LIBOR (London Interbank Offered Rate) has been a key benchmark interest rate used globally for pricing loans and derivatives, but its credibility has declined due to manipulation scandals and a lack of underlying transaction data. SOFR (Secured Overnight Financing Rate) is now the preferred alternative, based on overnight U.S. Treasury repurchase agreement transactions, providing a more transparent and reliable benchmark. Explore detailed comparisons between LIBOR and SOFR to understand their impact on financial markets.

Main Difference

LIBOR (London Interbank Offered Rate) reflects the average interest rate at which major global banks lend to one another in the London interbank market. SOFR (Secured Overnight Financing Rate) measures the cost of borrowing cash overnight collateralized by U.S. Treasury securities in the repurchase agreement (repo) market. LIBOR is based on subjective expert estimates, making it prone to manipulation, whereas SOFR is transaction-based, offering a more transparent and reliable benchmark. The transition from LIBOR to SOFR addresses regulatory concerns and aims to enhance the integrity of interest rate references in financial markets.

Connection

LIBOR (London Interbank Offered Rate) and SOFR (Secured Overnight Financing Rate) are key benchmark interest rates used in global financial markets to set borrowing costs and price various financial products. SOFR is considered a more robust and transparent alternative to LIBOR, reflecting rates on overnight repurchase agreements secured by U.S. Treasury securities. The transition from LIBOR to SOFR aims to enhance market stability by replacing LIBOR's reliance on expert judgment with SOFR's transaction-based data.

