Forward contracts are customized agreements between two parties to buy or sell an asset at a specified future date and price, often used in over-the-counter (OTC) markets. Futures contracts are standardized, exchange-traded contracts that obligate the purchase or sale of an asset at a predetermined price and date, offering greater liquidity and reduced counterparty risk. Explore the detailed differences in terms, trading mechanisms, and risk management to better understand which contract suits your financial strategy.

Main Difference

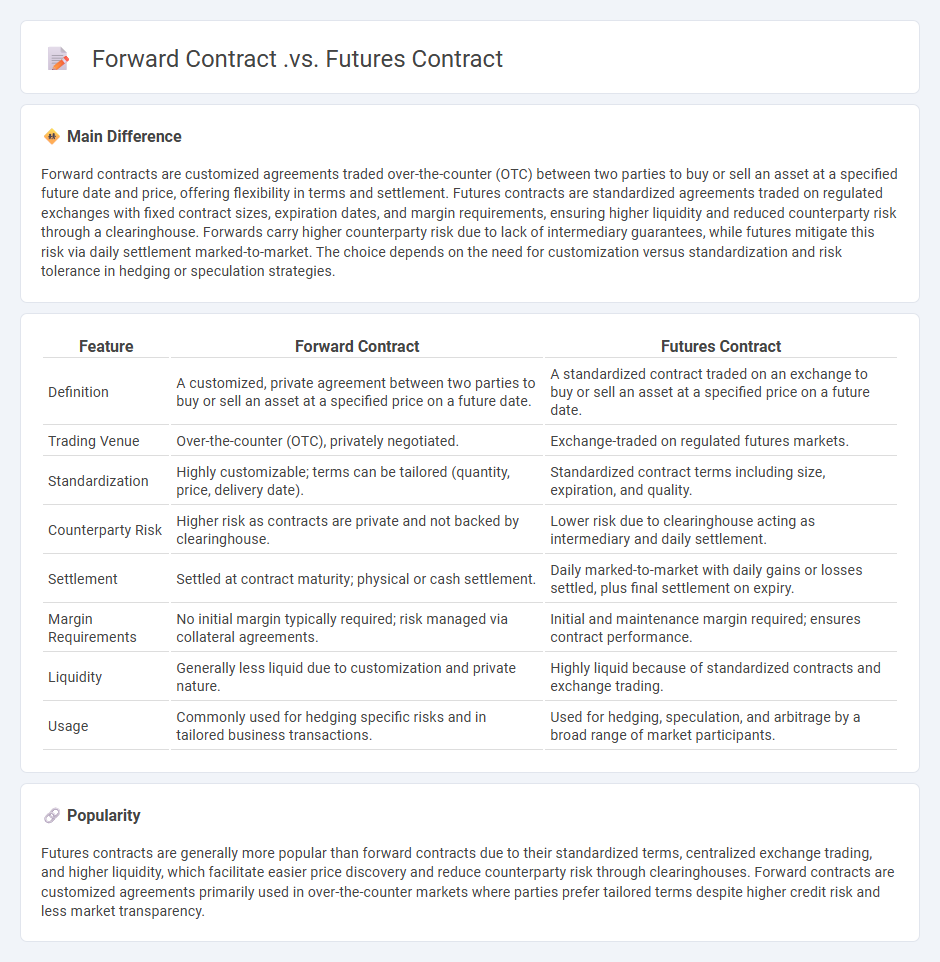

Forward contracts are customized agreements traded over-the-counter (OTC) between two parties to buy or sell an asset at a specified future date and price, offering flexibility in terms and settlement. Futures contracts are standardized agreements traded on regulated exchanges with fixed contract sizes, expiration dates, and margin requirements, ensuring higher liquidity and reduced counterparty risk through a clearinghouse. Forwards carry higher counterparty risk due to lack of intermediary guarantees, while futures mitigate this risk via daily settlement marked-to-market. The choice depends on the need for customization versus standardization and risk tolerance in hedging or speculation strategies.

Connection

Forward contracts and futures contracts are both derivatives that allow parties to buy or sell an asset at a predetermined price on a future date, effectively managing price risk. Forward contracts are customized agreements traded over-the-counter (OTC), while futures contracts are standardized and traded on regulated exchanges, providing greater liquidity and transparency. Both instruments serve hedging and speculative purposes in financial markets but differ primarily in terms of standardization, counterparty risk, and settlement procedures.

