A syndicated loan involves multiple lenders pooling resources to provide a large loan to a single borrower, spreading the risk among participants. In contrast, a bilateral loan consists of a single lender and borrower, offering a more straightforward, often faster negotiation process. Explore the differences to understand which financing option best suits your business needs.

Main Difference

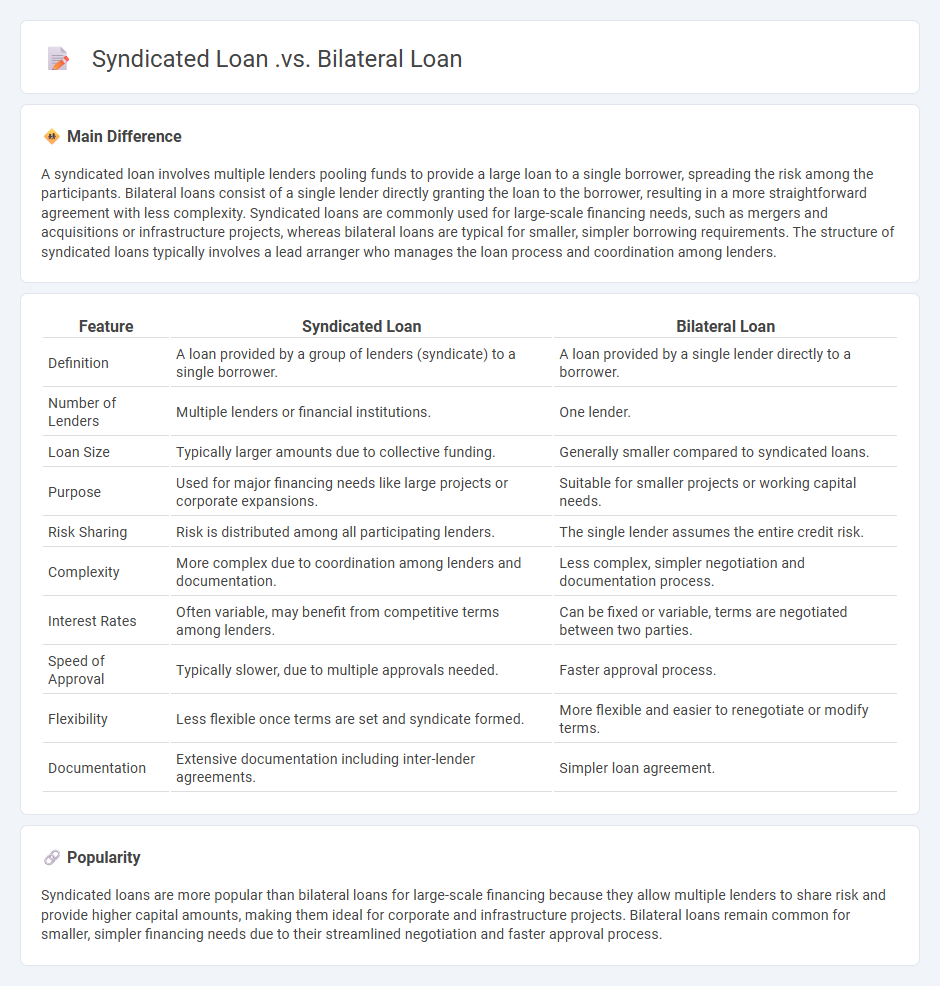

A syndicated loan involves multiple lenders pooling funds to provide a large loan to a single borrower, spreading the risk among the participants. Bilateral loans consist of a single lender directly granting the loan to the borrower, resulting in a more straightforward agreement with less complexity. Syndicated loans are commonly used for large-scale financing needs, such as mergers and acquisitions or infrastructure projects, whereas bilateral loans are typical for smaller, simpler borrowing requirements. The structure of syndicated loans typically involves a lead arranger who manages the loan process and coordination among lenders.

Connection

Syndicated loans and bilateral loans are connected through their shared purpose of providing debt financing to borrowers, with syndicated loans involving multiple lenders pooling resources while bilateral loans involve a single lender-borrower relationship. Syndicated loans offer larger capital than bilateral loans due to the collective financing from participating banks or financial institutions. Both loan types affect credit risk assessment and loan structuring, influencing borrower leverage and funding strategies.

