Accrual bonds accumulate interest periodically but do not pay it out until maturity, offering investors compounding returns over time. Zero coupon bonds are issued at a discount and provide a lump-sum payment at maturity without periodic interest payments, making them ideal for long-term investment strategies. Explore the detailed differences to optimize your bond investment portfolio.

Main Difference

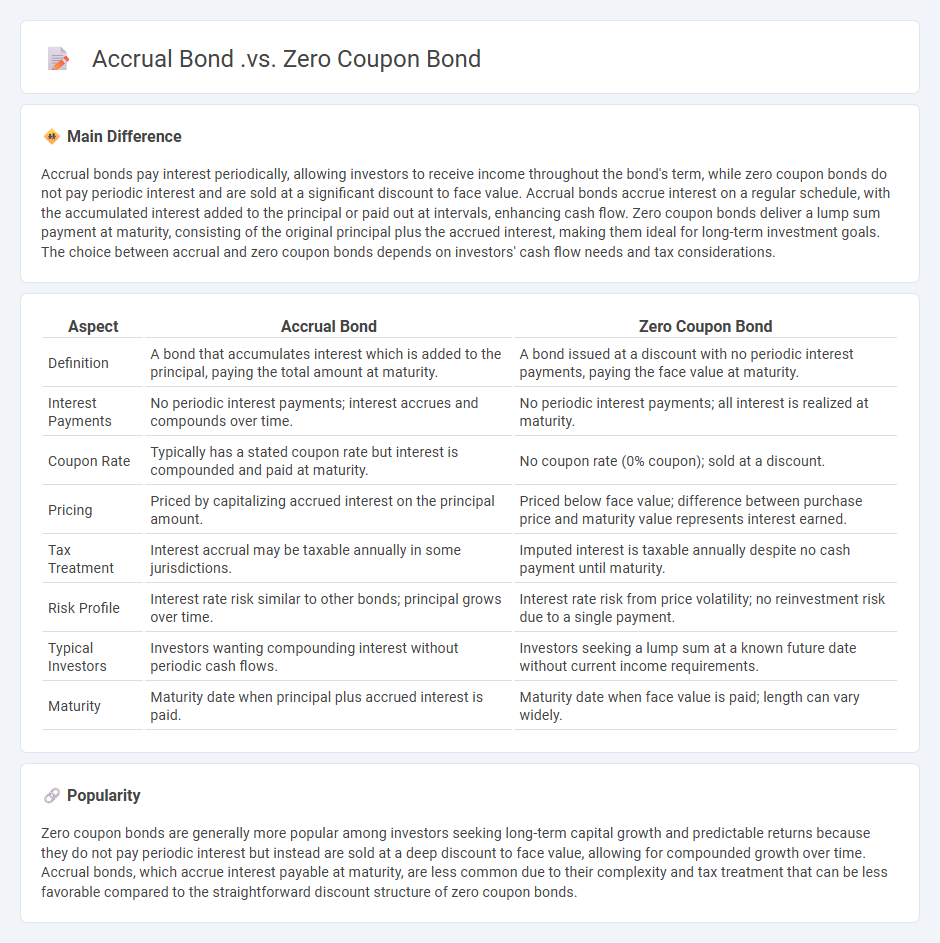

Accrual bonds pay interest periodically, allowing investors to receive income throughout the bond's term, while zero coupon bonds do not pay periodic interest and are sold at a significant discount to face value. Accrual bonds accrue interest on a regular schedule, with the accumulated interest added to the principal or paid out at intervals, enhancing cash flow. Zero coupon bonds deliver a lump sum payment at maturity, consisting of the original principal plus the accrued interest, making them ideal for long-term investment goals. The choice between accrual and zero coupon bonds depends on investors' cash flow needs and tax considerations.

Connection

Accrual bonds and zero coupon bonds are connected through their treatment of interest payments, as both do not pay periodic interest but rather accrue it over time and pay a lump sum at maturity. Accrual bonds accumulate the interest and add it to the principal value, increasing the bond's value until maturity, similar to zero coupon bonds that are issued at a discount and redeemed at face value. This connection highlights their shared characteristic of generating returns primarily through capital appreciation instead of periodic coupon payments.

Comparison Table

| Aspect | Accrual Bond | Zero Coupon Bond |

|---|---|---|

| Definition | A bond that accumulates interest which is added to the principal, paying the total amount at maturity. | A bond issued at a discount with no periodic interest payments, paying the face value at maturity. |

| Interest Payments | No periodic interest payments; interest accrues and compounds over time. | No periodic interest payments; all interest is realized at maturity. |

| Coupon Rate | Typically has a stated coupon rate but interest is compounded and paid at maturity. | No coupon rate (0% coupon); sold at a discount. |

| Pricing | Priced by capitalizing accrued interest on the principal amount. | Priced below face value; difference between purchase price and maturity value represents interest earned. |

| Tax Treatment | Interest accrual may be taxable annually in some jurisdictions. | Imputed interest is taxable annually despite no cash payment until maturity. |

| Risk Profile | Interest rate risk similar to other bonds; principal grows over time. | Interest rate risk from price volatility; no reinvestment risk due to a single payment. |

| Typical Investors | Investors wanting compounding interest without periodic cash flows. | Investors seeking a lump sum at a known future date without current income requirements. |

| Maturity | Maturity date when principal plus accrued interest is paid. | Maturity date when face value is paid; length can vary widely. |

