The bid-ask spread represents the price difference between the highest buying offer and the lowest selling offer in a market, directly impacting transaction costs for traders. Market depth measures the volume of buy and sell orders at different price levels, reflecting the supply and demand dynamics influencing liquidity and price stability. Explore how these critical market indicators shape trading strategies and investment decisions in financial markets.

Main Difference

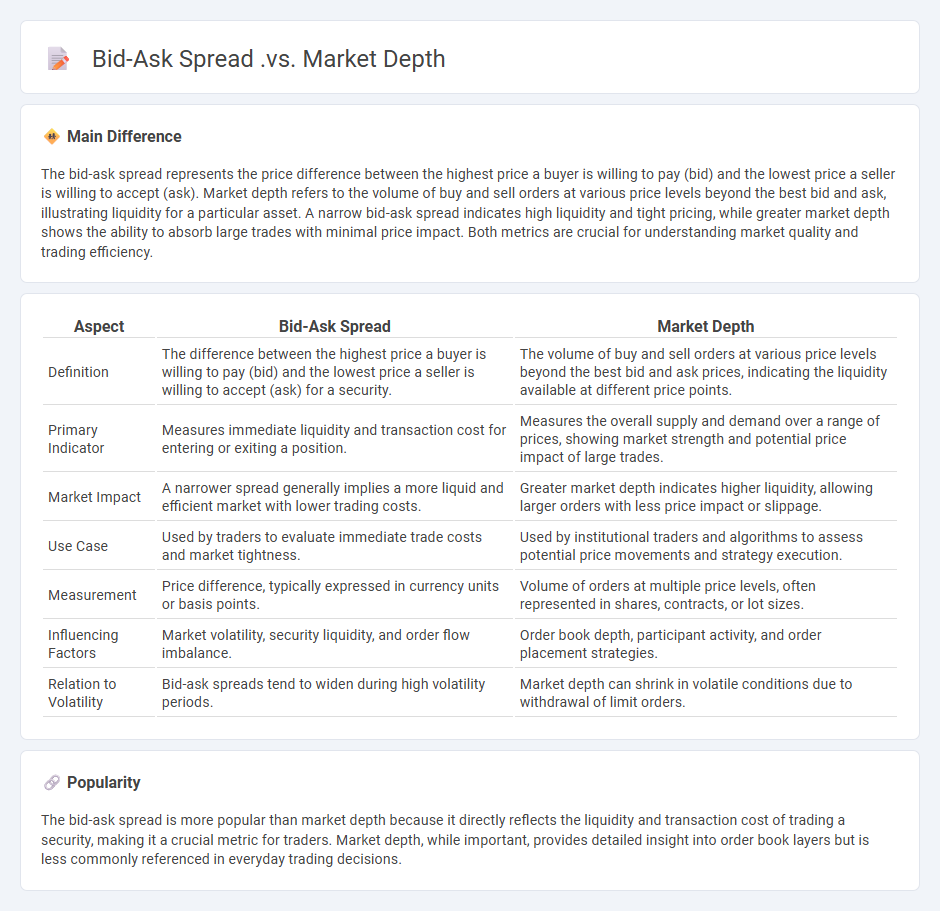

The bid-ask spread represents the price difference between the highest price a buyer is willing to pay (bid) and the lowest price a seller is willing to accept (ask). Market depth refers to the volume of buy and sell orders at various price levels beyond the best bid and ask, illustrating liquidity for a particular asset. A narrow bid-ask spread indicates high liquidity and tight pricing, while greater market depth shows the ability to absorb large trades with minimal price impact. Both metrics are crucial for understanding market quality and trading efficiency.

Connection

Bid-ask spread and market depth are closely intertwined indicators of liquidity in financial markets. A narrower bid-ask spread generally signifies higher market depth, meaning numerous buy and sell orders exist at various price levels, enhancing trade execution efficiency. Conversely, shallow market depth often results in wider bid-ask spreads, reflecting lower liquidity and increased transaction costs.

Comparison Table

| Aspect | Bid-Ask Spread | Market Depth |

|---|---|---|

| Definition | The difference between the highest price a buyer is willing to pay (bid) and the lowest price a seller is willing to accept (ask) for a security. | The volume of buy and sell orders at various price levels beyond the best bid and ask prices, indicating the liquidity available at different price points. |

| Primary Indicator | Measures immediate liquidity and transaction cost for entering or exiting a position. | Measures the overall supply and demand over a range of prices, showing market strength and potential price impact of large trades. |

| Market Impact | A narrower spread generally implies a more liquid and efficient market with lower trading costs. | Greater market depth indicates higher liquidity, allowing larger orders with less price impact or slippage. |

| Use Case | Used by traders to evaluate immediate trade costs and market tightness. | Used by institutional traders and algorithms to assess potential price movements and strategy execution. |

| Measurement | Price difference, typically expressed in currency units or basis points. | Volume of orders at multiple price levels, often represented in shares, contracts, or lot sizes. |

| Influencing Factors | Market volatility, security liquidity, and order flow imbalance. | Order book depth, participant activity, and order placement strategies. |

| Relation to Volatility | Bid-ask spreads tend to widen during high volatility periods. | Market depth can shrink in volatile conditions due to withdrawal of limit orders. |

