Time-weighted return measures investment performance by eliminating the impact of cash flows, focusing solely on the portfolio's growth rate over specific periods. Money-weighted return, also known as internal rate of return (IRR), accounts for the timing and size of cash flows, reflecting the investor's actual experience. Explore the key differences and applications of these return metrics to better assess investment success.

Main Difference

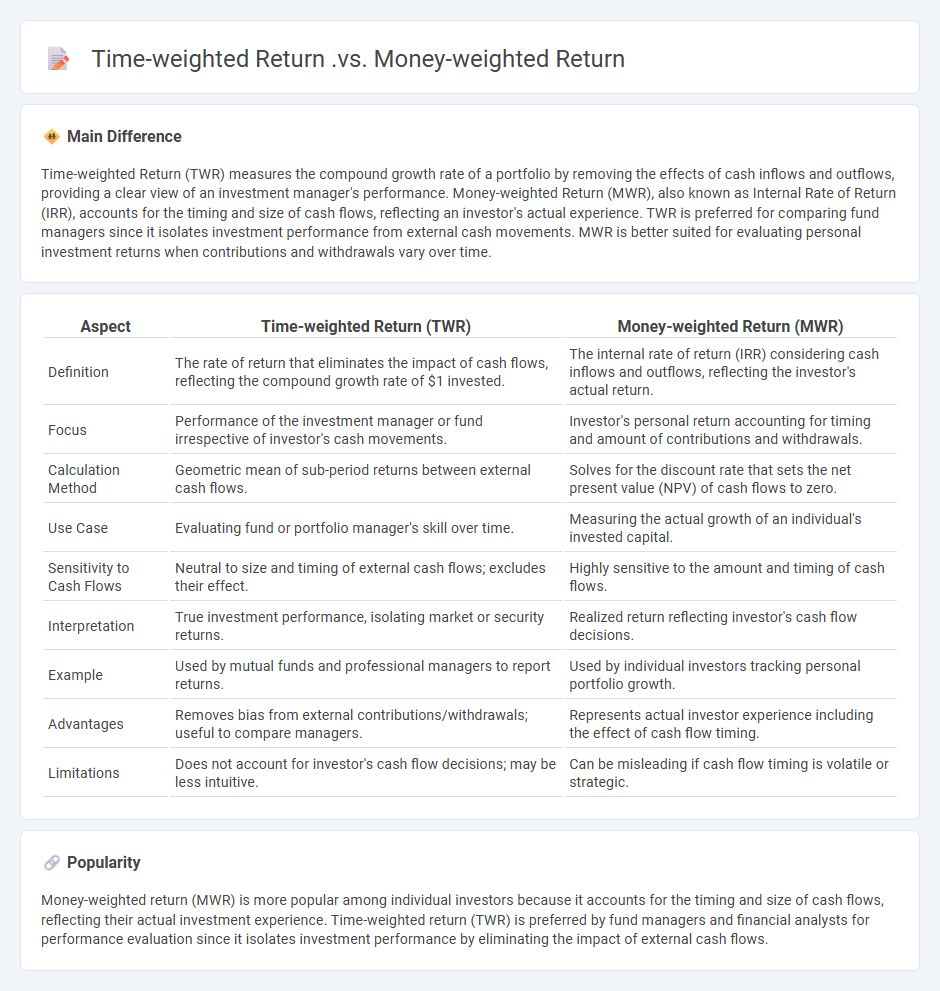

Time-weighted Return (TWR) measures the compound growth rate of a portfolio by removing the effects of cash inflows and outflows, providing a clear view of an investment manager's performance. Money-weighted Return (MWR), also known as Internal Rate of Return (IRR), accounts for the timing and size of cash flows, reflecting an investor's actual experience. TWR is preferred for comparing fund managers since it isolates investment performance from external cash movements. MWR is better suited for evaluating personal investment returns when contributions and withdrawals vary over time.

Connection

Time-weighted return (TWR) and money-weighted return (MWR) both measure investment performance but focus on different aspects of cash flow timing. TWR isolates the compound growth rate of a portfolio by eliminating the impact of external cash flows, making it ideal for comparing fund manager performance. MWR incorporates the timing and size of investor cash flows, capturing the internal rate of return (IRR) relevant for individual investor experience.

Comparison Table

| Aspect | Time-weighted Return (TWR) | Money-weighted Return (MWR) |

|---|---|---|

| Definition | The rate of return that eliminates the impact of cash flows, reflecting the compound growth rate of $1 invested. | The internal rate of return (IRR) considering cash inflows and outflows, reflecting the investor's actual return. |

| Focus | Performance of the investment manager or fund irrespective of investor's cash movements. | Investor's personal return accounting for timing and amount of contributions and withdrawals. |

| Calculation Method | Geometric mean of sub-period returns between external cash flows. | Solves for the discount rate that sets the net present value (NPV) of cash flows to zero. |

| Use Case | Evaluating fund or portfolio manager's skill over time. | Measuring the actual growth of an individual's invested capital. |

| Sensitivity to Cash Flows | Neutral to size and timing of external cash flows; excludes their effect. | Highly sensitive to the amount and timing of cash flows. |

| Interpretation | True investment performance, isolating market or security returns. | Realized return reflecting investor's cash flow decisions. |

| Example | Used by mutual funds and professional managers to report returns. | Used by individual investors tracking personal portfolio growth. |

| Advantages | Removes bias from external contributions/withdrawals; useful to compare managers. | Represents actual investor experience including the effect of cash flow timing. |

| Limitations | Does not account for investor's cash flow decisions; may be less intuitive. | Can be misleading if cash flow timing is volatile or strategic. |

