Value at Risk (VaR) estimates the maximum potential loss in a portfolio over a specified time frame at a given confidence level, serving as a key risk assessment metric in finance. Conditional Value at Risk (CVaR), also known as Expected Shortfall, provides the expected loss exceeding the VaR threshold, offering deeper insight into tail risk and extreme market scenarios. Explore further to understand how these risk measures compare and enhance portfolio risk management strategies.

Main Difference

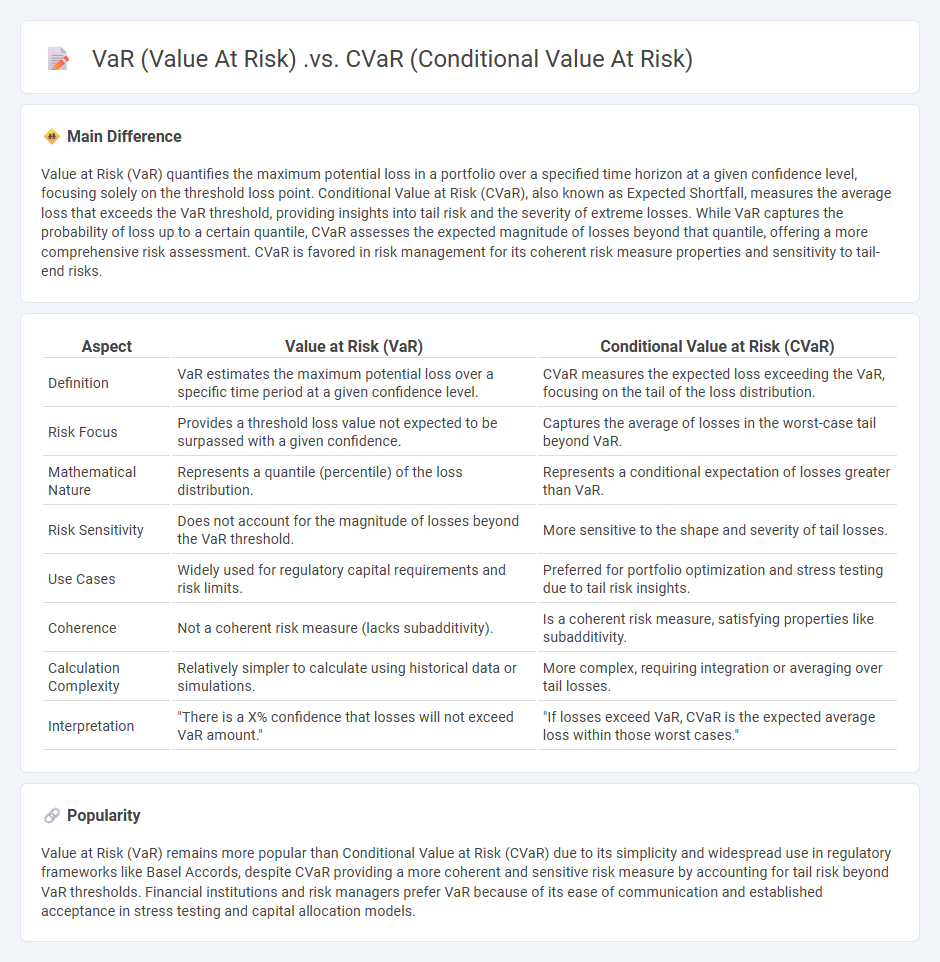

Value at Risk (VaR) quantifies the maximum potential loss in a portfolio over a specified time horizon at a given confidence level, focusing solely on the threshold loss point. Conditional Value at Risk (CVaR), also known as Expected Shortfall, measures the average loss that exceeds the VaR threshold, providing insights into tail risk and the severity of extreme losses. While VaR captures the probability of loss up to a certain quantile, CVaR assesses the expected magnitude of losses beyond that quantile, offering a more comprehensive risk assessment. CVaR is favored in risk management for its coherent risk measure properties and sensitivity to tail-end risks.

Connection

Value at Risk (VaR) quantifies the maximum expected loss over a specified time frame at a given confidence level, serving as a threshold for potential portfolio risk. Conditional Value at Risk (CVaR) extends this by calculating the average loss exceeding the VaR threshold, providing insight into tail risk beyond the VaR cutoff. Both metrics are integral to risk management, with CVaR offering a more comprehensive view of extreme losses in financial portfolios.

