Optimal capital structure balances debt and equity to minimize the overall cost of capital while maximizing firm value. The Static Trade-off Theory suggests firms maintain an ideal debt ratio by weighing tax advantages of debt against bankruptcy risks. Explore deeper insights and practical applications of these financial strategies to enhance corporate funding decisions.

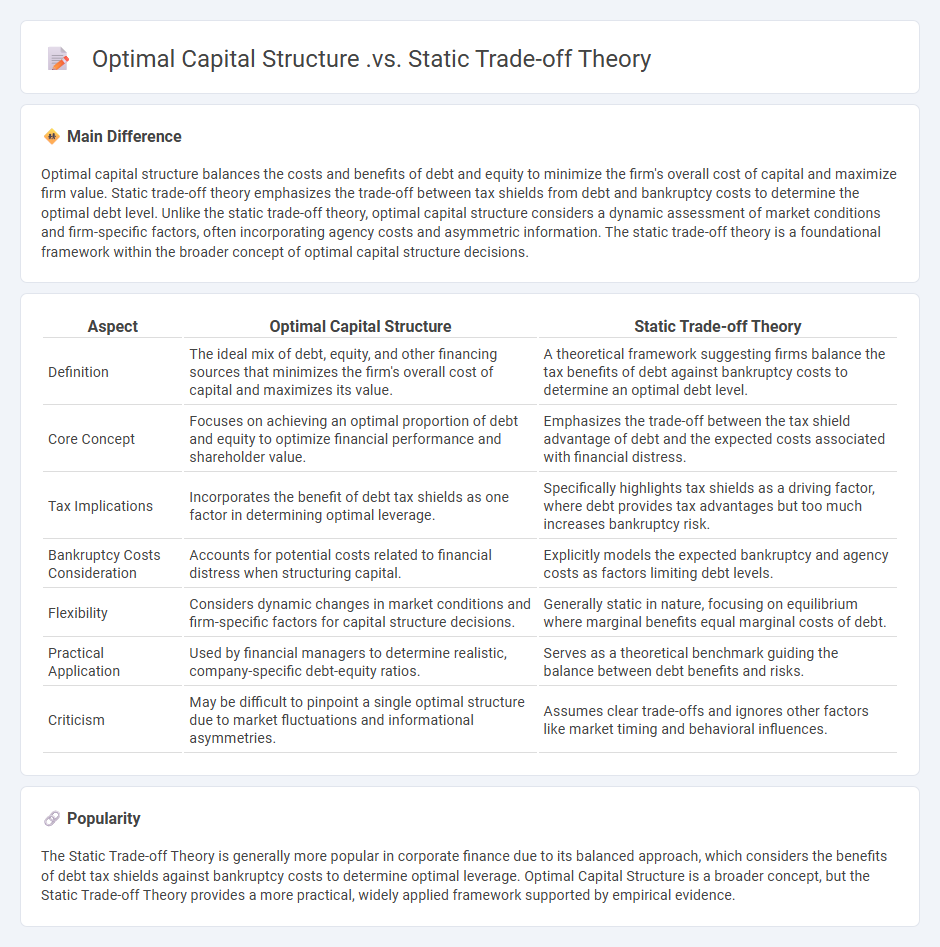

Main Difference

Optimal capital structure balances the costs and benefits of debt and equity to minimize the firm's overall cost of capital and maximize firm value. Static trade-off theory emphasizes the trade-off between tax shields from debt and bankruptcy costs to determine the optimal debt level. Unlike the static trade-off theory, optimal capital structure considers a dynamic assessment of market conditions and firm-specific factors, often incorporating agency costs and asymmetric information. The static trade-off theory is a foundational framework within the broader concept of optimal capital structure decisions.

Connection

Optimal capital structure is achieved by balancing the benefits of debt, such as tax shields, against the costs of financial distress, aligning directly with the static trade-off theory's premise of an equilibrium point. The static trade-off theory quantifies this balance by evaluating the marginal advantage of debt tax shields alongside the marginal costs of bankruptcy and agency problems. Firms utilize this theory to determine their ideal mix of debt and equity, maximizing firm value through minimized weighted average cost of capital (WACC).

Comparison Table

| Aspect | Optimal Capital Structure | Static Trade-off Theory |

|---|---|---|

| Definition | The ideal mix of debt, equity, and other financing sources that minimizes the firm's overall cost of capital and maximizes its value. | A theoretical framework suggesting firms balance the tax benefits of debt against bankruptcy costs to determine an optimal debt level. |

| Core Concept | Focuses on achieving an optimal proportion of debt and equity to optimize financial performance and shareholder value. | Emphasizes the trade-off between the tax shield advantage of debt and the expected costs associated with financial distress. |

| Tax Implications | Incorporates the benefit of debt tax shields as one factor in determining optimal leverage. | Specifically highlights tax shields as a driving factor, where debt provides tax advantages but too much increases bankruptcy risk. |

| Bankruptcy Costs Consideration | Accounts for potential costs related to financial distress when structuring capital. | Explicitly models the expected bankruptcy and agency costs as factors limiting debt levels. |

| Flexibility | Considers dynamic changes in market conditions and firm-specific factors for capital structure decisions. | Generally static in nature, focusing on equilibrium where marginal benefits equal marginal costs of debt. |

| Practical Application | Used by financial managers to determine realistic, company-specific debt-equity ratios. | Serves as a theoretical benchmark guiding the balance between debt benefits and risks. |

| Criticism | May be difficult to pinpoint a single optimal structure due to market fluctuations and informational asymmetries. | Assumes clear trade-offs and ignores other factors like market timing and behavioral influences. |