Interest Accrual

Interest accrual in finance refers to the process of accumulating interest on a principal amount over time, even if the interest has not yet been paid out. This concept is essential for calculating earned interest on loans, savings, and bonds based on the agreed interest rate and compounding frequency. Accurate interest accrual ensures that financial statements reflect the true cost or income associated with interest-bearing assets or liabilities as of a specific date. The accrual method adheres to the matching principle in accounting, recognizing interest expenses or revenues in the period they are incurred.

Maturity Payment

Maturity payment refers to the final amount paid to the holder of a financial instrument, such as a bond or fixed deposit, when it reaches its maturity date. This payment includes the principal amount invested plus any accrued interest or returns specified in the contract. In bond markets, maturity payments are critical for investors to recover their initial capital along with agreed-upon yield. The structure and timing of maturity payments are governed by the terms outlined during the instrument's issuance.

Coupon Payments

Coupon payments represent the periodic interest payments made to bondholders during the life of a bond, typically expressed as a fixed percentage of the bond's face value. These payments are usually made semiannually, although frequency can vary depending on the bond's terms. The coupon rate, which determines the payment amount, is a critical factor in bond valuation and investor yield calculations. Understanding coupon payments helps investors assess income streams and compare fixed-income securities effectively.

Yield to Maturity (YTM)

Yield to Maturity (YTM) represents the total return an investor can expect to earn if a bond is held until it matures. It incorporates the bond's current market price, coupon interest payments, face value, and time remaining until maturity to yield an annualized rate of return. YTM assumes all coupon payments are reinvested at the same rate and is expressed as an annual percentage. Investors use YTM to compare the attractiveness of different fixed-income securities with varying maturities and coupon rates.

Principal Reinvestment

Principal reinvestment is a critical strategy in finance where the principal amount from matured investments, such as bonds or certificates of deposit (CDs), is reinvested into new securities to maintain or grow the capital base. This approach maximizes compound growth potential by continuously deploying capital rather than withdrawing funds, enhancing overall portfolio returns. According to data from the Investment Company Institute, reinvested dividends and principal repayments contribute significantly to the total return of fixed-income investments, especially over long-term horizons. Tax-deferred accounts like IRAs and 401(k)s often amplify the benefits of principal reinvestment by allowing earnings to compound without immediate tax liabilities.

Source and External Links

Zero Coupon Bonds: A Look at the Accrual Bond Alternative - Accrual bonds, also known as zero-coupon bonds, are fixed-income securities issued at a discount that do not pay periodic interest but instead accrue interest over time and pay the full amount at maturity, offering a stable investment especially in volatile interest rate environments.

Zero Coupon Bond: Definition, Features & Formula - FreshBooks - Zero coupon bonds or accrual bonds are bought at a significant discount and pay no periodic interest, with their return being the difference between purchase price and the face value at maturity, contrasting with traditional coupon bonds that pay regular interest.

Zero Coupon Bonds - Financial Edge Training - Zero coupon bonds differ from traditional bonds by paying no interim interest but instead provide profit at maturity by being sold below their redemption value; they are also known as zero bonds, zeroes, or accrual bonds.

FAQs

What is an accrual bond?

An accrual bond is a type of bond that does not pay periodic interest but instead accumulates interest which is paid at maturity along with the principal.

What is a zero coupon bond?

A zero coupon bond is a debt security that is sold at a deep discount and pays no periodic interest, redeeming its face value at maturity.

How do accrual bonds generate interest?

Accrual bonds generate interest by accumulating unpaid interest over time, which is added to the bond's principal value and paid to investors at maturity.

How do zero coupon bonds generate returns?

Zero coupon bonds generate returns by being sold at a deep discount to their face value and paying no periodic interest, so investors gain profit when the bond matures at full par value.

What are the main differences between accrual bonds and zero coupon bonds?

Accrual bonds pay periodic interest that accrues and is compounded but not distributed until maturity, while zero coupon bonds do not pay periodic interest and are issued at a deep discount, repaid at face value at maturity.

Who should invest in accrual bonds vs zero coupon bonds?

Investors seeking regular income should invest in accrual bonds for periodic interest payments, while those aiming for capital appreciation and tax-deferral benefits should choose zero coupon bonds, which pay no interim interest but mature at face value.

What are the risks in investing in accrual bonds compared to zero coupon bonds?

Accrual bonds carry higher reinvestment risk due to periodic interest accruals, increased interest rate sensitivity causing greater price volatility, and potential credit risk from issuer default, whereas zero coupon bonds have no reinvestment risk but higher duration risk since all interest is realized at maturity.