Basel I established the initial international banking regulations focusing on credit risk and minimum capital requirements, setting a standard risk-weighted asset framework. Basel II expanded these regulations by incorporating operational and market risks, introducing a three-pillar structure emphasizing risk assessment, supervisory review, and market discipline. Explore the detailed differences and implications to understand how these frameworks shape global banking stability.

Main Difference

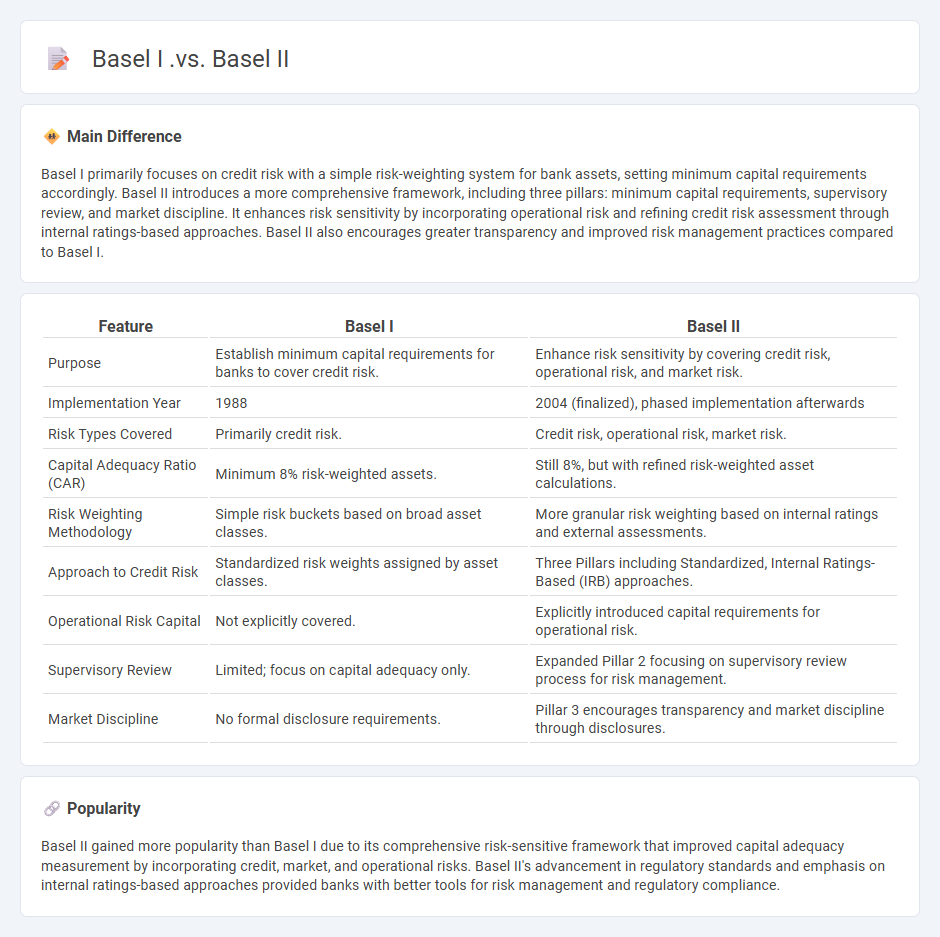

Basel I primarily focuses on credit risk with a simple risk-weighting system for bank assets, setting minimum capital requirements accordingly. Basel II introduces a more comprehensive framework, including three pillars: minimum capital requirements, supervisory review, and market discipline. It enhances risk sensitivity by incorporating operational risk and refining credit risk assessment through internal ratings-based approaches. Basel II also encourages greater transparency and improved risk management practices compared to Basel I.

Connection

Basel I established the first comprehensive framework for banking capital requirements, focusing primarily on credit risk with standardized risk weights. Basel II built on this foundation by introducing more sophisticated risk sensitivity through three pillars: minimum capital requirements, supervisory review, and market discipline. The advancements in Basel II aimed to improve the regulatory framework by incorporating operational and market risks alongside credit risk, enhancing risk management practices.

Comparison Table

| Feature | Basel I | Basel II |

|---|---|---|

| Purpose | Establish minimum capital requirements for banks to cover credit risk. | Enhance risk sensitivity by covering credit risk, operational risk, and market risk. |

| Implementation Year | 1988 | 2004 (finalized), phased implementation afterwards |

| Risk Types Covered | Primarily credit risk. | Credit risk, operational risk, market risk. |

| Capital Adequacy Ratio (CAR) | Minimum 8% risk-weighted assets. | Still 8%, but with refined risk-weighted asset calculations. |

| Risk Weighting Methodology | Simple risk buckets based on broad asset classes. | More granular risk weighting based on internal ratings and external assessments. |

| Approach to Credit Risk | Standardized risk weights assigned by asset classes. | Three Pillars including Standardized, Internal Ratings-Based (IRB) approaches. |

| Operational Risk Capital | Not explicitly covered. | Explicitly introduced capital requirements for operational risk. |

| Supervisory Review | Limited; focus on capital adequacy only. | Expanded Pillar 2 focusing on supervisory review process for risk management. |

| Market Discipline | No formal disclosure requirements. | Pillar 3 encourages transparency and market discipline through disclosures. |

Capital Adequacy Ratio

Capital Adequacy Ratio (CAR) measures a bank's available capital expressed as a percentage of its risk-weighted assets, ensuring financial stability and solvency. Regulatory bodies like the Basel Committee on Banking Supervision set minimum CAR requirements, typically 8%, to protect depositors and maintain risk management. Higher CAR indicates stronger capital buffers against potential losses, promoting trust among investors and customers. Banks with low CAR risk regulatory sanctions and reduced lending capacity, impacting overall financial health.

