PIK (Payment-in-Kind) bonds allow issuers to pay interest in additional securities rather than cash, benefiting companies with cash flow constraints. Zero-coupon bonds, meanwhile, are issued at a discount and provide no periodic interest, paying the full face value at maturity. Explore detailed comparisons to understand their unique structures and investment implications.

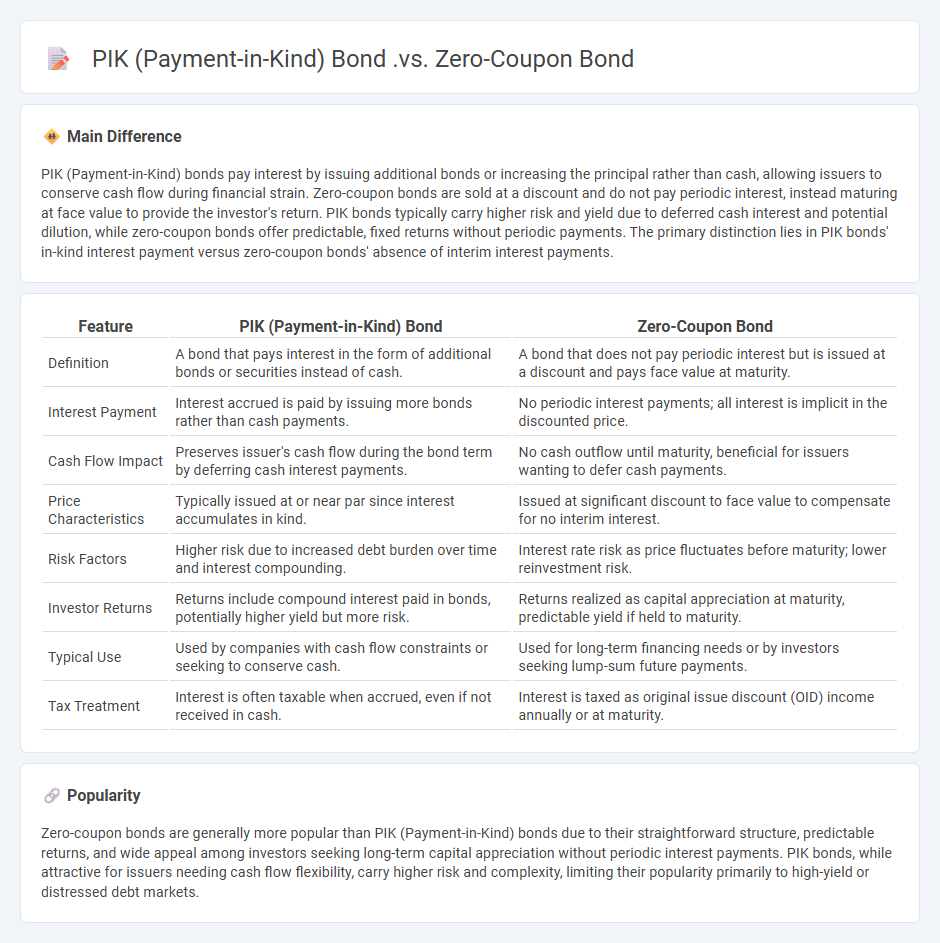

Main Difference

PIK (Payment-in-Kind) bonds pay interest by issuing additional bonds or increasing the principal rather than cash, allowing issuers to conserve cash flow during financial strain. Zero-coupon bonds are sold at a discount and do not pay periodic interest, instead maturing at face value to provide the investor's return. PIK bonds typically carry higher risk and yield due to deferred cash interest and potential dilution, while zero-coupon bonds offer predictable, fixed returns without periodic payments. The primary distinction lies in PIK bonds' in-kind interest payment versus zero-coupon bonds' absence of interim interest payments.

Connection

PIK bonds and zero-coupon bonds share the characteristic of deferring cash interest payments, with PIK bonds paying interest through additional bonds or equity instead of cash, and zero-coupon bonds accruing interest until maturity without periodic payments. Both instruments allow issuers to conserve cash flow during the initial period, making them attractive for companies needing liquidity flexibility. Investors in both bonds rely on the accrued value, realized either at maturity or through conversion, reflecting an embedded interest component despite the absence of regular cash coupons.

