characterized by fixed interest payments and priority claims over assets during liquidation. Hybrid securities, like convertible bonds and mezzanine financing, blend features of both equity and debt, providing flexible investment options depending on market conditions.

Source and External Links

Securitization - Columbia University - Securitization is the process of pooling financial assets and issuing securities backed by these assets, while tranching involves dividing these securities into segments with varying risk exposures and priorities of payment.

Securitization and tranched credit products - Securitization refers to the overall structuring and transformation of asset pools into securities, whereas tranching is the subdivision of that securitized pool into different classes or tranches that absorb losses and receive cash flows in a specified order.

Fixed-Income Securitization - PrepNuggets - Securitization creates a special purpose vehicle to hold transferred assets and issue securities, while tranching stratifies those securities by credit risk and payment priority, with senior tranches having the highest claim and lowest risk, and subordinated tranches taking the first credit losses but offering higher yields.

FAQs

What is securitization?

Securitization is the financial process of pooling various types of debt--such as mortgages, auto loans, or credit card debt--and converting them into marketable securities that investors can buy and trade.

What is tranching in finance?

Tranching in finance refers to dividing a pool of financial assets, such as loans or securities, into distinct layers called tranches that vary by risk level, maturity, and interest rates to appeal to different investor preferences.

How does securitization work?

Securitization involves pooling various financial assets like loans or mortgages, converting them into tradable securities, and selling them to investors to raise capital and transfer risk from the originator.

How are tranches created in securitization?

Tranches in securitization are created by segmenting pooled financial assets into different layers based on risk, maturity, and priority of payment to match investor preferences and credit ratings.

What is the purpose of tranching?

The purpose of tranching is to divide a financial product, such as a mortgage-backed security or collateralized debt obligation, into multiple segments with varying risk levels, maturities, and returns to attract different types of investors and optimize capital structure.

How do investors benefit from different tranches?

Investors benefit from different tranches by accessing varied risk and return profiles, allowing them to choose investments that match their risk tolerance and income preferences.

What are the key differences between securitization and tranching?

Securitization involves pooling financial assets to create marketable securities, while tranching divides these securities into layers with varying risk and return profiles.