Agency theory focuses on the conflicts of interest between principals and agents, emphasizing mechanisms to align managers' actions with shareholders' goals. Stewardship theory suggests that managers act as stewards whose interests are aligned with the organization's, promoting trust and collaboration. Explore the key differences and applications of these governance theories to enhance organizational management.

Main Difference

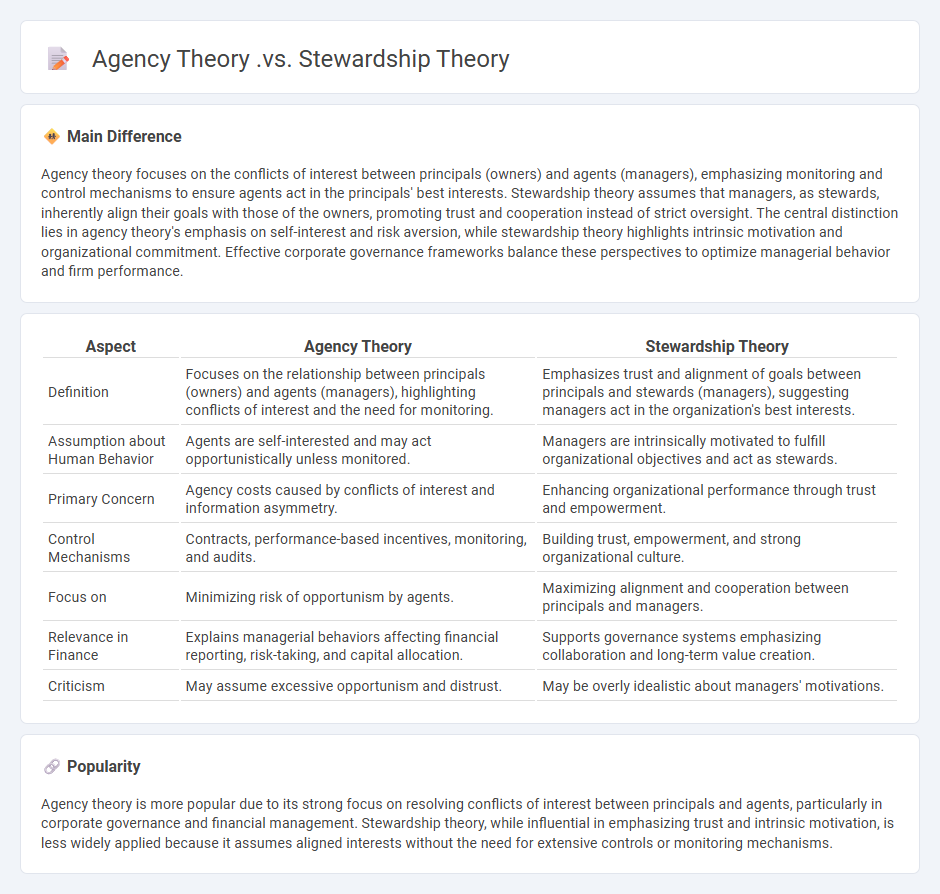

Agency theory focuses on the conflicts of interest between principals (owners) and agents (managers), emphasizing monitoring and control mechanisms to ensure agents act in the principals' best interests. Stewardship theory assumes that managers, as stewards, inherently align their goals with those of the owners, promoting trust and cooperation instead of strict oversight. The central distinction lies in agency theory's emphasis on self-interest and risk aversion, while stewardship theory highlights intrinsic motivation and organizational commitment. Effective corporate governance frameworks balance these perspectives to optimize managerial behavior and firm performance.

Connection

Agency theory and Stewardship theory both address the relationship between principals and agents in organizational governance, focusing on how managers (agents) align their actions with owners' (principals) interests. Agency theory assumes potential conflicts due to self-interest and requires monitoring and incentives to mitigate risks, while Stewardship theory views managers as motivated by intrinsic goals, promoting trust and collaboration for organizational success. These theories provide complementary perspectives on governance mechanisms to enhance accountability and performance in corporate management.

Comparison Table

| Aspect | Agency Theory | Stewardship Theory |

|---|---|---|

| Definition | Focuses on the relationship between principals (owners) and agents (managers), highlighting conflicts of interest and the need for monitoring. | Emphasizes trust and alignment of goals between principals and stewards (managers), suggesting managers act in the organization's best interests. |

| Assumption about Human Behavior | Agents are self-interested and may act opportunistically unless monitored. | Managers are intrinsically motivated to fulfill organizational objectives and act as stewards. |

| Primary Concern | Agency costs caused by conflicts of interest and information asymmetry. | Enhancing organizational performance through trust and empowerment. |

| Control Mechanisms | Contracts, performance-based incentives, monitoring, and audits. | Building trust, empowerment, and strong organizational culture. |

| Focus on | Minimizing risk of opportunism by agents. | Maximizing alignment and cooperation between principals and managers. |

| Relevance in Finance | Explains managerial behaviors affecting financial reporting, risk-taking, and capital allocation. | Supports governance systems emphasizing collaboration and long-term value creation. |

| Criticism | May assume excessive opportunism and distrust. | May be overly idealistic about managers' motivations. |

Principal-Agent Conflict

The principal-agent conflict arises when the interests of principals (shareholders) diverge from those of agents (company executives), leading to potential inefficiencies in financial decision-making. This agency problem often results in agents pursuing personal goals over maximizing shareholder value, impacting corporate governance and shareholder returns. Mechanisms such as performance-based incentives, monitoring by boards of directors, and shareholder activism are critical in aligning interests and mitigating conflicts. Effective resolution of principal-agent issues enhances firm valuation and ensures optimal allocation of financial resources.

