Broker-dealers facilitate the buying and selling of securities by acting as intermediaries between buyers and sellers, executing trades on behalf of clients while also trading for their own accounts. Market makers provide liquidity by continuously quoting bid and ask prices for specific securities, ready to buy or sell at those prices to ensure smooth market operations. Discover the key differences and roles these entities play in financial markets to better understand trading dynamics.

Main Difference

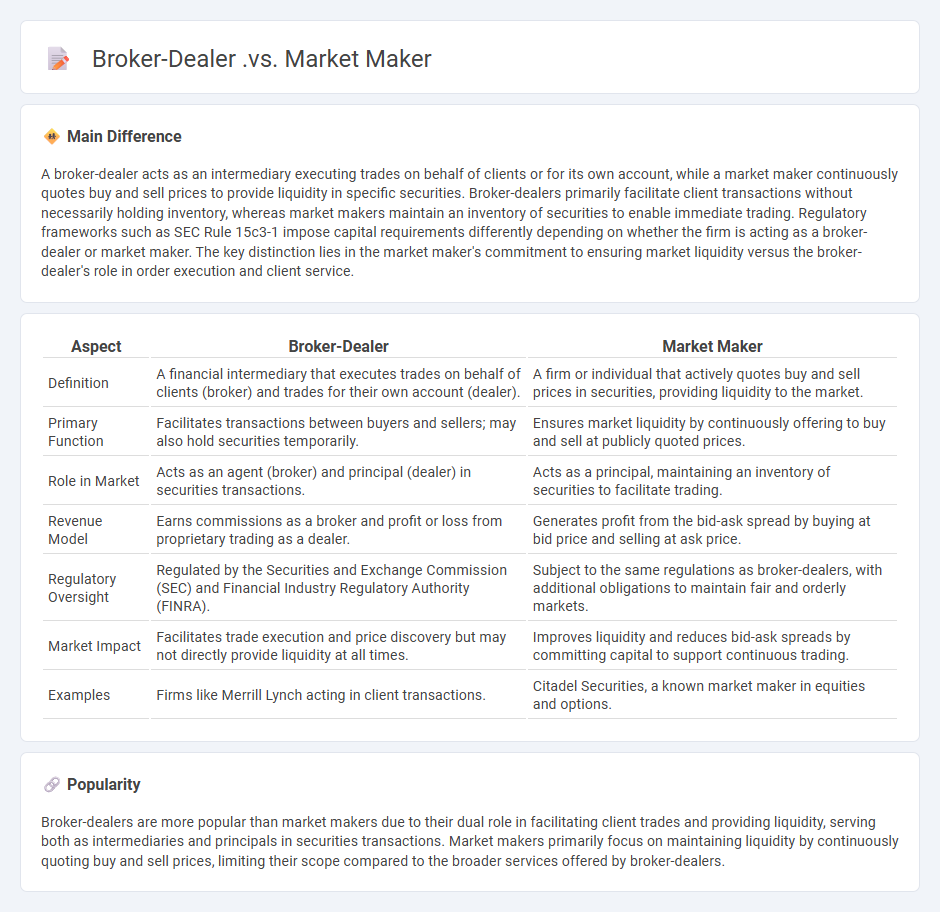

A broker-dealer acts as an intermediary executing trades on behalf of clients or for its own account, while a market maker continuously quotes buy and sell prices to provide liquidity in specific securities. Broker-dealers primarily facilitate client transactions without necessarily holding inventory, whereas market makers maintain an inventory of securities to enable immediate trading. Regulatory frameworks such as SEC Rule 15c3-1 impose capital requirements differently depending on whether the firm is acting as a broker-dealer or market maker. The key distinction lies in the market maker's commitment to ensuring market liquidity versus the broker-dealer's role in order execution and client service.

Connection

Broker-dealers facilitate client orders by executing trades, often relying on market makers who provide liquidity through continuous bid and ask quotes. Market makers help broker-dealers reduce transaction costs and improve trade execution speed by maintaining active inventories of securities. This symbiotic relationship enhances market efficiency and ensures smoother trading operations across exchanges.

Comparison Table

| Aspect | Broker-Dealer | Market Maker |

|---|---|---|

| Definition | A financial intermediary that executes trades on behalf of clients (broker) and trades for their own account (dealer). | A firm or individual that actively quotes buy and sell prices in securities, providing liquidity to the market. |

| Primary Function | Facilitates transactions between buyers and sellers; may also hold securities temporarily. | Ensures market liquidity by continuously offering to buy and sell at publicly quoted prices. |

| Role in Market | Acts as an agent (broker) and principal (dealer) in securities transactions. | Acts as a principal, maintaining an inventory of securities to facilitate trading. |

| Revenue Model | Earns commissions as a broker and profit or loss from proprietary trading as a dealer. | Generates profit from the bid-ask spread by buying at bid price and selling at ask price. |

| Regulatory Oversight | Regulated by the Securities and Exchange Commission (SEC) and Financial Industry Regulatory Authority (FINRA). | Subject to the same regulations as broker-dealers, with additional obligations to maintain fair and orderly markets. |

| Market Impact | Facilitates trade execution and price discovery but may not directly provide liquidity at all times. | Improves liquidity and reduces bid-ask spreads by committing capital to support continuous trading. |

| Examples | Firms like Merrill Lynch acting in client transactions. | Citadel Securities, a known market maker in equities and options. |