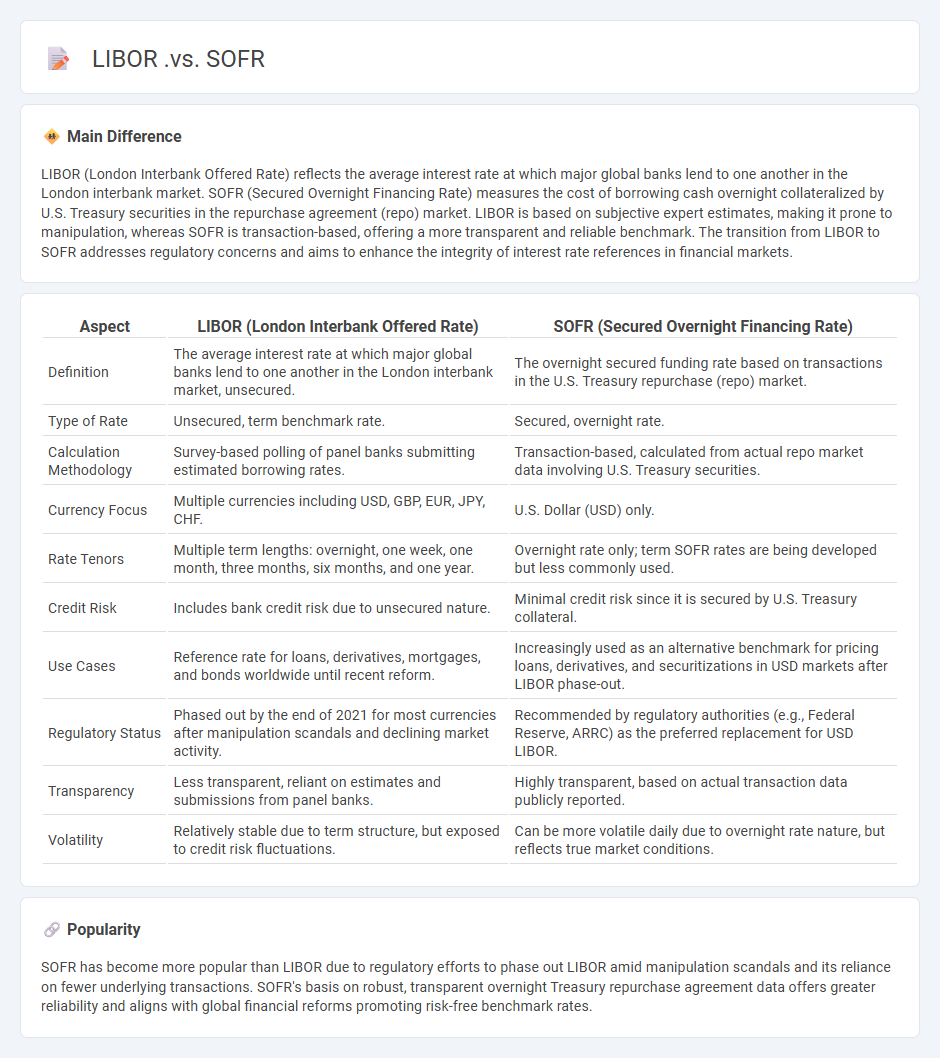

Comparison Table

| Aspect | LIBOR (London Interbank Offered Rate) | SOFR (Secured Overnight Financing Rate) |

|---|---|---|

| Definition | The average interest rate at which major global banks lend to one another in the London interbank market, unsecured. | The overnight secured funding rate based on transactions in the U.S. Treasury repurchase (repo) market. |

| Type of Rate | Unsecured, term benchmark rate. | Secured, overnight rate. |

| Calculation Methodology | Survey-based polling of panel banks submitting estimated borrowing rates. | Transaction-based, calculated from actual repo market data involving U.S. Treasury securities. |

| Currency Focus | Multiple currencies including USD, GBP, EUR, JPY, CHF. | U.S. Dollar (USD) only. |

| Rate Tenors | Multiple term lengths: overnight, one week, one month, three months, six months, and one year. | Overnight rate only; term SOFR rates are being developed but less commonly used. |

| Credit Risk | Includes bank credit risk due to unsecured nature. | Minimal credit risk since it is secured by U.S. Treasury collateral. |

| Use Cases | Reference rate for loans, derivatives, mortgages, and bonds worldwide until recent reform. | Increasingly used as an alternative benchmark for pricing loans, derivatives, and securitizations in USD markets after LIBOR phase-out. |

| Regulatory Status | Phased out by the end of 2021 for most currencies after manipulation scandals and declining market activity. | Recommended by regulatory authorities (e.g., Federal Reserve, ARRC) as the preferred replacement for USD LIBOR. |

| Transparency | Less transparent, reliant on estimates and submissions from panel banks. | Highly transparent, based on actual transaction data publicly reported. |

| Volatility | Relatively stable due to term structure, but exposed to credit risk fluctuations. | Can be more volatile daily due to overnight rate nature, but reflects true market conditions. |

Benchmark Rate

The benchmark rate in finance serves as a standard interest rate used to price loans, bonds, and other financial instruments. Common examples include the U.S. Federal Reserve's federal funds rate, the London Interbank Offered Rate (LIBOR), and the Secured Overnight Financing Rate (SOFR). These benchmark rates influence borrowing costs, monetary policy decisions, and financial market stability worldwide. Accurate tracking of benchmark rates is essential for risk management and investment strategies across banking and corporate sectors.

Credit Risk Premium

Credit risk premium represents the additional yield that investors require to compensate for the risk of borrower default compared to risk-free securities like U.S. Treasury bonds. This premium varies based on the borrower's creditworthiness, economic conditions, and market liquidity, often measured using credit spreads on corporate bonds or credit default swap (CDS) prices. Financial institutions analyze credit risk premiums to price loans, bonds, and derivatives accurately while managing portfolio risk. Understanding the credit risk premium is essential for effective risk management and capital allocation in corporate finance and investment management.

Secured vs. Unsecured

Secured loans require collateral, such as property or assets, to back the loan, reducing lender risk and often resulting in lower interest rates. Unsecured loans lack collateral, relying solely on the borrower's creditworthiness, which typically leads to higher interest rates and stricter approval criteria. Examples of secured loans include mortgages and auto loans, while credit cards and personal loans are common unsecured loan types. The choice between secured and unsecured financing depends on factors like credit score, loan amount, and asset availability.

