The Dividend Discount Model (DDM) values a company based on the present value of expected future dividends, assuming dividends directly reflect corporate profitability. The Free Cash Flow model (FCF) assesses firm value by discounting all available cash flows to both equity and debt holders, providing a broader picture of financial health. Explore deeper insights into how these models impact investment decisions and valuation accuracy.

Main Difference

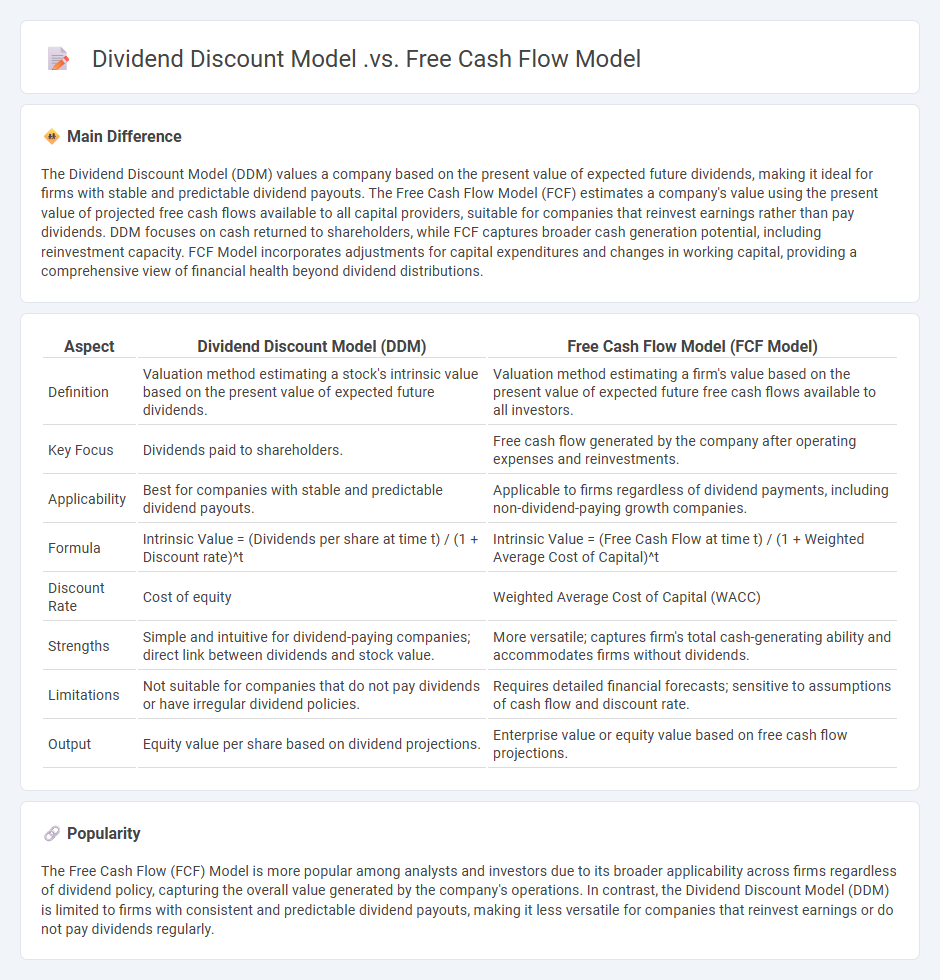

The Dividend Discount Model (DDM) values a company based on the present value of expected future dividends, making it ideal for firms with stable and predictable dividend payouts. The Free Cash Flow Model (FCF) estimates a company's value using the present value of projected free cash flows available to all capital providers, suitable for companies that reinvest earnings rather than pay dividends. DDM focuses on cash returned to shareholders, while FCF captures broader cash generation potential, including reinvestment capacity. FCF Model incorporates adjustments for capital expenditures and changes in working capital, providing a comprehensive view of financial health beyond dividend distributions.

Connection

The Dividend Discount Model (DDM) and Free Cash Flow Model (FCF) are connected through their shared goal of valuing a firm's intrinsic worth based on expected future cash flows. While DDM focuses specifically on dividends as cash flows to equity shareholders, the FCF model estimates cash flows available to all capital providers, encompassing debt and equity. Both models rely on discounting these future cash flows to present value using appropriate cost of capital metrics, providing complementary perspectives on firm valuation.

Comparison Table

| Aspect | Dividend Discount Model (DDM) | Free Cash Flow Model (FCF Model) |

|---|---|---|

| Definition | Valuation method estimating a stock's intrinsic value based on the present value of expected future dividends. | Valuation method estimating a firm's value based on the present value of expected future free cash flows available to all investors. |

| Key Focus | Dividends paid to shareholders. | Free cash flow generated by the company after operating expenses and reinvestments. |

| Applicability | Best for companies with stable and predictable dividend payouts. | Applicable to firms regardless of dividend payments, including non-dividend-paying growth companies. |

| Formula | Intrinsic Value = (Dividends per share at time t) / (1 + Discount rate)^t | Intrinsic Value = (Free Cash Flow at time t) / (1 + Weighted Average Cost of Capital)^t |

| Discount Rate | Cost of equity | Weighted Average Cost of Capital (WACC) |

| Strengths | Simple and intuitive for dividend-paying companies; direct link between dividends and stock value. | More versatile; captures firm's total cash-generating ability and accommodates firms without dividends. |

| Limitations | Not suitable for companies that do not pay dividends or have irregular dividend policies. | Requires detailed financial forecasts; sensitive to assumptions of cash flow and discount rate. |

| Output | Equity value per share based on dividend projections. | Enterprise value or equity value based on free cash flow projections. |

Intrinsic Value

Intrinsic value in finance refers to the true, inherent worth of an asset based on fundamental analysis, excluding market price fluctuations. It is calculated by evaluating tangible factors such as discounted future cash flows, earnings, dividends, and growth rates. Investors use intrinsic value to identify undervalued or overvalued securities, aiming to achieve long-term returns. Notably, Warren Buffett emphasizes intrinsic value as a crucial metric for value investing decisions.

