Tobin's Q ratio compares a firm's market value to the replacement cost of its assets, providing insight into investment attractiveness and market efficiency. The Price-to-Book Ratio measures a company's market price relative to its book value, revealing how investors value the equity compared to its accounting value. Explore the key differences and applications of Tobin's Q and Price-to-Book Ratio to better understand corporate valuation metrics.

Main Difference

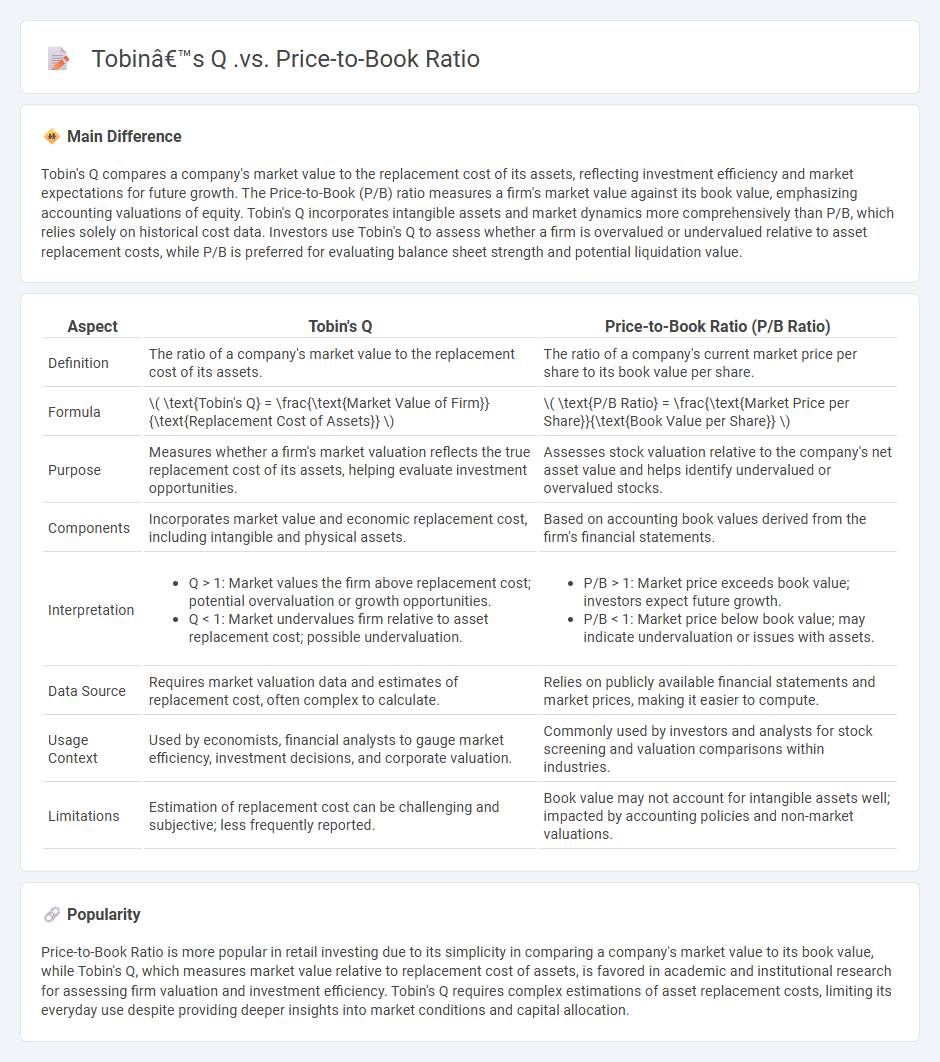

Tobin's Q compares a company's market value to the replacement cost of its assets, reflecting investment efficiency and market expectations for future growth. The Price-to-Book (P/B) ratio measures a firm's market value against its book value, emphasizing accounting valuations of equity. Tobin's Q incorporates intangible assets and market dynamics more comprehensively than P/B, which relies solely on historical cost data. Investors use Tobin's Q to assess whether a firm is overvalued or undervalued relative to asset replacement costs, while P/B is preferred for evaluating balance sheet strength and potential liquidation value.

Connection

Tobin's Q measures a company's market value relative to the replacement cost of its assets, while the Price-to-Book (P/B) ratio compares market price to book value, both reflecting market valuation against asset-based metrics. A Tobin's Q greater than one suggests market valuation exceeds asset replacement cost, often corresponding to a P/B ratio above one, indicating market prices surpass book values. Investors use these ratios to assess whether a stock is overvalued or undervalued based on asset valuation benchmarks.

