Mudharabah is an Islamic finance partnership where one party provides capital while the other manages the business, sharing profits according to a pre-agreed ratio, with losses borne solely by the capital provider. Musyarakah involves all partners contributing capital and sharing profits and losses proportionally based on their investment. Explore the detailed differences and applications of Mudharabah and Musyarakah to understand their unique roles in Shariah-compliant financing.

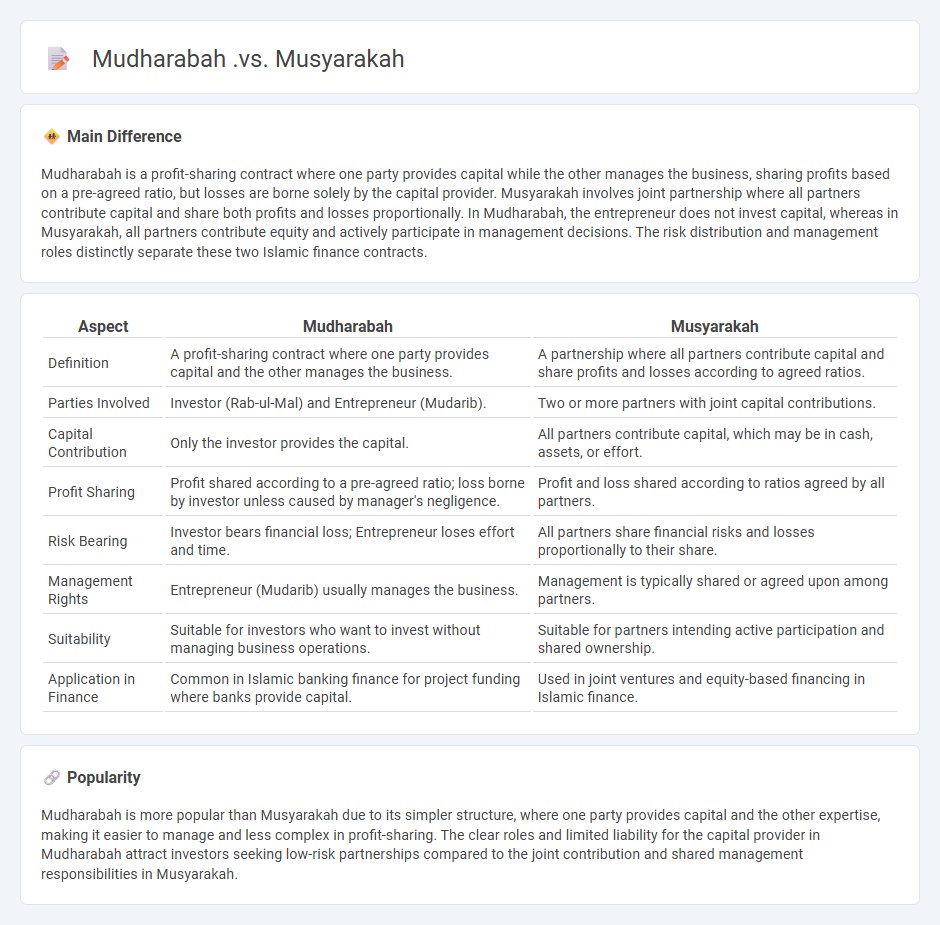

Main Difference

Mudharabah is a profit-sharing contract where one party provides capital while the other manages the business, sharing profits based on a pre-agreed ratio, but losses are borne solely by the capital provider. Musyarakah involves joint partnership where all partners contribute capital and share both profits and losses proportionally. In Mudharabah, the entrepreneur does not invest capital, whereas in Musyarakah, all partners contribute equity and actively participate in management decisions. The risk distribution and management roles distinctly separate these two Islamic finance contracts.

Connection

Mudharabah and Musyarakah are Islamic finance contracts based on profit-sharing principles rooted in Sharia law. Mudharabah involves a partnership where one party provides capital and the other offers expertise, sharing profits according to a pre-agreed ratio. Musyarakah entails a joint venture where all partners contribute capital and manage the business together, sharing profits and losses proportionally.

Comparison Table

| Aspect | Mudharabah | Musyarakah |

|---|---|---|

| Definition | A profit-sharing contract where one party provides capital and the other manages the business. | A partnership where all partners contribute capital and share profits and losses according to agreed ratios. |

| Parties Involved | Investor (Rab-ul-Mal) and Entrepreneur (Mudarib). | Two or more partners with joint capital contributions. |

| Capital Contribution | Only the investor provides the capital. | All partners contribute capital, which may be in cash, assets, or effort. |

| Profit Sharing | Profit shared according to a pre-agreed ratio; loss borne by investor unless caused by manager's negligence. | Profit and loss shared according to ratios agreed by all partners. |

| Risk Bearing | Investor bears financial loss; Entrepreneur loses effort and time. | All partners share financial risks and losses proportionally to their share. |

| Management Rights | Entrepreneur (Mudarib) usually manages the business. | Management is typically shared or agreed upon among partners. |

| Suitability | Suitable for investors who want to invest without managing business operations. | Suitable for partners intending active participation and shared ownership. |

| Application in Finance | Common in Islamic banking finance for project funding where banks provide capital. | Used in joint ventures and equity-based financing in Islamic finance. |

Profit and Loss Sharing (PLS)

Profit and Loss Sharing (PLS) is a financial mechanism where parties share both profits and risks from investments, commonly used in Islamic finance to comply with Sharia law prohibiting interest (riba). PLS models like Mudarabah and Musharakah enable equitable risk distribution between capital providers and entrepreneurs, fostering ethical investment practices. This system enhances transparency and aligns stakeholders' interests toward business success, promoting sustainable economic growth. Financial institutions incorporating PLS report improved asset quality and increased customer trust in markets valuing risk-sharing frameworks.