Risk-Weighted Assets

Risk-Weighted Assets (RWAs) quantify a bank's assets weighted by credit risk to determine capital requirements under Basel III regulations. Higher RWAs indicate greater risk exposure, influencing the minimum Tier 1 capital banks must hold to maintain solvency and absorb potential losses. Calculations incorporate credit risk, market risk, and operational risk, reflecting the diverse nature of a bank's portfolio. Regulators use RWAs to assess financial stability and enforce capital adequacy ratios, ensuring resilience in economic downturns.

Credit Risk Assessment

Credit risk assessment evaluates the probability that a borrower will default on a loan or financial obligation. It involves analyzing key financial indicators such as credit history, income stability, debt-to-income ratio, and economic conditions. Financial institutions use advanced statistical models and machine learning algorithms to predict potential losses and set appropriate interest rates. Accurate credit risk assessment supports informed lending decisions and mitigates financial losses in banking and finance sectors.

Tier 1 and Tier 2 Capital

Tier 1 Capital, also known as core capital, includes common equity, retained earnings, and non-cumulative preferred stock, serving as the primary measure of a bank's financial strength and ability to absorb losses. Tier 2 Capital comprises supplementary capital elements such as revaluation reserves, hybrid instruments, and subordinated debt, providing additional loss absorption capacity but with less permanence than Tier 1. Regulatory frameworks like Basel III require banks to maintain minimum Tier 1 and Tier 2 Capital ratios to ensure stability and reduce systemic risk within the financial system. These capital tiers play a crucial role in risk management, influencing a bank's lending capacity and overall resilience during economic downturns.

Supervisory Review Process

The Supervisory Review Process (SRP) is a critical component of banking regulation designed to ensure financial institutions maintain adequate capital levels relative to their risk profiles. Regulators use the SRP to assess risks such as credit, market, operational, and liquidity risks, requiring banks to implement robust risk management frameworks. The Basel Committee on Banking Supervision outlines the SRP within the Basel II and Basel III frameworks, emphasizing internal capital adequacy assessment processes (ICAAP). Effective supervisory review protects financial system stability by enforcing proactive capital planning and enhanced governance standards.

Source and External Links

Basel I vs. Basel II - Basel I focuses on minimum capital requirements with a simple risk-weighted asset approach, while Basel II introduces three pillars including risk management and market transparency.

Basel Accords - Basel I primarily addresses credit risk, whereas Basel II expands to include operational and market risks, enhancing risk management and capital adequacy.

Basel Accords - Basel I established basic capital requirements, while Basel II introduced a more comprehensive framework with standardized measures for various risks and enhanced transparency.

FAQs

What is Basel I?

Basel I is the first set of international banking regulations established by the Basel Committee on Banking Supervision in 1988 to set minimum capital requirements for banks, focusing on credit risk and promoting financial stability.

What is Basel II?

Basel II is an international banking regulatory framework established by the Basel Committee on Banking Supervision to enhance risk management by defining minimum capital requirements based on credit, market, and operational risks.

What are the main differences between Basel I and Basel II?

Basel I focuses on minimum capital requirements primarily based on credit risk using a standardized risk-weight approach, while Basel II introduces a three-pillar framework covering minimum capital requirements, supervisory review, and market discipline, incorporates credit, operational, and market risks, and allows advanced risk measurement approaches like Internal Ratings-Based (IRB) models.

How do Basel I and Basel II define capital requirements?

Basel I defines capital requirements by setting a minimum total capital ratio of 8% based on risk-weighted assets, focusing mainly on credit risk; Basel II refines this by introducing three pillars--minimum capital requirements (including credit, market, and operational risks), supervisory review, and market discipline--to calculate capital adequacy using more sophisticated risk assessment approaches.

What are the risks covered under Basel I and Basel II?

Basel I covers credit risk and market risk; Basel II expands coverage to credit risk, market risk, and operational risk.

How did Basel II improve upon Basel I?

Basel II improved upon Basel I by introducing a three-pillar framework emphasizing risk-sensitive capital requirements, supervisory review, and market discipline. It enhanced credit risk measurement through internal ratings-based approaches, incorporated operational risk capital charges, and improved risk management by requiring greater transparency and disclosure.

Why were changes from Basel I to Basel II necessary?

Changes from Basel I to Basel II were necessary to address the limitations of Basel I by introducing more risk-sensitive capital requirements, incorporating credit, operational, and market risk assessments, and improving the regulatory framework's ability to capture the complexity of modern banking activities.