Comparison Table

| Feature | PIK (Payment-in-Kind) Bond | Zero-Coupon Bond |

|---|---|---|

| Definition | A bond that pays interest in the form of additional bonds or securities instead of cash. | A bond that does not pay periodic interest but is issued at a discount and pays face value at maturity. |

| Interest Payment | Interest accrued is paid by issuing more bonds rather than cash payments. | No periodic interest payments; all interest is implicit in the discounted price. |

| Cash Flow Impact | Preserves issuer's cash flow during the bond term by deferring cash interest payments. | No cash outflow until maturity, beneficial for issuers wanting to defer cash payments. |

| Price Characteristics | Typically issued at or near par since interest accumulates in kind. | Issued at significant discount to face value to compensate for no interim interest. |

| Risk Factors | Higher risk due to increased debt burden over time and interest compounding. | Interest rate risk as price fluctuates before maturity; lower reinvestment risk. |

| Investor Returns | Returns include compound interest paid in bonds, potentially higher yield but more risk. | Returns realized as capital appreciation at maturity, predictable yield if held to maturity. |

| Typical Use | Used by companies with cash flow constraints or seeking to conserve cash. | Used for long-term financing needs or by investors seeking lump-sum future payments. |

| Tax Treatment | Interest is often taxable when accrued, even if not received in cash. | Interest is taxed as original issue discount (OID) income annually or at maturity. |

Interest Payment Structure

Interest payment structure defines how interest on debt instruments is calculated and disbursed, impacting both borrowers and lenders. Common structures include fixed-rate, where interest remains constant throughout the loan term, and variable-rate, which fluctuates based on benchmark indices such as LIBOR or SOFR. Amortizing loans require periodic payments covering both interest and principal, while bullet loans involve interest payments during the term and a lump-sum principal repayment at maturity. Understanding these structures is crucial for accurate financial modeling, risk assessment, and optimizing debt management strategies.

Coupon Frequency

Coupon frequency refers to the number of interest payments a bondholder receives per year, commonly ranging from annual, semi-annual, to quarterly intervals. Most U.S. Treasury bonds pay coupons semi-annually, meaning investors receive two payments each year. The coupon frequency influences the bond's cash flow schedule and affects its duration and yield calculations. Understanding coupon frequency is essential for accurately assessing the bond's income stream and reinvestment risk.

Maturity Value

Maturity value in finance refers to the total amount payable to an investor at the end of a financial instrument's term, including the principal and accrued interest or returns. It is commonly associated with fixed-income securities such as bonds, treasury bills, and certificates of deposit. Calculating maturity value involves factoring in the face value of the investment and the interest rate applied over the holding period. This metric is essential for investors to assess the profitability and expected returns of their investments at maturity.

Tax Treatment

Tax treatment in finance refers to the way various financial transactions, investments, and income streams are assessed for taxation purposes by authorities such as the IRS. Understanding how capital gains, dividends, interest income, and corporate earnings are taxed helps investors and businesses optimize their tax liabilities. Specific tax codes, like the Internal Revenue Code in the United States, detail rates, deductions, and exemptions applicable to different financial instruments. Proper tax planning can maximize after-tax returns and ensure compliance with relevant regulations.

Investor Risk

Investor risk refers to the potential financial loss an investor faces due to market volatility, economic downturns, or company-specific issues. Common types of investor risk include market risk, credit risk, liquidity risk, and interest rate risk, each affecting portfolio performance differently. Quantitative measures like beta, standard deviation, and Value at Risk (VaR) help assess the level of risk associated with an investment. Effective risk management strategies, such as diversification and asset allocation, aim to minimize exposure and protect capital in volatile financial markets.

Source and External Links

Payment-In-Kind Bonds Explained - PIK bonds pay interest in additional bonds instead of cash during the term, deferring cash payments until maturity, often carry higher risk and yields, and act as mezzanine debt relieving issuers from immediate cash interest obligations.

Types of Bonds Explained | CFA Level 1 - AnalystPrep - Zero-coupon bonds defer all interest payments until maturity by being issued at a deep discount, representing an extreme form of deferred coupon bond compared to PIK bonds which pay interest in kind but accrue it differently.

Giddy: What are Pay in Kind Securities? - NYU Stern - Both PIK and zero-coupon bonds offer issuers cash flow relief by deferring cash interest payments, but PIK bonds pay interest with additional securities while zero-coupon bonds make no interim interest payments and accrue value until maturity.

FAQs

What is a PIK bond?

A PIK bond is a type of debt instrument where interest payments are made in the form of additional bonds or increasing the principal rather than cash, commonly used in high-yield or leveraged financing.

What is a zero-coupon bond?

A zero-coupon bond is a debt security that does not pay periodic interest and is issued at a discount to its face value, maturing at par value to provide returns.

How do PIK bonds pay interest?

PIK bonds pay interest by issuing additional bonds or increasing the principal amount instead of making cash interest payments.

How do zero-coupon bonds generate returns?

Zero-coupon bonds generate returns by being issued at a discount to their face value and paying the full face value at maturity, with the difference representing the bondholder's earnings.

What are the risks of PIK bonds?

PIK bonds carry risks including higher default probability due to deferred interest payments, increased debt burden from compounding interest, lower liquidity in secondary markets, and potential dilution of equity if converted.

What are the risks of zero-coupon bonds?

Zero-coupon bonds carry risks including interest rate risk, inflation risk, credit/default risk, and liquidity risk.

When should investors consider PIK or zero-coupon bonds?

Investors should consider PIK or zero-coupon bonds when seeking deferred interest payments, aiming for capital appreciation, or during periods of cash flow constraints and low current income needs.