Liquidity Provision

Liquidity provision in finance refers to the process by which market participants facilitate trading by offering to buy and sell assets, ensuring smooth and continuous market operations. Market makers and institutional investors play a critical role in maintaining liquidity by narrowing bid-ask spreads and absorbing order flow imbalances. High-frequency trading firms often enhance liquidity through rapid order placement and cancellation, contributing to efficient price discovery. Robust liquidity provision reduces transaction costs and market volatility, benefiting both retail and institutional traders.

Order Execution

Order execution in finance refers to the process of completing buy or sell orders for securities on behalf of investors. Efficient order execution affects transaction costs, speed, and price optimization, impacting overall portfolio performance. Market participants use advanced trading algorithms and electronic communication networks (ECNs) to achieve best execution, ensuring favorable trade conditions. Regulatory frameworks like MiFID II in Europe mandate transparency and fairness in order execution practices.

Bid-Ask Spread

The bid-ask spread represents the difference between the highest price a buyer is willing to pay (bid) and the lowest price a seller is willing to accept (ask) for a security in financial markets. This spread serves as a key indicator of market liquidity and trading costs, with narrower spreads typically reflecting more liquid assets like blue-chip stocks or major currency pairs. In stock markets, the bid-ask spread can fluctuate based on supply and demand dynamics, trading volume, and market volatility. Market makers and liquidity providers often earn profits from the bid-ask spread by facilitating trades between buyers and sellers.

Agency vs Principal

In finance, the agency relationship involves a principal who delegates decision-making authority to an agent to act on their behalf, often seen in corporate management where shareholders (principals) appoint executives (agents) to run the company. Agency costs arise from conflicts of interest when agents prioritize personal gains over principals' wealth maximization, necessitating mechanisms like performance-based incentives and monitoring. Principal-agent problems are critical in investment management, where fund managers (agents) may not always act in the best interest of investors (principals). Effective governance structures aim to align incentives and reduce information asymmetry between principals and agents.

Regulatory Compliance

Regulatory compliance in finance ensures institutions adhere to laws such as the Dodd-Frank Act, Basel III, and Anti-Money Laundering (AML) regulations. Financial firms implement compliance programs to mitigate risks, avoid penalties, and maintain operational integrity. Key components include Know Your Customer (KYC) protocols, transaction monitoring, and regular audits by regulatory bodies like the SEC and FINRA. Staying compliant supports market stability and protects consumer interests in the financial ecosystem.

Source and External Links

Brokers vs. Dealers: What's the Difference? - Brokers act as intermediaries helping clients buy and sell securities for a commission, while dealers buy and sell securities for their own account, setting prices and profiting from spreads themselves.

Market Maker Brokers - Market makers are firms or brokers that provide liquidity by standing ready to buy and sell securities from their own accounts at quoted bid-ask prices, profiting from the spread, thus facilitating faster trades.

Roles | The secondary market | Achievable SIE - Market makers trade securities on a principal basis by maintaining bid and ask prices to provide liquidity, often filling trade requests initiated by broker-dealers who act as intermediaries on behalf of clients.

FAQs

What is a broker-dealer?

A broker-dealer is a financial firm or individual that buys and sells securities on behalf of clients (broker) and for their own account (dealer), regulated by the SEC and FINRA.

What is a market maker?

A market maker is a financial firm or individual that continuously provides buy and sell quotes for a specific asset, ensuring liquidity and facilitating smooth trading on an exchange.

How do broker-dealers and market makers differ?

Broker-dealers act as agents executing client orders and may also trade securities for their own accounts, while market makers continuously quote buy and sell prices to provide liquidity and facilitate trading in specific securities.

What role does a broker-dealer play in trading?

A broker-dealer facilitates securities trading by acting as an agent executing orders for clients or as a principal buying and selling securities for its own account.

What does a market maker do in the market?

A market maker provides liquidity by continuously quoting buy and sell prices for financial instruments, facilitating smooth trading and reducing price volatility.

Can a broker-dealer also be a market maker?

Yes, a broker-dealer can also act as a market maker by quoting buy and sell prices and standing ready to trade securities from their own inventory.

Why are market makers important to liquidity?

Market makers provide continuous bid and ask prices, facilitating smoother transactions and ensuring sufficient liquidity in financial markets.