Required Rate of Return

The required rate of return is the minimum annual percentage an investor expects to earn on an investment to compensate for its risk. It varies based on the risk profile of the asset, prevailing interest rates, and market conditions. For stocks, the Capital Asset Pricing Model (CAPM) estimates this rate by adding the risk-free rate to the asset's beta multiplied by the market risk premium. Accurate calculation of this rate is essential for capital budgeting, portfolio management, and determining the feasibility of investment projects.

Dividend Payments

Dividend payments represent the distribution of a portion of a company's earnings to its shareholders, typically issued as cash or additional stock. These payments reflect a company's profitability and cash flow stability, often influencing investor confidence and stock valuation. The frequency of dividends varies, with most companies issuing quarterly payments, while some opt for annual or semi-annual distributions. Analyzing dividend yield and payout ratio offers critical insights into a firm's financial health and shareholder value proposition.

Free Cash Flow to Firm (FCFF)

Free Cash Flow to Firm (FCFF) represents the cash generated by a company's operations available to all capital providers, including debt and equity holders, after accounting for operating expenses and investments in working capital and fixed assets. It is calculated by adding non-cash expenses like depreciation to net income, subtracting capital expenditures, and adjusting for changes in net working capital. FCFF is crucial for valuation models such as the discounted cash flow (DCF) analysis, helping investors assess a firm's intrinsic value independently of its capital structure. Accurate FCFF measurement enables better decision-making regarding investment, financing, and dividend policies.

Terminal Value

Terminal value represents the estimated value of a business or project beyond a forecast period, capturing all future cash flows in perpetuity. It is a crucial component in discounted cash flow (DCF) analysis, often calculated using the Gordon Growth model or exit multiple method. Accurate terminal value estimation significantly influences the overall valuation since it typically accounts for a large portion of the total present value. Analysts must carefully assess growth rates, discount rates, and market conditions to ensure realistic terminal value assumptions.

Source and External Links

FCFF vs FCFE vs Dividends - Definition, When to Use - The Dividend Discount Model (DDM) and Free Cash Flow to Equity (FCFE) approach both value the cash flows available to stockholders, but DDM uses dividends while FCFE uses free cash flows, with FCFE preferred when dividends are unstable; FCFF uses WACC to discount cash flows to the firm, whereas FCFE uses cost of equity only.

Why Is Free Cash Flow Approach Better Than Dividend Discount Model - The Dividend Discount Model relies on dividends as proxies for firm performance which can be misleading since firms can pay dividends while underlying performance declines or forego dividends for growth, whereas Free Cash Flow models directly measure cash available to investors, making them more reliable especially for large shareholders or acquiring firms.

Free Cash Flow Valuation | CFA Institute - Free Cash Flow Models (FCFF and FCFE) are generally favored by analysts over the Dividend Discount Model because they provide an economically sound basis for valuation by focusing on cash flows available to shareholders rather than dividends paid, which can be influenced by company policy; FCFF discounts at WACC and FCFE at cost of equity.

FAQs

What is the Dividend Discount Model?

The Dividend Discount Model (DDM) is a valuation method that calculates a stock's intrinsic value by discounting expected future dividends to their present value using a required rate of return.

What is the Free Cash Flow Model?

The Free Cash Flow Model values a company based on the present value of projected free cash flows, which represent the cash generated after operating expenses and capital expenditures, available for distribution to investors.

How do the models estimate company value?

Models estimate company value by analyzing financial metrics such as discounted cash flows (DCF), earnings, revenue growth, market multiples (P/E ratio, EV/EBITDA), and asset valuations to project future profitability and compare against industry benchmarks.

What are the main assumptions of each model?

The main assumptions of the linear regression model include linearity, independence, homoscedasticity, normality of errors, and no multicollinearity. The logistic regression model assumes independence of observations, linearity of log odds, no multicollinearity, and a large sample size. The decision tree model assumes no prior distribution of data, that data can be split based on feature thresholds, and does not require linear relationships. The neural network model assumes data is sufficiently large and representative, input features capture relevant patterns, and non-linear relationships exist between inputs and outputs.

When should you use the Dividend Discount Model?

Use the Dividend Discount Model when valuing companies with stable, predictable dividend payments and a consistent dividend growth rate.

When is the Free Cash Flow Model preferred?

The Free Cash Flow Model is preferred when evaluating companies with unstable dividends or inconsistent dividend policies, as it focuses on cash flow available to all capital providers rather than dividend payments.

What are the limitations of each valuation method?

Discounted Cash Flow (DCF) relies on accurate future cash flow projections and discount rates, making it sensitive to assumptions. Comparable Company Analysis depends on finding truly comparable firms and current market conditions, which may distort value. Precedent Transactions Analysis can be affected by unique deal circumstances and market anomalies at the time of transactions. Asset-Based Valuation often ignores intangible assets and future earning potential, focusing primarily on book value.