Zero-coupon bonds are debt securities that do not pay periodic interest but are issued at a deep discount to their face value, maturing at par. Coupon bonds provide regular interest payments, known as coupons, throughout the life of the bond, offering steady income to investors. Explore the key differences between zero-coupon bonds and coupon bonds to understand which investment aligns with your financial goals.

Main Difference

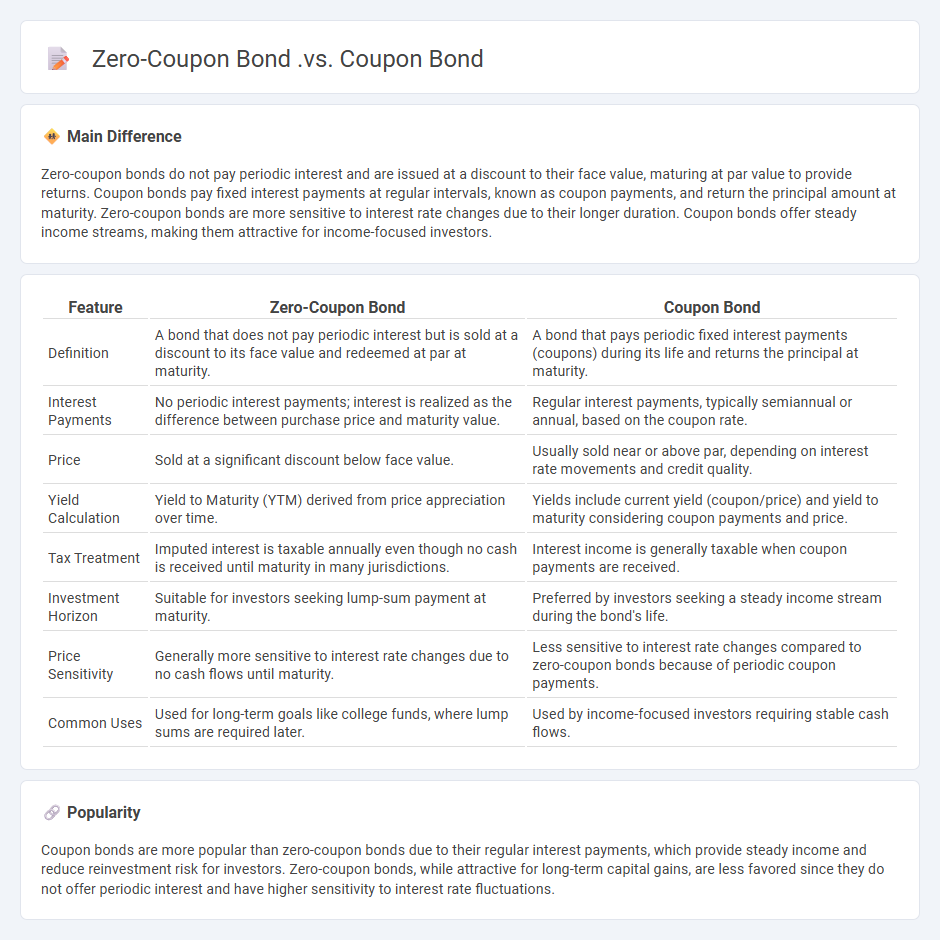

Zero-coupon bonds do not pay periodic interest and are issued at a discount to their face value, maturing at par value to provide returns. Coupon bonds pay fixed interest payments at regular intervals, known as coupon payments, and return the principal amount at maturity. Zero-coupon bonds are more sensitive to interest rate changes due to their longer duration. Coupon bonds offer steady income streams, making them attractive for income-focused investors.

Connection

Zero-coupon bonds and coupon bonds are both fixed-income securities that represent loans made by investors to issuers, typically corporations or governments. Zero-coupon bonds are sold at a discount to their face value and do not pay periodic interest, while coupon bonds provide regular interest payments throughout the life of the bond. Both bond types are linked by their fundamental function of debt financing and the eventual repayment of principal at maturity.

Comparison Table

| Feature | Zero-Coupon Bond | Coupon Bond |

|---|---|---|

| Definition | A bond that does not pay periodic interest but is sold at a discount to its face value and redeemed at par at maturity. | A bond that pays periodic fixed interest payments (coupons) during its life and returns the principal at maturity. |

| Interest Payments | No periodic interest payments; interest is realized as the difference between purchase price and maturity value. | Regular interest payments, typically semiannual or annual, based on the coupon rate. |

| Price | Sold at a significant discount below face value. | Usually sold near or above par, depending on interest rate movements and credit quality. |

| Yield Calculation | Yield to Maturity (YTM) derived from price appreciation over time. | Yields include current yield (coupon/price) and yield to maturity considering coupon payments and price. |

| Tax Treatment | Imputed interest is taxable annually even though no cash is received until maturity in many jurisdictions. | Interest income is generally taxable when coupon payments are received. |

| Investment Horizon | Suitable for investors seeking lump-sum payment at maturity. | Preferred by investors seeking a steady income stream during the bond's life. |

| Price Sensitivity | Generally more sensitive to interest rate changes due to no cash flows until maturity. | Less sensitive to interest rate changes compared to zero-coupon bonds because of periodic coupon payments. |

| Common Uses | Used for long-term goals like college funds, where lump sums are required later. | Used by income-focused investors requiring stable cash flows. |

