Subordinated debt ranks below senior debt in the hierarchy of claims on assets and earnings, resulting in higher risk and typically higher interest rates for investors. Senior debt holds priority during liquidation and repayment processes, ensuring lower risk and often secured collateral. Explore the critical differences between subordinated and senior debt to optimize your investment strategy.

Main Difference

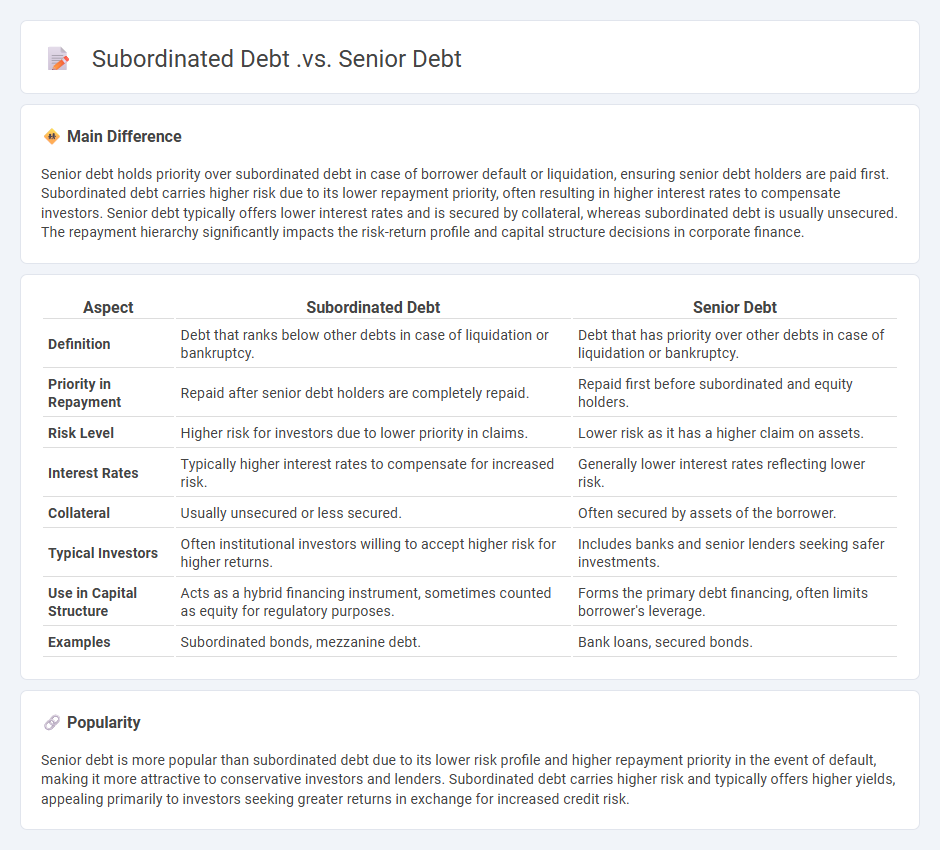

Senior debt holds priority over subordinated debt in case of borrower default or liquidation, ensuring senior debt holders are paid first. Subordinated debt carries higher risk due to its lower repayment priority, often resulting in higher interest rates to compensate investors. Senior debt typically offers lower interest rates and is secured by collateral, whereas subordinated debt is usually unsecured. The repayment hierarchy significantly impacts the risk-return profile and capital structure decisions in corporate finance.

Connection

Subordinated debt ranks below senior debt in the capital structure, meaning its holders are paid after senior debt holders in case of liquidation. Senior debt carries lower risk and typically has lower interest rates, while subordinated debt offers higher yields due to increased risk. This hierarchical relationship affects the cost of capital and priority of claims among creditors.

Comparison Table

| Aspect | Subordinated Debt | Senior Debt |

|---|---|---|

| Definition | Debt that ranks below other debts in case of liquidation or bankruptcy. | Debt that has priority over other debts in case of liquidation or bankruptcy. |

| Priority in Repayment | Repaid after senior debt holders are completely repaid. | Repaid first before subordinated and equity holders. |

| Risk Level | Higher risk for investors due to lower priority in claims. | Lower risk as it has a higher claim on assets. |

| Interest Rates | Typically higher interest rates to compensate for increased risk. | Generally lower interest rates reflecting lower risk. |

| Collateral | Usually unsecured or less secured. | Often secured by assets of the borrower. |