Comparison Table

| Aspect | Tobin's Q | Price-to-Book Ratio (P/B Ratio) |

|---|---|---|

| Definition | The ratio of a company's market value to the replacement cost of its assets. | The ratio of a company's current market price per share to its book value per share. |

| Formula | \( \text{Tobin's Q} = \frac{\text{Market Value of Firm}}{\text{Replacement Cost of Assets}} \) | \( \text{P/B Ratio} = \frac{\text{Market Price per Share}}{\text{Book Value per Share}} \) |

| Purpose | Measures whether a firm's market valuation reflects the true replacement cost of its assets, helping evaluate investment opportunities. | Assesses stock valuation relative to the company's net asset value and helps identify undervalued or overvalued stocks. |

| Components | Incorporates market value and economic replacement cost, including intangible and physical assets. | Based on accounting book values derived from the firm's financial statements. |

| Interpretation |

|

|

| Data Source | Requires market valuation data and estimates of replacement cost, often complex to calculate. | Relies on publicly available financial statements and market prices, making it easier to compute. |

| Usage Context | Used by economists, financial analysts to gauge market efficiency, investment decisions, and corporate valuation. | Commonly used by investors and analysts for stock screening and valuation comparisons within industries. |

| Limitations | Estimation of replacement cost can be challenging and subjective; less frequently reported. | Book value may not account for intangible assets well; impacted by accounting policies and non-market valuations. |

Market Value

Market value in finance represents the current price at which an asset or company can be bought or sold in the marketplace. It reflects real-time supply and demand dynamics and is a key indicator for investors assessing stock prices, real estate, or business valuations. Market value differs from book value by accounting for external factors such as investor sentiment and market trends. It serves as a crucial metric in financial analysis, mergers and acquisitions, and portfolio management.

Book Value

Book value in finance represents the net asset value of a company, calculated as total assets minus total liabilities, reflecting the equity available to shareholders. It serves as a fundamental metric for assessing a company's intrinsic value and is often used in valuation models like the price-to-book (P/B) ratio. Investors analyze book value to identify undervalued stocks relative to their market prices. Accurate book value calculation depends on up-to-date financial statements and adherence to accounting standards such as GAAP or IFRS.

Replacement Cost

Replacement cost in finance refers to the amount needed to replace an asset at current market prices, factoring in inflation and technological advancements. It is essential for accurate insurance valuations, ensuring sufficient coverage to replace damaged or lost property. Businesses use replacement cost to assess the true value of their fixed assets for accounting and investment decisions. This metric helps avoid underestimating asset worth compared to historical cost accounting.

Balance Sheet

A balance sheet is a fundamental financial statement that provides a snapshot of a company's financial position at a specific point in time. It details assets, liabilities, and shareholders' equity, reflecting the accounting equation: Assets = Liabilities + Equity. Common asset categories include current assets such as cash, accounts receivable, and inventory, alongside long-term assets like property, plant, and equipment. Liabilities are divided into current liabilities, such as accounts payable and short-term debt, and long-term liabilities like bonds payable, providing insights into the company's financial health and stability.

Financial Ratio

Financial ratios are essential tools used in finance to evaluate a company's performance by analyzing its financial statements. Key ratios include liquidity ratios like the current ratio, profitability ratios such as return on equity (ROE), leverage ratios like debt-to-equity, and efficiency ratios including inventory turnover. These metrics help investors, creditors, and management assess operational efficiency, financial health, and risk levels. Accurate calculation and interpretation of financial ratios enable informed decision-making and strategic financial planning.

Source and External Links

Market-to-Book Value and Tobin's Q - Tobin's Q compares the total market value of the firm (equity plus debt) to the replacement value of its assets, while the Price-to-Book (market-to-book) ratio compares the market value of equity only to the book value of equity, which reflects historical costs.

Tobin's q - Tobin's Q is the ratio of the market value of the firm to the replacement cost of its tangible assets, whereas the Price-to-Book ratio is equity capitalization divided by book equity; they are related but Tobin's Q accounts for total firm value and replacement cost, not just equity and historical cost.

Tobin's q, or The Q Ratio - Tobin's Q measures how much a company is worth on the market relative to the cost of replacing its assets, providing a forward-looking valuation, while the Price-to-Book ratio contrasts market value of equity to book value, useful for assessing market pricing versus accounting value.

FAQs

What is Tobin’s Q?

Tobin's Q is the ratio of a firm's market value to the replacement cost of its assets, used to assess if a company is overvalued (Q > 1) or undervalued (Q < 1).

What is the Price-to-Book Ratio?

The Price-to-Book Ratio (P/B Ratio) measures a company's market value relative to its book value by dividing its stock price per share by its book value per share.

How is Tobin’s Q calculated?

Tobin's Q is calculated as the ratio of the market value of a firm's assets to the replacement cost of those assets.

How is the Price-to-Book Ratio calculated?

The Price-to-Book Ratio is calculated by dividing a company's market price per share by its book value per share.

What are the key differences between Tobin’s Q and Price-to-Book Ratio?

Tobin's Q measures the market value of a company's assets divided by their replacement cost, reflecting investment efficiency, while Price-to-Book Ratio compares a company's market price per share to its accounting book value per share, indicating market valuation relative to net assets.

What factors influence Tobin’s Q and Price-to-Book Ratio?

Tobin's Q is influenced by market value of a firm's assets, replacement cost of assets, investment opportunities, and macroeconomic conditions; Price-to-Book Ratio depends on net asset value, earnings growth prospects, accounting policies, and investor sentiment.

Which metric is more useful for evaluating a company’s value?

Enterprise Value (EV) is more useful for evaluating a company's value as it accounts for market capitalization, debt, and cash, providing a comprehensive measure of a company's total worth.