Value at Risk (VaR) quantifies the maximum potential loss over a specific time frame at a given confidence level, serving as a standard risk assessment tool in finance. Expected Shortfall (ES), also known as Conditional VaR, measures the average loss beyond the VaR threshold, providing a more comprehensive view of tail risk and extreme market events. Explore the distinctions between VaR and ES to enhance your understanding of risk management methodologies.

Main Difference

Value at Risk (VaR) measures the maximum potential loss over a specified time frame at a given confidence level, focusing on the threshold loss that is not expected to be exceeded. Expected Shortfall (ES), also known as Conditional VaR, calculates the average loss given that the loss has exceeded the VaR threshold, providing insight into the tail risk beyond the VaR cutoff. Unlike VaR, ES captures the severity of extreme losses and is coherent, satisfying properties such as subadditivity. Financial institutions prefer ES for risk management since it offers a more comprehensive assessment of potential downside risk in extreme market conditions.

Connection

Value at Risk (VaR) estimates the maximum potential loss over a specified time horizon at a given confidence level, while Expected Shortfall (ES) measures the average loss exceeding the VaR threshold, providing a deeper insight into tail risk. Both metrics are fundamental in risk management frameworks, with ES offering a coherent risk measure that addresses VaR's limitations by capturing the magnitude of extreme losses. Regulatory standards such as Basel III increasingly emphasize ES for its ability to better quantify potential losses in adverse market conditions.

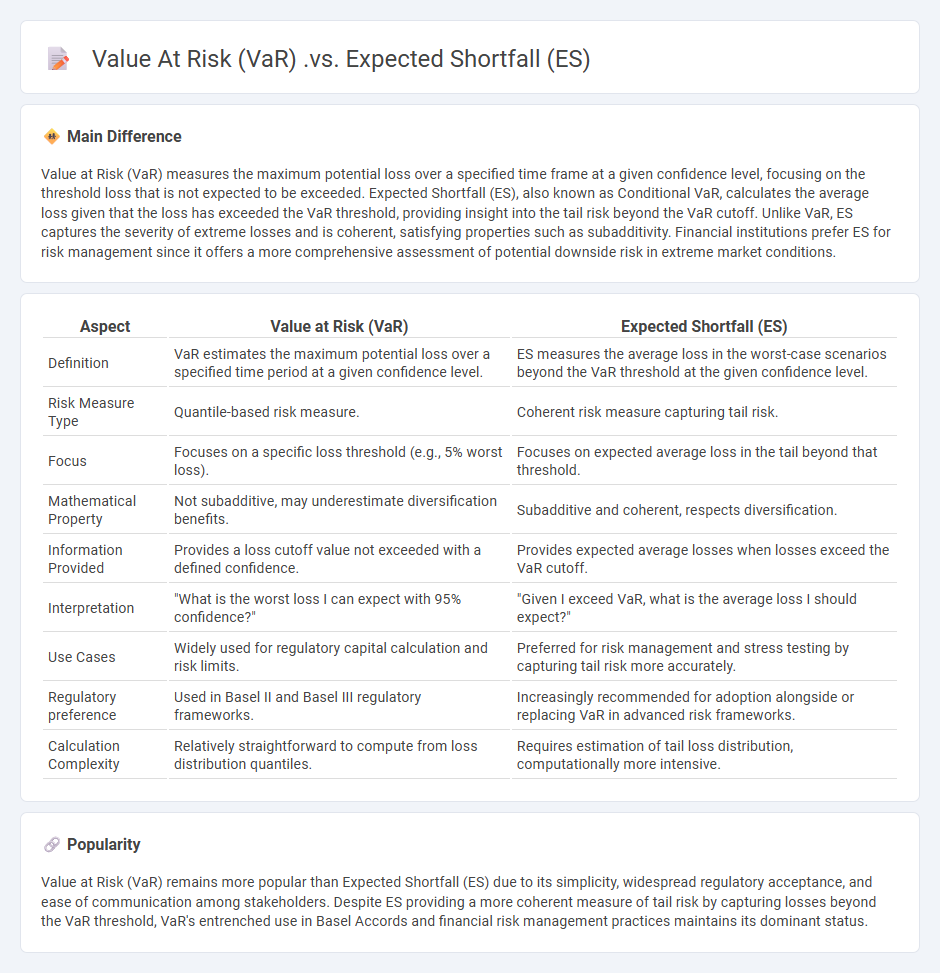

Comparison Table

| Aspect | Value at Risk (VaR) | Expected Shortfall (ES) |

|---|---|---|

| Definition | VaR estimates the maximum potential loss over a specified time period at a given confidence level. | ES measures the average loss in the worst-case scenarios beyond the VaR threshold at the given confidence level. |