Comparison Table

| Feature | Forward Contract | Futures Contract |

|---|---|---|

| Definition | A customized, private agreement between two parties to buy or sell an asset at a specified price on a future date. | A standardized contract traded on an exchange to buy or sell an asset at a specified price on a future date. |

| Trading Venue | Over-the-counter (OTC), privately negotiated. | Exchange-traded on regulated futures markets. |

| Standardization | Highly customizable; terms can be tailored (quantity, price, delivery date). | Standardized contract terms including size, expiration, and quality. |

| Counterparty Risk | Higher risk as contracts are private and not backed by clearinghouse. | Lower risk due to clearinghouse acting as intermediary and daily settlement. |

| Settlement | Settled at contract maturity; physical or cash settlement. | Daily marked-to-market with daily gains or losses settled, plus final settlement on expiry. |

| Margin Requirements | No initial margin typically required; risk managed via collateral agreements. | Initial and maintenance margin required; ensures contract performance. |

| Liquidity | Generally less liquid due to customization and private nature. | Highly liquid because of standardized contracts and exchange trading. |

| Usage | Commonly used for hedging specific risks and in tailored business transactions. | Used for hedging, speculation, and arbitrage by a broad range of market participants. |

Standardization

Standardization in finance refers to the process of establishing uniform procedures, regulations, and reporting formats to ensure consistency and comparability across financial markets and institutions. Key examples include the International Financial Reporting Standards (IFRS), which harmonize accounting principles globally, and the use of standardized financial instruments such as derivatives contracts governed by the International Swaps and Derivatives Association (ISDA) master agreements. Standardization enhances transparency, reduces transaction costs, and facilitates efficient risk management by enabling investors and regulators to better analyze and compare financial data. Major financial centers like New York, London, and Tokyo rely heavily on standardized practices to support global capital flows and regulatory compliance.

Counterparty Risk

Counterparty risk in finance refers to the possibility that the other party involved in a financial transaction, such as a derivative contract, loan, or trade, may default on their contractual obligations. This risk is critical in over-the-counter (OTC) markets where transactions are customized and lack central clearinghouses. Financial institutions use credit risk assessment models and collateral requirements to mitigate counterparty risk exposure. Effective management of counterparty risk is essential for maintaining market stability and preventing systemic failures.

Settlement Method

Settlement method in finance refers to the process through which securities transactions are finalized by transferring ownership and payment between buyer and seller. Common settlement methods include delivery versus payment (DVP), where securities are exchanged only if payment occurs simultaneously, reducing counterparty risk. The standard settlement cycle for most equity trades in major markets like the NYSE and NASDAQ is T+2, meaning two business days after the trade date. Efficient settlement methods enhance market liquidity, minimize settlement risk, and ensure regulatory compliance.

Trading Venue

A trading venue refers to a marketplace where financial instruments such as stocks, bonds, derivatives, and commodities are bought and sold. Examples of prominent trading venues include stock exchanges like the New York Stock Exchange (NYSE), NASDAQ, and multinational platforms such as the London Stock Exchange (LSE). These venues provide regulated environments ensuring transparency, liquidity, and price discovery for market participants. Advances in technology have led to the rise of electronic trading venues and alternative trading systems (ATS), enhancing market access and execution speed.

Hedging and Speculation

Hedging in finance involves using financial instruments or market strategies to reduce the risk of adverse price movements in assets. Speculation aims to profit from price fluctuations by taking on higher risk, often through derivative contracts like options and futures. Both practices rely heavily on market analysis and risk management techniques to optimize returns and mitigate losses. Effective hedging and speculation strategies are essential for portfolio diversification and capital preservation in volatile markets.

Source and External Links

Forward contracts and futures: What's the difference? - Kraken - Forward contracts are private, customizable agreements traded OTC without margin requirements, while futures contracts are standardized, regulated, exchange-traded instruments requiring margins and daily settlement. Forward contracts carry higher counterparty risk and involve no middleman fees, whereas futures are highly regulated with fixed terms and exchange fees.

Futures Contracts Compared to Forwards - CME Group - Futures contracts trade on exchanges with standardized terms and no counterparty risk due to clearinghouses, whereas forward contracts are privately negotiated, customizable, and subject to credit risk. Futures are actively traded and regulated, forwards are not.

Futures vs. Forwards: Explaining the Differences | LiteFinance - Forward contracts are OTC private agreements used mainly by hedgers to reduce price volatility impact, whereas futures contracts are exchange-traded standardized agreements often used for speculation and are highly regulated. Futures have no private modification and are subject to government oversight, especially in the U.S.

FAQs

What is a forward contract?

A forward contract is a customized financial agreement between two parties to buy or sell an asset at a specified price on a future date.

What is a futures contract?

A futures contract is a standardized legal agreement to buy or sell a specific quantity of a commodity or financial instrument at a predetermined price on a specified future date.

How do forward and futures contracts differ in structure?

Forward contracts are customizable private agreements traded over-the-counter with flexible terms, while futures contracts are standardized agreements traded on exchanges with fixed contract specifications.

What are the key features of forward contracts?

Forward contracts are customized agreements between two parties to buy or sell an asset at a specified future date for a price agreed upon today, featuring no standardized terms, settlement at contract maturity, and counterparty risk.

What are the major advantages of futures contracts?

Futures contracts provide price risk hedging, standardized terms for liquidity, margin trading for leverage, and transparent pricing on regulated exchanges.

How are risks managed in forward and futures contracts?

Risks in forward and futures contracts are managed through hedging strategies, margin requirements, mark-to-market settlements, and counterparty credit risk assessments to mitigate price fluctuations and default risks.

When should investors use forward contracts vs futures contracts?

Investors should use forward contracts for customized, over-the-counter hedging with flexible terms and futures contracts for standardized, exchange-traded hedging requiring liquidity and daily settlement.