Liquidity

Liquidity in finance refers to the ease with which an asset can be quickly converted into cash without significantly affecting its market price. Cash is the most liquid asset, while real estate and collectibles are typically less liquid due to longer selling times and transaction costs. High liquidity enables firms and investors to meet short-term obligations and capitalize on investment opportunities. Markets like foreign exchange (forex) and large stock exchanges exhibit high liquidity with substantial trading volumes and tight bid-ask spreads.

Price Volatility

Price volatility in finance refers to the degree of variation in the price of a financial asset over a specific period. It is typically measured using statistical metrics such as standard deviation or variance of asset returns. High volatility indicates larger price swings, implying higher investment risk and potential for profit or loss. Volatility is a critical factor in option pricing models like Black-Scholes and is influenced by market events, liquidity, and investor sentiment.

Order Book

An order book in finance is a real-time, electronic list of buy and sell orders for a specific security or financial instrument, organized by price level. It provides transparency into market liquidity and depth by showing quantities of bids (buy orders) and asks (sell orders) at various prices. Traders and algorithms use the order book to gauge supply and demand dynamics, identify price trends, and execute trades effectively. Major exchanges like NASDAQ and NYSE rely on order books to facilitate orderly market transactions and price discovery.

Transaction Costs

Transaction costs in finance refer to the expenses incurred when buying or selling assets, including broker fees, bid-ask spreads, taxes, and slippage. These costs directly impact market efficiency by influencing trading frequency and liquidity, often reducing overall investment returns. High transaction costs can deter market participation and affect asset pricing by increasing the cost basis for investors. Understanding transaction costs is critical for portfolio management, risk assessment, and optimizing trading strategies.

Slippage

Slippage in finance refers to the difference between the expected price of a trade and the actual price at which the trade is executed. It commonly occurs in volatile markets or during periods of low liquidity, impacting forex, stocks, and cryptocurrency trading. Institutional traders often experience slippage during large orders, as market orders get filled incrementally at varying prices. Minimizing slippage involves using limit orders or algorithms designed to execute trades at desired price points.

Source and External Links

Market Depth an In-depth Look | Trade for Good - The bid-ask spread is the difference between the best available buy (bid) and sell (ask) prices, while market depth refers to the number of orders at various price levels that indicate liquidity and how much the market can absorb large orders without significant price impact.

Understanding Bid-Ask Spread: The Hidden Cost Every Trader Pays - The bid-ask spread represents the cost traders pay due to the difference between buying and selling prices, and its width reflects liquidity; tighter spreads occur in more liquid markets, whereas wider spreads indicate lower liquidity.

2025 Trader's Guide to Market Depth - The Trading Analyst - Market depth is influenced by factors such as tick size, margin requirements, trading restrictions, volatility, and market sentiment, all of which affect liquidity and the spread between bid and ask prices.

FAQs

What is a bid-ask spread?

A bid-ask spread is the difference between the highest price a buyer is willing to pay (bid) and the lowest price a seller is willing to accept (ask) for a security or asset in the market.

What does market depth mean?

Market depth refers to the measure of supply and demand for a financial asset at different price levels, showing the quantity of buy and sell orders in the order book.

How is the bid-ask spread different from market depth?

The bid-ask spread represents the price difference between the highest bid and lowest ask in the market, while market depth measures the volume of buy and sell orders available at various price levels beyond the best bid and ask.

Why is a tight bid-ask spread important?

A tight bid-ask spread is important because it reduces trading costs, increases market liquidity, and reflects accurate asset pricing.

How does market depth affect trading decisions?

Market depth reveals the volume of buy and sell orders at various price levels, enabling traders to assess liquidity, predict price movements, and make informed decisions on order timing and size to minimize slippage and optimize trade execution.

What factors influence the bid-ask spread?

Bid-ask spread is influenced by market liquidity, trading volume, asset volatility, market maker competition, time of day, and transaction costs.

How can traders use market depth information?

Traders use market depth information to assess supply and demand levels, identify support and resistance zones, anticipate price movements, optimize order placement, and improve trade execution by analyzing the volume and price of pending buy and sell orders.