Comparison Table

| Feature | Syndicated Loan | Bilateral Loan |

|---|---|---|

| Definition | A loan provided by a group of lenders (syndicate) to a single borrower. | A loan provided by a single lender directly to a borrower. |

| Number of Lenders | Multiple lenders or financial institutions. | One lender. |

| Loan Size | Typically larger amounts due to collective funding. | Generally smaller compared to syndicated loans. |

| Purpose | Used for major financing needs like large projects or corporate expansions. | Suitable for smaller projects or working capital needs. |

| Risk Sharing | Risk is distributed among all participating lenders. | The single lender assumes the entire credit risk. |

| Complexity | More complex due to coordination among lenders and documentation. | Less complex, simpler negotiation and documentation process. |

| Interest Rates | Often variable, may benefit from competitive terms among lenders. | Can be fixed or variable, terms are negotiated between two parties. |

| Speed of Approval | Typically slower, due to multiple approvals needed. | Faster approval process. |

| Flexibility | Less flexible once terms are set and syndicate formed. | More flexible and easier to renegotiate or modify terms. |

| Documentation | Extensive documentation including inter-lender agreements. | Simpler loan agreement. |

Loan Structure

Loan structure defines the specific terms and conditions of a loan, including principal amount, interest rate, repayment schedule, and maturity date. It incorporates fixed or variable interest rates, amortization methods, and covenants that protect lenders' interests. Effective loan structuring balances borrower capacity with lender risk, influencing cash flow management and creditworthiness evaluation. Financial institutions use detailed models and credit analysis to customize loan packages for diverse borrower profiles.

Lender Composition

Lender composition in finance refers to the diverse mix of institutions and individuals providing capital in a financial market or institution's loan portfolio. This composition typically includes commercial banks, credit unions, mortgage companies, insurance firms, hedge funds, and private equity firms, each possessing unique lending criteria and risk appetites. A balanced lender composition enhances financial stability by distributing risk and ensuring competitive loan pricing. Analysis of lender composition aids regulators and investors in assessing credit availability and systemic risk within the financial ecosystem.

Documentation Complexity

Documentation complexity in finance often arises from regulatory compliance requirements, intricate financial instruments, and multi-jurisdictional transactions. High complexity can lead to increased operational risks, longer processing times, and elevated costs for financial institutions. Automated document management systems leveraging artificial intelligence and natural language processing can significantly reduce errors and enhance efficiency. Effective handling of financial documentation complexity improves transparency and supports audit readiness in dynamic regulatory environments.

Negotiation Process

The negotiation process in finance involves strategic communication between parties to reach mutually beneficial agreements on transactions such as mergers, acquisitions, loans, or investment terms. Key stages include preparation, where financial data and valuation metrics are analyzed, followed by the exchange of offers and counteroffers based on due diligence findings. Effective negotiation requires understanding market conditions, regulatory frameworks, and risk assessments to optimize financial outcomes. Employing tactics like anchoring, BATNA (Best Alternative to a Negotiated Agreement), and concession management enhances agreement quality in high-stakes financial deals.

Flexibility

Flexibility in finance refers to the ability of companies or individuals to adapt their financial strategies and decisions in response to changing market conditions, economic shifts, or unexpected expenses. This includes maintaining liquid assets, accessing diverse funding sources, and structuring debt with adjustable terms to manage risk effectively. Financial flexibility supports sustained growth and stability by enabling prompt responses to investment opportunities or financial downturns. Key measures often include cash reserves, credit lines, and low fixed-cost commitments.

Source and External Links

Bilateral Loans vs. Syndicated Loans: Which One Is Right for You? - This article compares bilateral and syndicated loans, highlighting that bilateral loans offer more flexibility and faster negotiations, while syndicated loans provide larger funding by distributing risk among multiple lenders.

Bilateral vs. Syndicated Lending: Which is Right for Your Business? - This piece discusses the differences between bilateral and syndicated lending, emphasizing that bilateral loans are simpler and more customizable, while syndicated loans are complex but offer larger funding options.

Syndicated Credit and Bilateral Lines Complement Each Other - This article explains how syndicated and bilateral loans can complement each other in a financing strategy, with syndicated loans providing larger amounts and bilateral lines offering flexibility and simplicity in management.

FAQs

What is a syndicated loan?

A syndicated loan is a large loan provided by a group of lenders, called a syndicate, to a single borrower, distributing the risk among multiple financial institutions.

What is a bilateral loan?

A bilateral loan is a debt agreement between one borrower and one lender, typically a bank or financial institution.

How do syndicated loans differ from bilateral loans?

Syndicated loans involve multiple lenders sharing a single loan to a borrower, distributing risk and pooling large capital, whereas bilateral loans involve a single lender providing funds directly to the borrower.

What are the advantages of a syndicated loan?

A syndicated loan offers advantages such as risk diversification among multiple lenders, access to larger loan amounts, potential for lower borrowing costs, simplified loan management under a single agreement, and enhanced credibility for the borrower.

What are the benefits of a bilateral loan?

A bilateral loan offers benefits such as streamlined negotiation, faster approval, customized terms, lower costs, and strengthened lender-borrower relationships.

Who are the typical participants in a syndicated loan?

Typical participants in a syndicated loan include the lead arranger or agent bank, participating banks or lenders, the borrower, and sometimes other financial institutions such as institutional investors or credit funds.

When is a syndicated loan preferred over a bilateral loan?

A syndicated loan is preferred over a bilateral loan when a borrower requires a large loan amount that exceeds the capacity of a single lender or seeks risk diversification among multiple lenders.