Comparison Table

| Aspect | Value at Risk (VaR) | Conditional Value at Risk (CVaR) |

|---|---|---|

| Definition | VaR estimates the maximum potential loss over a specific time period at a given confidence level. | CVaR measures the expected loss exceeding the VaR, focusing on the tail of the loss distribution. |

| Risk Focus | Provides a threshold loss value not expected to be surpassed with a given confidence. | Captures the average of losses in the worst-case tail beyond VaR. |

| Mathematical Nature | Represents a quantile (percentile) of the loss distribution. | Represents a conditional expectation of losses greater than VaR. |

| Risk Sensitivity | Does not account for the magnitude of losses beyond the VaR threshold. | More sensitive to the shape and severity of tail losses. |

| Use Cases | Widely used for regulatory capital requirements and risk limits. | Preferred for portfolio optimization and stress testing due to tail risk insights. |

| Coherence | Not a coherent risk measure (lacks subadditivity). | Is a coherent risk measure, satisfying properties like subadditivity. |

| Calculation Complexity | Relatively simpler to calculate using historical data or simulations. | More complex, requiring integration or averaging over tail losses. |

| Interpretation | "There is a X% confidence that losses will not exceed VaR amount." | "If losses exceed VaR, CVaR is the expected average loss within those worst cases." |

Value at Risk (VaR)

Value at Risk (VaR) quantifies the potential loss in value of a portfolio or asset over a defined period for a given confidence interval, commonly 95% or 99%. Financial institutions use VaR to measure market risk, estimating the maximum expected loss under normal market conditions. Methods for calculating VaR include historical simulation, variance-covariance, and Monte Carlo simulation, each varying in complexity and assumptions. Regulators, such as the Basel Committee on Banking Supervision, often require banks to report VaR as part of risk management frameworks.

Conditional Value at Risk (CVaR)

Conditional Value at Risk (CVaR) quantifies the expected loss exceeding the Value at Risk (VaR) threshold, offering a more comprehensive risk assessment in finance. CVaR is widely used for portfolio optimization and risk management, especially under extreme market conditions. It incorporates tail risk by averaging losses in the worst a% scenarios, typically calculated using historical simulation or Monte Carlo methods. Regulatory frameworks, including Basel III, emphasize CVaR for stress testing financial institutions' capital adequacy.

Tail Risk

Tail risk refers to the probability of rare events that result in extreme negative outcomes within a financial portfolio, typically beyond three standard deviations from the mean in a normal distribution. This risk significantly impacts asset prices, especially during market crashes or financial crises, such as the 2008 global financial collapse. Investors often mitigate tail risk through hedging strategies including options, value-at-risk (VaR) models, and stress testing scenarios to assess potential losses. Understanding tail risk is critical for portfolio management and regulatory frameworks aimed at minimizing systemic financial instability.

Loss Distribution

Loss distribution in finance quantifies the probability and magnitude of potential losses within a portfolio or investment. It is a critical component of risk management, enabling institutions to estimate Value at Risk (VaR) and Conditional Value at Risk (CVaR) effectively. Key models for loss distribution include the binomial, Poisson, and heavy-tailed distributions like Pareto or lognormal, which capture extreme loss events. Accurate loss distribution modeling supports regulatory compliance and strategic capital allocation under frameworks such as Basel III.

Risk Management

Risk management in finance involves identifying, assessing, and prioritizing financial risks to minimize potential losses and maximize returns. Techniques such as diversification, hedging, and the use of derivatives help mitigate market, credit, and operational risks. Financial institutions rely on quantitative models and regulatory frameworks like Basel III to ensure capital adequacy and liquidity management. Effective risk management supports stable financial performance and compliance with industry standards.

Source and External Links

Conditional Value at Risk: CVaR vs: VaR: A Comparative Analysis - VaR measures the maximum loss at a given confidence level, while CVaR quantifies the average loss exceeding the VaR threshold, capturing tail risk more comprehensively.

CVaR vs: VaR: Which Risk Measure Should You Use - VaR is a quantile-based, easier-to-calculate measure not coherent in portfolio diversification, whereas CVaR is an expected-value-based, coherent risk measure that better captures extreme losses and encourages diversification.

Value-at-Risk vs. Conditional Value-at-Risk in Risk Management and Optimization - The choice between VaR and CVaR depends on mathematical properties, stability of estimates, and regulatory acceptance; CVaR offers advantages in optimization and risk management despite its computational complexity.