Modigliani-Miller Proposition I asserts that a firm's value is unaffected by its capital structure in perfect markets, emphasizing capital structure irrelevance. Proposition II introduces the impact of financial leverage on a company's cost of equity, showing that increased debt raises equity risk and cost. Explore further to understand how these foundational theories shape modern corporate finance decisions.

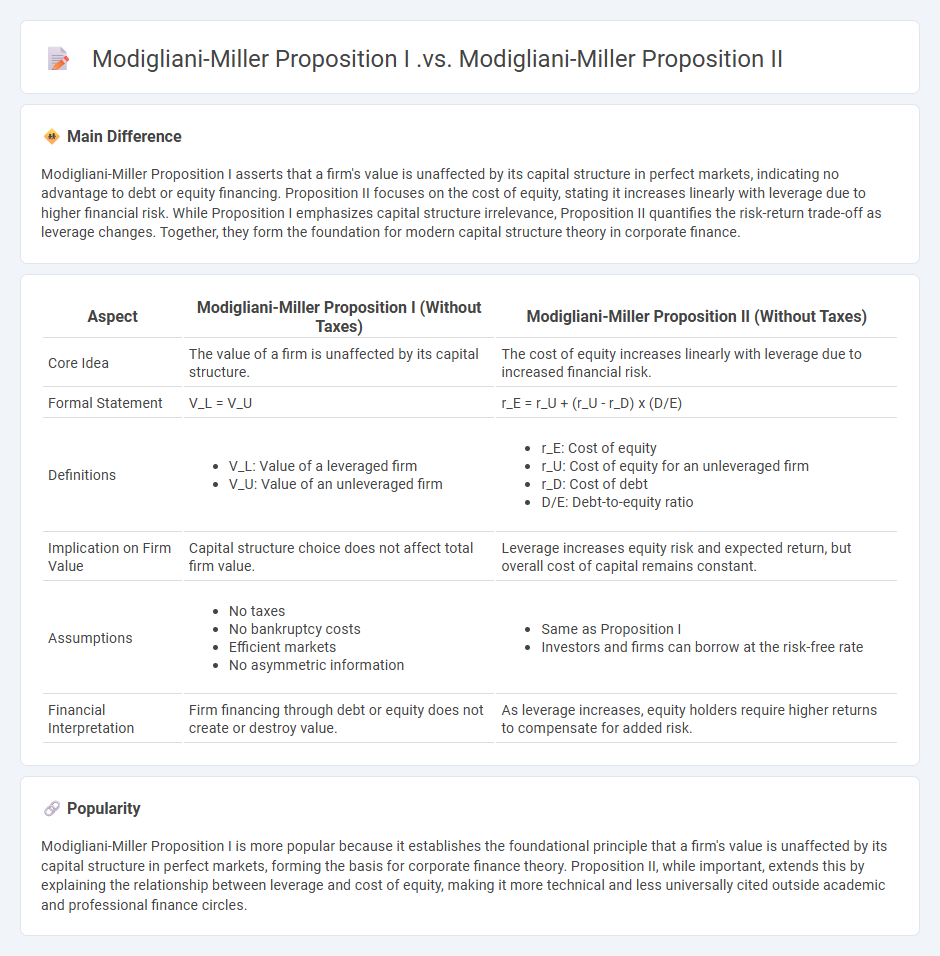

Main Difference

Modigliani-Miller Proposition I asserts that a firm's value is unaffected by its capital structure in perfect markets, indicating no advantage to debt or equity financing. Proposition II focuses on the cost of equity, stating it increases linearly with leverage due to higher financial risk. While Proposition I emphasizes capital structure irrelevance, Proposition II quantifies the risk-return trade-off as leverage changes. Together, they form the foundation for modern capital structure theory in corporate finance.

Connection

Modigliani-Miller Proposition I establishes that a firm's value is unaffected by its capital structure in perfect markets, while Proposition II builds on this by illustrating how the cost of equity increases linearly with leverage due to higher financial risk. The connection lies in Proposition I's assumption that total firm value remains constant, which underpins Proposition II's derivation of the weighted average cost of capital (WACC) and its relationship with leverage and equity cost. Together, these propositions provide a foundational framework for understanding the trade-offs between debt and equity financing in corporate finance.