Managerial Motivation

Managerial motivation in finance significantly influences corporate decision-making and firm performance. Incentive-based compensation, such as stock options and bonuses, aligns managers' interests with shareholders, encouraging value maximization. Behavioral finance studies reveal that overconfidence and risk aversion impact financial strategies, affecting investment and financing decisions. Empirical research from institutions like the National Bureau of Economic Research (NBER) highlights the role of managerial incentives in capital structure optimization and earnings management.

Risk Tolerance

Risk tolerance in finance measures an investor's ability and willingness to endure market volatility and potential losses in their investment portfolio. It depends on factors such as age, income, financial goals, investment horizon, and psychological comfort with uncertainty. Understanding risk tolerance assists in creating diversified portfolios tailored to balance potential returns against acceptable levels of risk. Financial advisors often use risk tolerance questionnaires to identify suitable asset allocations for individual investors.

Governance Mechanisms

Governance mechanisms in finance play a critical role in aligning the interests of shareholders and management, ensuring transparency, and minimizing agency costs. Effective mechanisms include board oversight, shareholder voting rights, executive compensation linked to performance, and regulatory compliance frameworks such as Sarbanes-Oxley Act. Studies show firms with strong governance structures exhibit higher firm value, lower capital costs, and improved financial performance. Institutional investors and proxy advisory firms also significantly influence governance practices, promoting accountability and sustainable growth.

Organizational Alignment

Organizational alignment in finance ensures that financial strategies, goals, and resources are consistently coordinated across departments to drive overall business performance. Strong alignment improves budgeting accuracy, enhances risk management, and supports regulatory compliance by integrating financial planning with operational objectives. Companies like JPMorgan Chase and Goldman Sachs leverage organizational alignment to optimize capital allocation and maximize shareholder value. Effective communication between finance leaders and other business units is essential for maintaining alignment and responding swiftly to market changes.

Source and External Links

Difference Between the Agency Theory and Stewardship Theory - Agency theory assumes managers act in self-interest and require strict monitoring and performance incentives, while stewardship theory assumes managers act as loyal stewards working in the company's best interest, thriving under empowerment, trust, and long-term vision.

A Symphony of Agency and Stewardship Values Ensures Family Business Success - Agency theory frames the manager-shareholder relationship as contractual and conflict-prone due to divergent interests, whereas stewardship theory sees it as collaborative, with aligned interests and a shared commitment to organizational success.

Difference Between Agency Theory and Stewardship Theory - Agency theory is rooted in economics and extrinsic motivation, viewing managers as self-serving agents requiring governance to curb opportunism, while stewardship theory is based on psychology and intrinsic motivation, viewing managers as pro-organizational stewards whose personal success is tied to the company's success.

FAQs

What is Agency Theory in management?

Agency Theory in management explains the relationship between principals (owners) and agents (managers), focusing on resolving conflicts of interest through contracts and incentives.

What is Stewardship Theory in organizations?

Stewardship Theory in organizations posits that managers act as stewards whose interests align with organizational goals, prioritizing collective success over personal gain.

How does Agency Theory compare to Stewardship Theory?

Agency Theory focuses on conflicts of interest between principals and agents, emphasizing monitoring and control mechanisms, while Stewardship Theory assumes managers act as responsible stewards whose goals align with organizational objectives, prioritizing trust and empowerment.

What are the main assumptions of Agency Theory?

Agency Theory assumes that principals delegate work to agents who have different information and goals, agents are self-interested and may act opportunistically, there is information asymmetry causing monitoring costs for principals, and contracts are designed to align interests and control agent behavior.

What are the primary beliefs of Stewardship Theory?

Stewardship Theory primarily believes that managers, as stewards, are motivated to act in the best interests of shareholders, prioritizing organizational success over personal gain, emphasizing trust, intrinsic motivation, and aligned goals between managers and owners.

How do Agency and Stewardship theories view managers?

Agency theory views managers as agents who may prioritize personal interests over shareholders' goals, requiring monitoring and incentives to align actions; stewardship theory views managers as stewards motivated to act in the best interests of owners, emphasizing trust and intrinsic motivation.

Which situations favor Agency Theory over Stewardship Theory?

Agency Theory is favored in situations with divergent goals between principals and agents, high performance measurement difficulties, significant information asymmetry, and when agents have strong incentives for self-interest over organizational objectives.