Basel II and Basel III are international regulatory frameworks developed by the Basel Committee on Banking Supervision to enhance bank capital adequacy and risk management. Basel II introduced a three-pillar approach focusing on minimum capital requirements, supervisory review, and market discipline, while Basel III builds on this by implementing stricter capital ratios, leverage limits, and liquidity standards to address weaknesses revealed during the 2008 financial crisis. Explore the key distinctions and impacts of Basel II versus Basel III to understand their roles in shaping global banking stability.

Main Difference

Basel II primarily focuses on enhancing risk sensitivity by introducing three pillars: minimum capital requirements, supervisory review, and market discipline, while Basel III significantly strengthens capital adequacy by increasing minimum capital ratios and introducing a leverage ratio and liquidity requirements like the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR). Basel III addresses shortcomings revealed during the 2008 financial crisis by emphasizing higher quality capital, particularly common equity tier 1 (CET1), and requiring banks to hold capital buffers to absorb potential losses. Basel II's risk-weighted asset framework is improved in Basel III through more stringent risk coverage and constraints on excessive leverage to improve bank resilience. Basel III also incorporates macroprudential tools, such as countercyclical capital buffers, to mitigate systemic risks absent in Basel II.

Connection

Basel II and Basel III are connected through their shared goal of strengthening bank capital requirements and risk management to enhance financial system stability. Basel III builds upon Basel II's framework by introducing higher capital thresholds, improved risk coverage, and new liquidity standards such as the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR). Together, these accords form a progressive regulatory approach to mitigate systemic risks and promote resilience within international banking sectors.

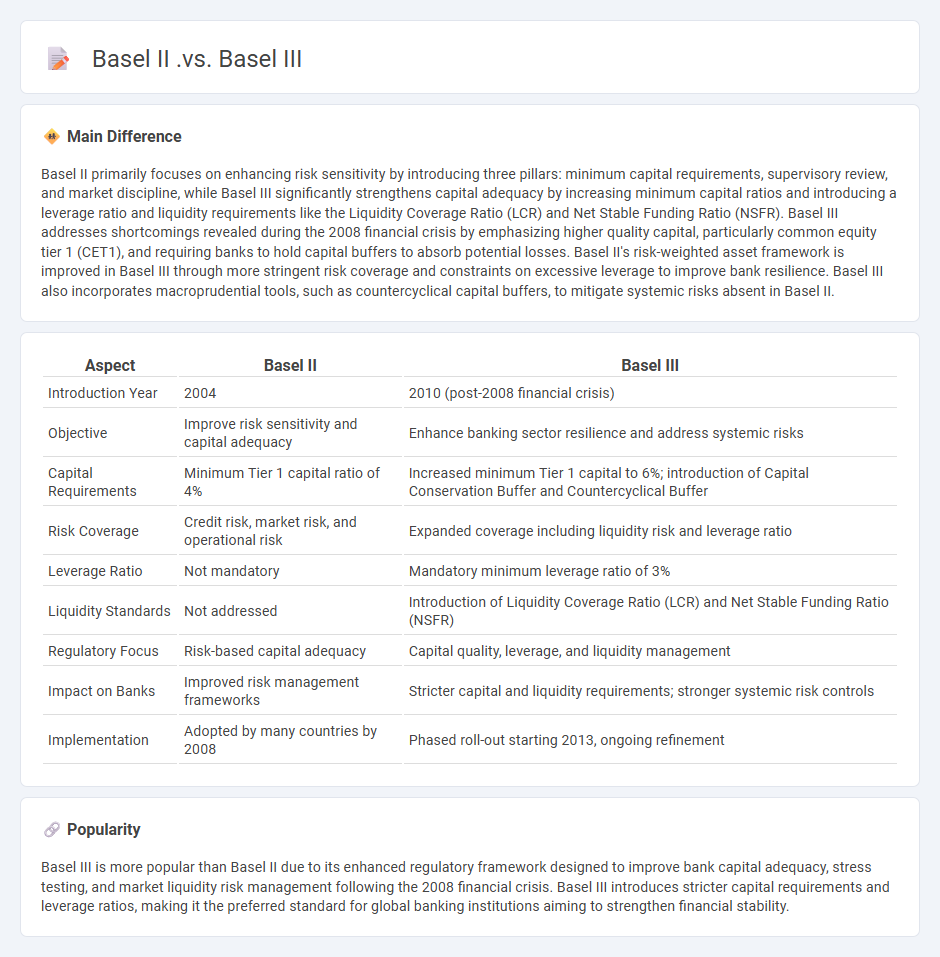

Comparison Table

| Aspect | Basel II | Basel III |

|---|---|---|

| Introduction Year | 2004 | 2010 (post-2008 financial crisis) |

| Objective | Improve risk sensitivity and capital adequacy | Enhance banking sector resilience and address systemic risks |

| Capital Requirements | Minimum Tier 1 capital ratio of 4% | Increased minimum Tier 1 capital to 6%; introduction of Capital Conservation Buffer and Countercyclical Buffer |

| Risk Coverage | Credit risk, market risk, and operational risk | Expanded coverage including liquidity risk and leverage ratio |

| Leverage Ratio | Not mandatory | Mandatory minimum leverage ratio of 3% |

| Liquidity Standards | Not addressed | Introduction of Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) |

| Regulatory Focus | Risk-based capital adequacy | Capital quality, leverage, and liquidity management |

| Impact on Banks | Improved risk management frameworks | Stricter capital and liquidity requirements; stronger systemic risk controls |

| Implementation | Adopted by many countries by 2008 | Phased roll-out starting 2013, ongoing refinement |

Capital Adequacy

Capital adequacy measures a financial institution's ability to absorb losses and sustain operations, ensuring stability and protecting depositors. Regulatory frameworks such as Basel III require banks to maintain minimum capital ratios, including the Common Equity Tier 1 (CET1) ratio above 4.5%. This metric evaluates equity capital relative to risk-weighted assets, promoting risk management and reducing insolvency risk. Maintaining robust capital adequacy is critical for compliance with international banking standards and financial resilience.