| Typical Investors | Often institutional investors willing to accept higher risk for higher returns. | Includes banks and senior lenders seeking safer investments. |

| Use in Capital Structure | Acts as a hybrid financing instrument, sometimes counted as equity for regulatory purposes. | Forms the primary debt financing, often limits borrower's leverage. |

| Examples | Subordinated bonds, mezzanine debt. | Bank loans, secured bonds. |

Seniority

Seniority in finance refers to the priority level of debt or claims during liquidation or bankruptcy, determining the order in which creditors are paid. Senior debt holders have the highest repayment priority, often secured by collateral, reducing their risk compared to subordinated or junior debt holders. This hierarchy impacts interest rates, with senior debt typically offering lower yields due to its lower risk profile. Corporate bonds issued by companies often specify seniority to inform investors about their relative risk and claim status.

Collateral

Collateral in finance refers to an asset pledged by a borrower to secure a loan or credit, providing the lender with a form of protection against default. Common types of collateral include real estate, vehicles, equipment, and financial securities such as stocks or bonds. The value and liquidity of collateral influence loan terms, interest rates, and approval decisions by financial institutions. Effective collateral management reduces credit risk and enhances borrowing capacity for individuals and businesses.

Repayment Priority

Repayment priority in finance determines the order in which creditors are paid during a liquidation or bankruptcy event, impacting the recoverable amount each creditor receives. Senior debt holders typically hold the highest priority, followed by subordinated debt, mezzanine financing, and equity investors at the lowest tier. This structured hierarchy minimizes risk for lenders with prioritized claims, influencing loan pricing and investment strategies. Understanding repayment priority is essential for accurately assessing credit risk and capital structure in corporate finance.

Interest Rates

Interest rates represent the cost of borrowing money or the return on investment for lending funds, typically expressed as an annual percentage rate (APR). Central banks, such as the Federal Reserve in the United States, influence interest rates to control inflation and stimulate economic growth. Changes in interest rates impact consumer loans, mortgages, and savings accounts, affecting overall financial markets and economic activity. Investors and businesses closely monitor interest rates to make informed decisions regarding financing and investments.

Risk Exposure

Risk exposure in finance quantifies the potential losses an investor or institution may face due to market fluctuations, credit defaults, or operational failures. It encompasses various types such as market risk, credit risk, liquidity risk, and operational risk, each measurable through metrics like Value at Risk (VaR) and Expected Shortfall. Financial institutions implement risk management frameworks, including stress testing and scenario analysis, to monitor and mitigate exposure effectively. Accurate risk exposure assessment supports regulatory compliance and strategic decision-making in asset allocation and portfolio management.

Source and External Links

The Difference Between Senior Debt and Subordinated Debt - This webpage explains the key differences between senior and subordinated debt, focusing on repayment priority, interest rates, collateral, and covenants.

Subordinated Debt - This resource provides an overview of subordinated debt characteristics, its positioning in the capital structure, and how it compares to senior debt in terms of risk and interest rates.

What is subordinated debt? - This article discusses subordinated debt as Tier 2 capital, highlighting its features such as fixed maturity, non-discretionary coupons, and risk characteristics compared to senior debt.

FAQs

What is senior debt?

Senior debt is a type of loan or credit obligation that has priority over other unsecured or junior debts in case of borrower default or bankruptcy, ensuring senior debt holders are paid first.

What is subordinated debt?

Subordinated debt is a type of loan or bond that ranks below other debts in case of borrower bankruptcy, meaning it is repaid after senior debt claims.

What are the main differences between senior debt and subordinated debt?

Senior debt has higher repayment priority and lower interest rates; subordinated debt has lower repayment priority and higher interest rates due to increased risk.

Why do companies issue subordinated debt?

Companies issue subordinated debt to raise capital while offering higher interest rates to attract investors willing to accept greater risk, enhance leverage without diluting equity, and prioritize senior creditors in case of bankruptcy.

How are risks different in senior and subordinated debt?

Senior debt carries lower risk due to priority in repayment and collateral claims, while subordinated debt involves higher risk because it is repaid only after senior debt obligations are fulfilled, often lacking collateral security.

Which gets repaid first in a bankruptcy, senior debt or subordinated debt?

Senior debt gets repaid first in a bankruptcy before subordinated debt.

How does interest rate differ between senior and subordinated debt?

Senior debt typically carries lower interest rates than subordinated debt due to higher repayment priority and lower risk for lenders.