| Risk Measure Type | Quantile-based risk measure. | Coherent risk measure capturing tail risk. |

| Focus | Focuses on a specific loss threshold (e.g., 5% worst loss). | Focuses on expected average loss in the tail beyond that threshold. |

| Mathematical Property | Not subadditive, may underestimate diversification benefits. | Subadditive and coherent, respects diversification. |

| Information Provided | Provides a loss cutoff value not exceeded with a defined confidence. | Provides expected average losses when losses exceed the VaR cutoff. |

| Interpretation | "What is the worst loss I can expect with 95% confidence?" | "Given I exceed VaR, what is the average loss I should expect?" |

| Use Cases | Widely used for regulatory capital calculation and risk limits. | Preferred for risk management and stress testing by capturing tail risk more accurately. |

| Regulatory preference | Used in Basel II and Basel III regulatory frameworks. | Increasingly recommended for adoption alongside or replacing VaR in advanced risk frameworks. |

| Calculation Complexity | Relatively straightforward to compute from loss distribution quantiles. | Requires estimation of tail loss distribution, computationally more intensive. |

Risk Measurement

Risk measurement in finance quantifies the potential loss associated with investments, using metrics such as Value at Risk (VaR), Conditional Value at Risk (CVaR), and standard deviation. These tools assess market, credit, liquidity, and operational risks within portfolios to ensure compliance with regulatory frameworks like Basel III and Solvency II. Advanced risk measurement employs techniques including Monte Carlo simulations and stress testing to capture extreme market scenarios. Financial institutions integrate risk measurement with asset allocation strategies to optimize returns while maintaining acceptable risk levels.

Tail Risk

Tail risk refers to the probability of extreme losses in financial markets that lie outside the normal distribution curve, often associated with rare but severe events. These risks occur in the tails of the distribution and can result in losses beyond what standard risk models predict, impacting portfolio performance significantly. Investors and risk managers use measures like Value at Risk (VaR) and Conditional Value at Risk (CVaR) to quantify tail risk. Strategies to mitigate tail risk include diversification, hedging with options, and stress testing portfolios against historical market crashes.

Quantile (VaR) vs Average Shortfall (ES)

Value at Risk (VaR) estimates the maximum potential loss within a specific confidence interval over a defined time horizon, commonly used at 95% or 99% levels. Expected Shortfall (ES), also known as Conditional VaR, measures the average loss exceeding the VaR threshold, providing a more comprehensive risk assessment during extreme market downturns. Unlike VaR, ES captures tail risk by considering the severity of losses beyond the quantile cutoff, making it a coherent risk measure favored under Basel III regulations. Financial institutions leverage ES for stress testing and capital allocation to better withstand rare but catastrophic financial events.

Portfolio Risk Management

Portfolio risk management involves identifying, assessing, and mitigating potential losses within a financial investment portfolio. Techniques include diversification across asset classes, asset allocation strategies, and the use of financial derivatives such as options and futures to hedge against market volatility. Quantitative models like Value at Risk (VaR), Conditional Value at Risk (CVaR), and Monte Carlo simulations provide predictive insights on portfolio exposure to various risk factors. Regulatory frameworks such as Basel III and the Dodd-Frank Act mandate risk management practices to enhance financial stability and protect investor interests.

Regulatory Compliance

Regulatory compliance in finance involves adhering to laws, regulations, and guidelines set by governing bodies such as the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA). Financial institutions must implement robust risk management frameworks to prevent fraud, money laundering, and ensure transparency in transactions. Compliance requirements include accurate reporting, ongoing audits, and maintaining records as mandated by regulations like the Dodd-Frank Act and Basel III standards. Failure to comply can result in significant fines, legal penalties, and reputational damage for banks, investment firms, and insurance companies.

Source and External Links

Value at Risk (VaR) vs Expected Shortfall (ES) - Forrs.de - Expected Shortfall provides a more comprehensive risk assessment than VaR by considering not only the loss threshold but also the severity of losses beyond that threshold, making it more informative especially in volatile markets and financial crises.

Comparative Analyses of Expected Shortfall and Value-at-Risk - Expected Shortfall (also called conditional VaR) measures the average loss exceeding the VaR threshold, is sub-additive, easily decomposed and optimized, while VaR can underestimate tail losses and is not sub-additive.

Which is better, ES or VaR? - Models and risk - Although VaR can be estimated more accurately at high confidence levels than ES, ES at slightly lower confidence levels offers better risk sensitivity by capturing tail risks beyond VaR and thus provides a more meaningful risk measure for extreme losses.