Comparison Table

| Aspect | Modigliani-Miller Proposition I (Without Taxes) | Modigliani-Miller Proposition II (Without Taxes) |

|---|---|---|

| Core Idea | The value of a firm is unaffected by its capital structure. | The cost of equity increases linearly with leverage due to increased financial risk. |

| Formal Statement | V_L = V_U | r_E = r_U + (r_U - r_D) x (D/E) |

| Definitions |

|

|

| Implication on Firm Value | Capital structure choice does not affect total firm value. | Leverage increases equity risk and expected return, but overall cost of capital remains constant. |

| Assumptions |

|

|

| Financial Interpretation | Firm financing through debt or equity does not create or destroy value. | As leverage increases, equity holders require higher returns to compensate for added risk. |

Capital Structure

Capital structure refers to the specific mix of debt and equity that a company uses to finance its operations and growth. A well-balanced capital structure minimizes the cost of capital while maximizing shareholder value, typically involving a combination of long-term debt, preferred stock, and common equity. Companies in different industries maintain varied capital structures; for example, utility firms often have higher debt ratios due to steady cash flows, whereas tech companies may rely more heavily on equity. Optimizing capital structure requires careful analysis of market conditions, interest rates, and tax implications to achieve financial stability and growth.

Firm Value

Firm value represents the total worth of a company, reflecting its market capitalization plus the value of its debt and any cash reserves. It serves as a critical indicator for investors assessing the company's financial health, growth potential, and risk profile. Key components influencing firm value include revenue streams, cash flow stability, capital structure, and future earnings potential. Accurate valuation methods such as discounted cash flow (DCF) analysis and comparables enhance investment decisions and corporate finance strategies.

Cost of Equity

Cost of equity represents the return a company must offer investors to compensate for the risk of owning its stock. It is a critical component in calculating the weighted average cost of capital (WACC) and is often estimated using models such as the Capital Asset Pricing Model (CAPM). The CAPM formula calculates cost of equity by adding the risk-free rate to the product of the stock's beta and the equity market risk premium. Accurate assessment of the cost of equity helps firms make informed decisions about capital budgeting and financing strategies.

Weighted Average Cost of Capital (WACC)

Weighted Average Cost of Capital (WACC) represents a firm's average after-tax cost of capital from all sources, including equity, debt, and preferred stock. It is calculated by weighting the cost of each capital component according to its proportion in the overall capital structure. WACC serves as a critical discount rate in financial modeling and investment valuation, influencing decisions on project feasibility and corporate financial strategy. Accurate WACC estimation incorporates market value data, tax rates, and the risk profiles of different funding sources.

Financial Leverage

Financial leverage measures the use of borrowed funds to increase a company's investment capacity and potential return on equity. It is calculated by the ratio of total debt to shareholders' equity, indicating the degree to which a firm relies on debt financing. High financial leverage can amplify profits but also increases the risk of insolvency during downturns. Key metrics like the debt-to-equity ratio and interest coverage ratio provide insights into leverage levels and financial risk.

Source and External Links

M&M Theorem - Overview, Assumptions, Propositions - Modigliani-Miller Proposition I states that the capital structure of a company does not affect its overall value in a perfect market with no taxes or bankruptcy costs, while Proposition II states that the cost of equity increases linearly with leverage, reflecting increased financial risk as debt level rises.

Modigliani-Miller Proposition II | CFA Level 1 - Proposition II refines the theorem by stating that the company's cost of equity rises as the company takes on more debt, to maintain a constant weighted average cost of capital (WACC), highlighting how financial risk affects equity returns.

Handout 13: MM Propositions I and II (Case with No Taxes) - Proposition I asserts firm value is independent of debt/equity ratio, while Proposition II formally expresses the cost of equity as increasing with leverage: \( r_E = r_0 + \frac{D}{E}(r_0 - r_D) \), where \(r_0\) is the cost of capital for an all-equity firm.

FAQs

What is the Modigliani-Miller Proposition I?

Modigliani-Miller Proposition I states that in a perfect market without taxes, bankruptcy costs, or asymmetric information, a firm's value is independent of its capital structure.

What is the Modigliani-Miller Proposition II?

Modigliani-Miller Proposition II states that a firm's cost of equity increases linearly with its debt-to-equity ratio, reflecting the higher financial risk borne by equity holders as leverage rises, while the overall weighted average cost of capital (WACC) remains constant in a perfect market without taxes.

How does Proposition I differ from Proposition II?

Proposition I establishes foundational principles, while Proposition II extends or applies those principles to specific cases or conditions.

What assumptions underlie both propositions?

Both propositions assume a shared foundational premise or commonly accepted truth.

How do these propositions impact capital structure decisions?

These propositions influence capital structure decisions by guiding the optimal mix of debt and equity to minimize cost of capital, balance financial risk, and maximize firm value.

What are the practical implications of Proposition I?

Proposition I states that the value of a levered firm equals the value of an unlevered firm plus the present value of the tax shield on debt, implying that firms can increase their value by using debt to benefit from tax deductions on interest payments.

What are the practical implications of Proposition II?

Proposition II implies that a firm's cost of equity increases as its debt-to-equity ratio increases, reflecting higher financial risk for equity holders.