Time-weighted Return (TWR)

Time-weighted Return (TWR) measures the compound growth rate of one unit of currency invested over a specified period, neutralizing the impact of cash flows. It is used extensively in portfolio performance evaluation, reflecting an investment manager's ability independent of deposits and withdrawals. Calculated by geometrically linking sub-period returns between cash flow events, TWR provides a consistent, comparable measure across multiple portfolios or benchmarks. This metric is favored by institutions managing client assets, ensuring transparency and accuracy in performance reporting.

Money-weighted Return (MWR)

Money-weighted return (MWR) measures the performance of an investment portfolio by considering the timing and amount of cash flows. It is calculated as the internal rate of return (IRR) where the net present value of cash inflows and outflows equals zero. MWR reflects the investor's actual experience by incorporating contributions and withdrawals, making it sensitive to the timing of cash flows. This differs from time-weighted return (TWR), which isolates investment performance from external cash flow effects.

Cash Flow Timing

Cash flow timing refers to the scheduling of inflows and outflows of cash within a business, impacting liquidity management and financial planning. Precise forecasting of cash flow timing helps companies ensure they have sufficient funds to cover operational expenses, debt obligations, and investment opportunities. Misalignment in cash flow timing can lead to cash shortages, increasing reliance on credit lines or costly financing options. Effective cash flow management improves financial stability and supports strategic decision-making in corporate finance.

Performance Attribution

Performance attribution in finance evaluates the sources of investment returns by decomposing portfolio performance into individual factors such as asset allocation, security selection, and market timing. This analysis helps portfolio managers understand whether returns stem from systematic risks or active management decisions. Common methodologies include the Brinson-Fachler model and the multi-factor attribution approach, which quantify contributions by sector, style, and security. Accurate performance attribution informs better investment strategies and risk management, enhancing alpha generation.

Internal Rate of Return (IRR)

Internal Rate of Return (IRR) represents the discount rate at which the net present value (NPV) of all cash flows from a particular investment equals zero. Financial analysts use IRR to evaluate the profitability and efficiency of projects, comparing it against the company's required rate of return or cost of capital. A higher IRR indicates a more attractive investment opportunity, with typical benchmarks varying by industry but often ranging between 10% to 20%. Calculating IRR involves iterative methodologies or software tools, as it cannot be derived through a straightforward algebraic formula.

Source and External Links

Time-Weighted Return (TWR) vs. Money Weighted Rate of Return (MWRR) - Time-weighted return eliminates the effect of cash flows in and out, ideal for evaluating manager performance; money-weighted return includes cash flow timing, reflecting actual investor returns and effects of contributions or withdrawals during the period.

Understanding the Differences Between Time-weighted and Money-weighted Returns - Time-weighted return is the industry standard for performance measurement excluding cash flow effects, while money-weighted return incorporates the impact of contributions and withdrawals, showing the investor's real return.

Money-Weighted vs Time-Weighted Returns | CFA Level 1 - Time-weighted return calculates compound growth regardless of cash flows, suitable for assessing fund manager skill, whereas money-weighted return weights returns by the size and timing of cash flows, reflecting investor experience but can misrepresent manager performance.

FAQs

What is a time-weighted return?

A time-weighted return measures an investment's compound growth rate by eliminating the impact of cash flows, reflecting the portfolio manager's performance over specific periods.

What is a money-weighted return?

A money-weighted return measures investment performance by accounting for the timing and size of cash flows, effectively calculating the internal rate of return (IRR) for an investment portfolio.

How do time-weighted and money-weighted returns differ?

Time-weighted returns measure investment performance by eliminating the impact of cash flows, reflecting the compound growth rate over time. Money-weighted returns, or internal rate of return (IRR), account for the timing and size of cash flows, indicating the investor's actual portfolio growth including contributions and withdrawals.

When should time-weighted return be used?

Time-weighted return should be used to measure the performance of an investment portfolio by isolating the impact of the manager's decisions, regardless of cash inflows or outflows.

Why use money-weighted return?

Use money-weighted return to accurately measure investment performance by accounting for cash flow timing and amounts.

How are time-weighted returns calculated?

Time-weighted returns are calculated by dividing the investment period into sub-periods based on cash flows, computing the return for each sub-period, and then multiplying these sub-period returns together to measure the compound growth rate independent of cash flow timing.

What factors affect money-weighted returns?

Money-weighted returns are affected by the timing and size of cash flows, such as contributions and withdrawals, as well as the performance of the underlying investments during the investment period.