Risk Coverage

Risk coverage in finance refers to the strategies and mechanisms used to protect against potential financial losses from uncertain events. Common methods include insurance policies, hedging strategies using derivatives like options and futures, and diversification of investment portfolios. Effective risk coverage mitigates exposure to market volatility, credit defaults, interest rate fluctuations, and operational risks. Financial institutions often employ risk assessment models such as Value at Risk (VaR) to quantify potential losses and determine adequate risk coverage levels.

Leverage Ratio

The leverage ratio measures a company's financial leverage by comparing its total debt to its equity or assets, indicating the proportion of borrowed funds used to finance assets. Regulatory standards, such as Basel III, require banks to maintain a minimum leverage ratio of 3% to ensure financial stability and reduce systemic risk. High leverage ratios often signal increased risk of insolvency during economic downturns, while lower ratios suggest more conservative financing strategies. Investors and analysts use the leverage ratio to assess credit risk, capital structure, and the potential impact of debt on return on equity (ROE).

Liquidity Standards

Liquidity standards in finance are regulatory requirements designed to ensure financial institutions maintain sufficient liquid assets to meet short-term obligations. These standards, such as the Liquidity Coverage Ratio (LCR) established by Basel III, mandate banks to hold a buffer of high-quality liquid assets covering net cash outflows over a 30-day stress period. Maintaining adequate liquidity reduces the risk of insolvency during market disruptions, preserving financial stability. Central banks and regulatory bodies worldwide enforce these standards to prevent systemic crises and protect depositors.

Regulatory Framework

The regulatory framework in finance comprises laws, guidelines, and standards set by authorities such as the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA) to ensure market integrity and protect investors. Key regulations include the Dodd-Frank Act, Sarbanes-Oxley Act, and Basel III, which address risk management, corporate governance, and capital requirements. Compliance with these regulations helps prevent fraud, promotes transparency, and stabilizes financial institutions. Regulatory bodies continuously update policies to adapt to evolving market dynamics and technological advancements like fintech and digital currencies.

Source and External Links

Basel II - Basel II is a framework for international banking standards that aimed to improve the minimum capital requirements for banks, superseding Basel I and addressing various risks but was criticized for its weaknesses during the 2008 financial crisis

Basel III - Basel III is a set of financial reforms developed to strengthen regulation, supervision, and risk management within the banking sector, enhancing capital requirements and liquidity standards in response to the 2008 financial crisis

Basel III vs Basel II Output Floor - Basel III reforms replaced the Basel II output floor with a more robust risk-sensitive floor based on revised standardized approaches to ensure comparability and credibility in risk-weighted calculations among banks

FAQs

What are Basel II and Basel III?

Basel II and Basel III are international regulatory frameworks developed by the Basel Committee on Banking Supervision to strengthen bank capital requirements, risk management, and financial stability. Basel II focuses on minimum capital requirements, supervisory review, and market discipline, while Basel III introduces higher capital standards, leverage ratios, and liquidity requirements to address vulnerabilities exposed by the 2008 financial crisis.

What are the key differences between Basel II and Basel III?

Basel II focuses on minimum capital requirements with three pillars: minimum capital, supervisory review, and market discipline, while Basel III enhances these by increasing capital quality and quantity, introducing leverage ratio, liquidity standards like LCR and NSFR, and stricter risk coverage.

How does Basel III improve upon Basel II?

Basel III improves upon Basel II by increasing minimum capital requirements, introducing leverage and liquidity ratios, enhancing risk coverage for derivatives and off-balance-sheet exposures, and implementing stricter supervisory review and market discipline standards.

What are the main requirements of Basel II?

Basel II requires banks to maintain adequate capital based on risk exposure, implement effective risk management practices, conduct regular internal and external audits, and enhance transparency through detailed disclosures of risk and capital adequacy.

What are the new capital requirements introduced by Basel III?

Basel III introduced a minimum Common Equity Tier 1 (CET1) capital ratio of 4.5%, a Tier 1 capital ratio of 6%, a total capital ratio of 8%, a Capital Conservation Buffer of 2.5%, and a Countercyclical Capital Buffer ranging from 0% to 2.5% of risk-weighted assets.

How do Basel III regulations affect banks compared to Basel II?

Basel III regulations increase bank capital requirements by raising minimum common equity Tier 1 ratios to 4.5% from 2%, introduce a 2.5% capital conservation buffer, implement a leverage ratio minimum of 3%, and enforce stricter liquidity standards like the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR), resulting in enhanced bank resilience compared to Basel II.

Why was Basel III introduced after Basel II?

Basel III was introduced after Basel II to address the weaknesses in risk management revealed during the 2008 financial crisis by enhancing bank capital requirements, improving liquidity standards, and strengthening overall financial system resilience.