Capital Contribution

Capital contribution refers to the funds or assets that investors or owners provide to a company to finance its operations, growth, or acquisitions. These contributions increase the company's equity and are recorded in the shareholders' equity section of the balance sheet under common stock or additional paid-in capital. In startups, capital contributions often come from founders, venture capitalists, or angel investors as initial seed money or subsequent funding rounds. Regulatory frameworks such as GAAP and IFRS require clear disclosure of capital contributions to maintain transparency and protect stakeholders.

Management Participation

Management participation in finance refers to the active involvement of company executives and managers in financial decision-making processes, including budgeting, investment strategies, and capital allocation. Studies show that high levels of management participation correlate with improved financial performance and enhanced shareholder value due to better-informed decisions and alignment of management goals with company objectives. This approach often includes equity participation through stock options or profit-sharing plans, incentivizing managers to focus on long-term growth and risk management. Data from firms with strong management participation exhibit higher return on equity (ROE) and increased market competitiveness.

Risk Allocation

Risk allocation in finance involves distributing potential risks among parties involved in a financial transaction or investment to minimize individual exposure. Effective risk allocation enhances portfolio diversification, reducing the impact of market volatility on overall returns. Financial instruments such as derivatives, insurance contracts, and hedging strategies are commonly utilized to manage and transfer risks. Institutional investors, including pension funds and hedge funds, rely heavily on precise risk allocation to optimize asset performance and safeguard capital.

Practical Use Cases

Artificial intelligence powers fraud detection systems by analyzing transaction patterns to identify anomalies in real-time, significantly reducing financial losses. Robo-advisors leverage machine learning algorithms to provide personalized investment recommendations, optimizing portfolio management based on individual risk tolerance and market data. Credit scoring models utilize vast datasets to improve accuracy in predicting borrower reliability, enhancing lending decisions. Automated compliance tools streamline regulatory reporting and risk assessment, ensuring adherence to evolving financial regulations.

Source and External Links

Here are three concise comparisons between Mudharabah and Musyarakah:Understanding Islamic Banking - Mudharabah involves one party providing capital and the other managing, with profits shared based on agreements, while Musyarakah is a partnership where all parties contribute capital and share both profits and losses.

Differences between Musharakah and Mudarabah - In Musyarakah, all partners are agents and guarantors for each other and participate in management, whereas Mudharabah restricts the capital provider's active participation in business operations.

Comparative Analysis between Musyarakah and Mudharabah - Musyarakah shares both profits and risks proportionally among partners, while Mudharabah places the main business risk on the capital provider.

FAQs

What do Mudharabah and Musyarakah mean?

Mudharabah refers to a profit-sharing partnership where one party provides capital and the other manages the business, while Musyarakah is a joint venture where all partners contribute capital and share profits and losses according to their equity.

How do Mudharabah and Musyarakah differ in structure?

Mudharabah involves one party providing capital while the other manages the business, sharing profits based on a pre-agreed ratio, with the capital provider bearing losses; Musyarakah is a partnership where all partners contribute capital and participate in management, sharing profits and losses proportionally.

Who provides capital in Mudharabah and Musyarakah?

In Mudharabah, the capital is provided solely by the Rab al-Mal (investor). In Musyarakah, all partners contribute capital either in cash or assets.

How are profits and losses shared in Mudharabah vs Musyarakah?

In Mudharabah, profits are shared according to a pre-agreed ratio while losses are borne entirely by the capital provider; in Musyarakah, both profits and losses are shared proportionally based on each partner's capital contribution.

Which risks are involved in Mudharabah compared to Musyarakah?

Mudharabah involves risk primarily borne by the capital provider who bears all losses if the entrepreneur defaults, while the entrepreneur loses only effort and time; Musyarakah involves shared risks and losses proportionate to each partner's capital contribution.

What are the typical uses for Mudharabah and Musyarakah?

Mudharabah is typically used for profit-sharing investment ventures where one party provides capital and the other manages the business, ideal for capital financing and investment projects. Musyarakah is commonly employed for joint partnership ventures where all partners contribute capital and share profits and losses, frequently used in business collaborations, real estate development, and financial partnerships.

Why are both Mudharabah and Musyarakah important in Islamic finance?

Mudharabah and Musyarakah are important in Islamic finance because they facilitate profit-and-loss sharing, align stakeholder interests, comply with Shariah principles prohibiting interest (riba), and promote ethical, risk-sharing partnerships in investment and business ventures.