Variance swaps and volatility swaps are derivative contracts used to hedge or speculate on future market fluctuations, with variance swaps based on the squared returns and volatility swaps on the standard deviation of returns. Variance swaps offer exposure to the variability of asset prices by directly trading variance, while volatility swaps provide a more intuitive exposure by trading the volatility level itself. Explore the distinct mechanics and applications of each to enhance your risk management strategy.

Main Difference

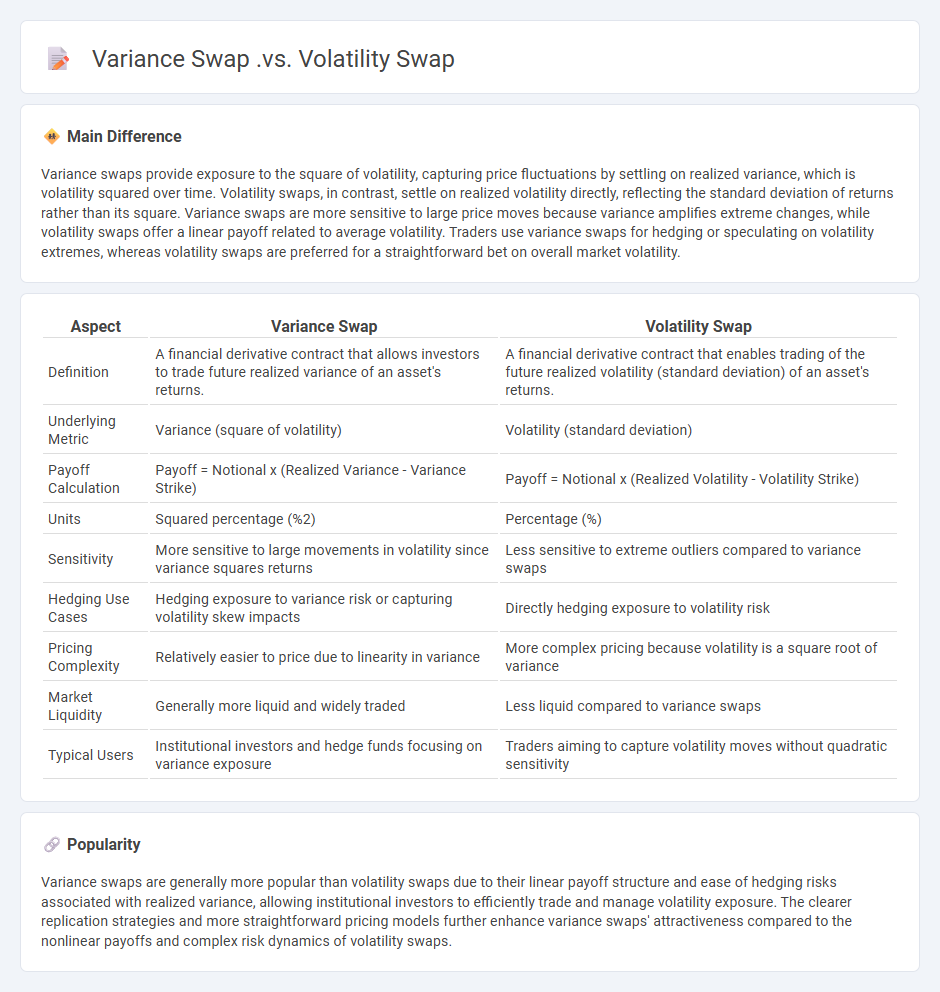

Variance swaps provide exposure to the square of volatility, capturing price fluctuations by settling on realized variance, which is volatility squared over time. Volatility swaps, in contrast, settle on realized volatility directly, reflecting the standard deviation of returns rather than its square. Variance swaps are more sensitive to large price moves because variance amplifies extreme changes, while volatility swaps offer a linear payoff related to average volatility. Traders use variance swaps for hedging or speculating on volatility extremes, whereas volatility swaps are preferred for a straightforward bet on overall market volatility.

Connection

Variance swaps and volatility swaps are both derivative contracts that allow investors to trade future realized volatility of an underlying asset, but they differ in payoff structure. A variance swap's payoff is based on the squared volatility (variance), making it sensitive to large movements, while a volatility swap's payoff depends directly on the realized volatility, which is the square root of variance. Traders often use variance swaps to hedge or speculate on volatility variance, while volatility swaps provide a more intuitive exposure to actual volatility levels.