Leverage Optimization

Leverage optimization in finance involves balancing debt and equity to maximize a company's return on investment while minimizing the cost of capital. Companies analyze various financial ratios, such as debt-to-equity and interest coverage ratios, to determine the ideal leverage level that supports growth without increasing financial risk. Optimal leverage strategies improve shareholder value by enhancing earnings per share and maintaining sufficient liquidity to meet obligations. Advanced financial models and market data assist in continuously adjusting leverage to respond to economic conditions and interest rate changes.

Debt-Equity Ratio

The debt-equity ratio measures a company's financial leverage by comparing total liabilities to shareholders' equity, indicating the proportion of debt used to finance assets. In 2023, an ideal debt-equity ratio typically ranges from 1 to 1.5, varying by industry standards, with higher ratios signaling increased risk for investors and creditors. Companies in capital-intensive sectors like utilities often show higher ratios, while technology firms tend to maintain lower debt levels to preserve flexibility. Monitoring this ratio aids stakeholders in assessing a firm's solvency, financial stability, and ability to meet long-term obligations.

Tax Shield Utilization

Tax shield utilization in finance refers to the strategic use of deductible expenses such as interest payments on debt to reduce taxable income and lower overall tax liability. Companies leverage debt financing to maximize interest tax shields, improving cash flow and increasing firm value. Effective tax shield utilization depends on factors like corporate tax rates, capital structure, and the cost of debt. Proper management of tax shields can enhance financial performance and optimize the weighted average cost of capital (WACC).

Bankruptcy Costs

Bankruptcy costs refer to the direct and indirect expenses incurred when a firm faces financial distress leading to insolvency or reorganization. These costs include legal fees, administrative expenses, and losses from operational disruptions, often reducing the overall value of the distressed company. Empirical studies in corporate finance show that bankruptcy costs can significantly impact capital structure decisions, as firms weigh the benefits of debt financing against the risks of financial distress. Understanding the magnitude of these costs is crucial for optimizing leverage ratios and minimizing agency problems between debt holders and equity investors.

Dynamic Adjustment

Dynamic adjustment in finance refers to the continuous modification of portfolio allocations or financial strategies in response to changing market conditions and risk exposures. This approach leverages real-time data, quantitative models, and algorithmic trading to optimize asset performance and minimize losses. Hedge funds and asset managers employ dynamic adjustment techniques such as risk parity, volatility targeting, and tactical asset allocation to enhance returns. Effective dynamic adjustment improves portfolio resilience during market volatility and economic shifts.

Source and External Links

Theories of Capital Structure II - Static Trade-off Theory - This theory posits that an optimal capital structure exists by balancing the tax shield benefits and the costs of financial distress.

Trade-Off Theory of Capital Structure - The trade-off theory suggests that the optimal capital structure is achieved by balancing the tax benefits of debt against the risks of financial distress.

Static Trade-off Theory - This theory explains a company's optimal capital structure by weighing the benefits of increased tax shields against the rising costs of financial distress.

FAQs

What is capital structure?

Capital structure is the mix of debt and equity that a company uses to finance its operations and growth.

What defines optimal capital structure?

Optimal capital structure is defined by the mix of debt and equity that minimizes a company's overall cost of capital while maximizing its market value and financial flexibility.

What is the static trade-off theory?

The static trade-off theory explains that firms balance the tax benefits of debt with the bankruptcy costs to determine an optimal capital structure.

How does optimal capital structure differ from the static trade-off theory?

Optimal capital structure balances tax benefits of debt with bankruptcy costs, while the static trade-off theory specifically models this balance by weighing the marginal tax shield of debt against expected bankruptcy costs to identify the debt level maximizing firm value.

What factors influence a firm's optimal capital structure?

A firm's optimal capital structure is influenced by factors such as business risk, tax considerations, financial flexibility, management style, market conditions, asset structure, growth opportunities, and agency costs.

What are the main assumptions of the static trade-off theory?

The static trade-off theory assumes firms balance the tax advantages of debt financing against bankruptcy costs, maintain an optimal capital structure by adjusting debt levels to minimize the weighted average cost of capital, and that market imperfections like taxes and financial distress risks influence financing decisions.

Why is understanding capital structure important for financial management?

Understanding capital structure is important for financial management because it directly influences a company's risk profile, cost of capital, and overall financial stability, enabling optimal financing decisions and maximizing shareholder value.