Market Transparency

Market transparency in finance refers to the availability of timely and accurate information about financial instruments, prices, and market activities. High transparency reduces information asymmetry between buyers and sellers, fostering liquidity and efficient price discovery. Regulatory bodies like the SEC and MiFID II enforce disclosure standards to enhance transparency across stock exchanges, bond markets, and derivatives trading platforms. Enhanced transparency supports investor confidence, mitigates systemic risks, and promotes fair competition within global financial markets.

Transition Timeline

The transition timeline in finance refers to the structured schedule by which financial institutions and markets adapt to evolving regulations, technologies, or economic frameworks. Key milestones include Basel III implementation by 2023, widespread adoption of ESG (Environmental, Social, and Governance) reporting standards by 2025, and integration of fintech solutions such as blockchain and AI-driven analytics accelerating between 2024 and 2027. These timelines enable risk mitigation, compliance alignment, and enhanced operational efficiency within banking, asset management, and insurance sectors. Monitoring regulatory bodies like the SEC, EBA, and FSB provides critical updates to maintain alignment with global financial transition roadmaps.

Source and External Links

From LIBOR to SOFR - LIBOR (London Interbank Offered Rate) was a survey-based average interest rate at which banks lent to each other, while SOFR (Secured Overnight Financing Rate) is a single overnight rate based on transactions secured by U.S. Treasury securities, replacing LIBOR as the main benchmark in mid-2023 due to LIBOR's declining representativeness and manipulation concerns.

Goodbye LIBOR, hello SOFR--what this means for you - Historically, the 1-month SOFR has averaged about 11.45 basis points lower than 1-month LIBOR, with both rates tracking closely during periods of monetary stimulus but often diverging during times of market stress, necessitating spread adjustments in contracts transitioning from LIBOR to SOFR.

LIBOR to SOFR Transition - SOFR is a transparent, transaction-based overnight rate backed by nearly $1 trillion in daily repo market activity, unlike LIBOR, which relied on estimates from a panel of banks, making SOFR less susceptible to manipulation and more reflective of actual borrowing costs in the U.S. dollar market.

FAQs

What is LIBOR?

LIBOR is the London Interbank Offered Rate, a benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans.

What is SOFR?

SOFR (Secured Overnight Financing Rate) is a benchmark interest rate reflecting the cost of borrowing cash overnight collateralized by U.S. Treasury securities.

How is LIBOR calculated?

LIBOR is calculated by collecting borrowing rate submissions from a panel of major global banks, removing the highest and lowest quartiles, and averaging the remaining rates for different currencies and maturities.

How is SOFR calculated?

SOFR is calculated as the volume-weighted median of transaction-level repo rates on overnight Treasury repurchase agreements cleared through the Fixed Income Clearing Corporation (FICC).

What are the main differences between LIBOR and SOFR?

LIBOR is based on estimated unsecured interbank lending rates and includes credit risk and term premiums, while SOFR is a secured overnight rate based on actual Treasury repo transactions, reflecting minimal credit risk and no term premium.

Why is LIBOR being replaced by SOFR?

LIBOR is being replaced by SOFR due to LIBOR's susceptibility to manipulation, declining transaction volumes in its underlying markets, and SOFR's basis on a robust, transparent overnight Treasury repurchase agreement market.

How does the transition from LIBOR to SOFR affect borrowers and lenders?

The transition from LIBOR to SOFR impacts borrowers by changing interest rate benchmarks to a nearly risk-free overnight rate, potentially lowering borrowing costs but increasing rate volatility due to SOFR's secured nature, while lenders face challenges in adjusting contract terms, managing basis risk, and updating risk models to reflect SOFR's transaction-based rates.