Interest Payments

Interest payments represent the cost borrowers incur for using borrowed capital, calculated as a percentage of the principal amount. In 2023, global interest payments on corporate debt reached approximately $3.8 trillion, reflecting rising interest rates and increased borrowing. Central banks' monetary policies directly influence interest rates, shaping loan affordability and investment decisions. Effective management of interest payments is crucial for maintaining corporate liquidity and creditworthiness.

Maturity Value

Maturity value in finance refers to the amount payable to the holder of a financial instrument at the end of its term or maturity date. It typically includes the principal investment plus any accrued interest or earnings over the period. For example, the maturity value of a fixed deposit or a bond is the sum of the initial principal and the interest earned at the agreed rate. Understanding the maturity value is crucial for investors to evaluate the returns on time-bound financial assets.

Yield to Maturity (YTM)

Yield to Maturity (YTM) is the total return anticipated on a bond if held until it matures, expressed as an annual rate. It incorporates all future coupon payments, the difference between the bond's current price and its face value at maturity, and assumes reinvestment of coupons at the same yield. YTM is a critical metric for investors assessing the profitability of fixed-income securities and comparing bonds with different prices, coupons, and maturities. Calculating YTM involves solving for the discount rate that equates the present value of all future cash flows to the bond's current market price.

Discount vs Par Issuance

Issuing bonds at a discount occurs when the bond's coupon rate is lower than prevailing market interest rates, causing its price to fall below its face value. Par issuance refers to bonds sold at exactly their face value, typically because the coupon rate aligns with current market rates. Discount bonds yield a higher effective interest rate than their coupon rate, compensating investors for the lower initial price. Such pricing impacts the issuer's cost of capital and the investor's yield-to-maturity calculations.

Investment Objectives

Investment objectives define the specific financial goals that guide an investor's decision-making process, such as capital appreciation, income generation, or wealth preservation. These objectives are critical in shaping portfolio allocation strategies, balancing risk tolerance with expected returns over a defined investment horizon. Investors often align their objectives with benchmarks like the S&P 500 for growth or Bloomberg Barclays U.S. Aggregate Bond Index for income-focused portfolios. Clear investment objectives facilitate performance measurement and risk management, ensuring that portfolio outcomes meet the investor's long-term financial plans.

Source and External Links

Bond Basics: Zero-Coupon Bonds - Kiplinger - Zero-coupon bonds pay no periodic interest but are sold at a substantial discount to their face value, with full payment made at maturity, unlike conventional coupon bonds that make regular interest payments.

Zero Coupon Bonds vs Regular Bonds - Kotak Securities - Zero-coupon bonds do not pay periodic interest and have higher price volatility but eliminate reinvestment risk, making them suitable for long horizons, whereas regular bonds pay steady interest and are less volatile.

Zero Coupon Bond Vs Regular Coupon Bond - Fintelligents - Regular coupon bonds provide periodic interest payments and return principal at maturity, while zero-coupon bonds are issued at a discount and only pay the face value at maturity without interim interest.

FAQs

What is a bond?

A bond is a fixed-income security representing a loan made by an investor to a borrower, typically corporations or governments, with a promise to repay principal plus interest at a specified maturity date.

What is a zero-coupon bond?

A zero-coupon bond is a debt security that does not pay periodic interest and is issued at a discount to its face value, with the full face value repaid at maturity.

What is a coupon bond?

A coupon bond is a debt security that pays fixed periodic interest payments, called coupons, to the bondholder until maturity, when the principal amount is repaid.

How does a zero-coupon bond generate returns?

A zero-coupon bond generates returns by being issued at a discount to its face value and paying no periodic interest, with the investor receiving the full face value at maturity, resulting in the return from the difference between purchase price and maturity value.

How are coupon bonds structured?

Coupon bonds are structured with a face value, a fixed interest rate (coupon rate), periodic interest payments (coupons) to bondholders, and a maturity date at which the principal is repaid.

What are the main differences between zero-coupon bonds and coupon bonds?

Zero-coupon bonds pay no periodic interest and are issued at a discount to face value, maturing at par, while coupon bonds pay regular interest payments (coupons) and return the face value at maturity.

Which bond type is better for long-term investors?

Government bonds are better for long-term investors due to their lower risk and stable returns.