Comparison Table

| Aspect | Variance Swap | Volatility Swap |

|---|---|---|

| Definition | A financial derivative contract that allows investors to trade future realized variance of an asset's returns. | A financial derivative contract that enables trading of the future realized volatility (standard deviation) of an asset's returns. |

| Underlying Metric | Variance (square of volatility) | Volatility (standard deviation) |

| Payoff Calculation | Payoff = Notional x (Realized Variance - Variance Strike) | Payoff = Notional x (Realized Volatility - Volatility Strike) |

| Units | Squared percentage (%2) | Percentage (%) |

| Sensitivity | More sensitive to large movements in volatility since variance squares returns | Less sensitive to extreme outliers compared to variance swaps |

| Hedging Use Cases | Hedging exposure to variance risk or capturing volatility skew impacts | Directly hedging exposure to volatility risk |

| Pricing Complexity | Relatively easier to price due to linearity in variance | More complex pricing because volatility is a square root of variance |

| Market Liquidity | Generally more liquid and widely traded | Less liquid compared to variance swaps |

| Typical Users | Institutional investors and hedge funds focusing on variance exposure | Traders aiming to capture volatility moves without quadratic sensitivity |

Payoff Structure

Payoff structure in finance defines the relationship between an investment's outcomes and its corresponding financial returns under various market conditions. It quantifies potential profits or losses from assets like options, futures, and derivatives by mapping payoffs across different price levels at maturity. Analyzing payoff structures helps investors gauge risk exposure and design strategies such as hedging or speculation to optimize portfolio performance. Common payoff profiles include linear (stocks), asymmetric (options), and capped (bonds with callable features), each influencing risk-reward dynamics distinctly.

Exposure Type

Exposure type in finance refers to the categorization of potential risks that investors or institutions face due to market, credit, operational, or liquidity factors. Common exposure types include market exposure, which involves fluctuations in asset prices; credit exposure, reflecting the risk of counterparty default; operational exposure related to internal process failures; and liquidity exposure, concerning the ability to meet short-term obligations. Financial institutions quantify these exposures to manage risk through diversification, hedging strategies, and regulatory capital requirements. Accurate measurement of exposure types supports robust risk management and compliance with frameworks such as Basel III.

Hedging Strategies

Hedging strategies in finance involve using financial instruments or market positions to reduce the risk of adverse price movements in assets. Common tools include derivatives like options, futures, and swaps, which help investors and companies protect against fluctuations in interest rates, currency exchange rates, and commodity prices. Effective hedging enhances portfolio stability and can improve risk-adjusted returns by mitigating potential losses in volatile markets. Firms in industries such as agriculture, energy, and finance frequently employ these strategies for risk management and financial planning.

Settlement Calculation

Settlement calculation in finance involves determining the final amount payable or receivable in a securities transaction, factoring in trade price, quantity, and applicable fees or taxes. The process ensures accurate transfer of ownership and funds between buyer and seller on the settlement date, commonly two business days after the trade date (T+2) for equities. Precise settlement calculations mitigate counterparty risk and support regulatory compliance in markets worldwide. Efficient settlement systems leverage automation and real-time data to enhance accuracy and reduce processing time.

Application Scenarios

Finance leverages artificial intelligence to enhance risk assessment by analyzing vast datasets for credit scoring and fraud detection, improving accuracy and reducing defaults. Algorithmic trading systems use real-time market data and predictive models to execute high-frequency trades, optimizing portfolio performance. Automated customer service platforms employ natural language processing to handle inquiries and streamline financial transactions efficiently. Regulatory compliance is supported by AI tools that monitor transactions for suspicious activities and ensure adherence to evolving financial regulations.

Source and External Links

Variance Swap - What Is It, Replication, Example, vs Volatility Swap - This article provides an overview of variance swaps, including how they differ from volatility swaps, with variance swaps being more commonly used for hedging in equity markets.

Volatility Swap - Overview, Definition of Swap, Payoff, and Example - This resource explains volatility swaps, highlighting their resemblance to variance swaps but with a focus on absolute volatility rather than variance.

Volatility and Variance Swaps - This thesis discusses the complexities of pricing volatility and variance swaps, including the challenges of estimating future volatility and variance for these derivatives.

FAQs

What is a variance swap?

A variance swap is a financial derivative contract that allows investors to trade future realized variance of an asset's returns against current implied variance, enabling direct exposure to volatility without exposure to the asset price itself.

What is a volatility swap?

A volatility swap is a financial derivative contract allowing investors to trade future realized volatility of an asset, providing pure exposure to volatility risk without price direction bias.

How does a variance swap differ from a volatility swap?

A variance swap pays the difference between realized variance and the variance strike, measuring squared volatility, while a volatility swap pays the difference between realized volatility (the square root of variance) and the volatility strike, reflecting actual volatility levels.

What are the payoffs in a variance swap?

The payoff of a variance swap is the difference between the realized variance of the underlying asset over the swap period and the variance strike, multiplied by the notional amount of the variance swap.

What are the payoffs in a volatility swap?

The payoff of a volatility swap is the difference between the realized volatility of the underlying asset over the swap period and the predetermined strike volatility, multiplied by the notional amount.

Why do traders use variance swaps?

Traders use variance swaps to hedge or speculate on the future volatility of an asset without exposure to its price direction.

Why do traders use volatility swaps?

Traders use volatility swaps to hedge against or speculate on future volatility without exposure to the direction of the underlying asset's price.