Mark-to-market accounting reflects the current market value of assets and liabilities, providing real-time financial information. Historical cost accounting records assets and liabilities at their original purchase price, offering stability but less responsiveness to market fluctuations. Explore the differences and implications of these valuation methods to enhance your understanding of financial reporting.

Main Difference

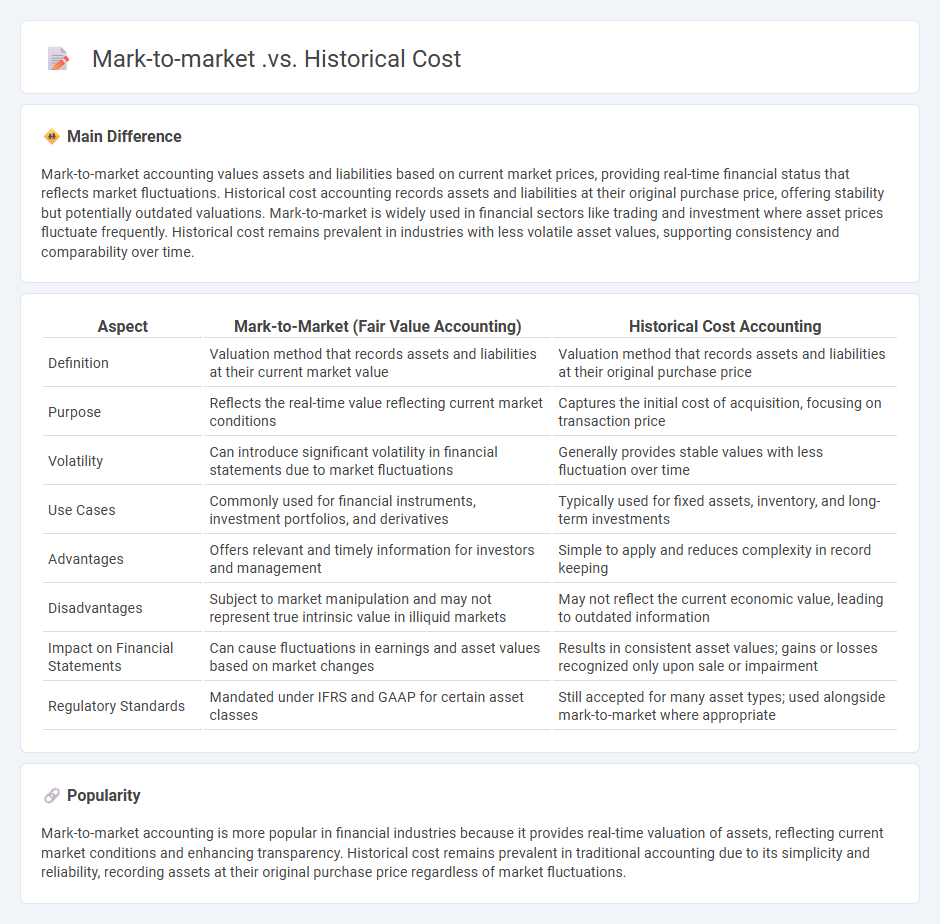

Mark-to-market accounting values assets and liabilities based on current market prices, providing real-time financial status that reflects market fluctuations. Historical cost accounting records assets and liabilities at their original purchase price, offering stability but potentially outdated valuations. Mark-to-market is widely used in financial sectors like trading and investment where asset prices fluctuate frequently. Historical cost remains prevalent in industries with less volatile asset values, supporting consistency and comparability over time.

Connection

Mark-to-market and historical cost accounting both measure asset values but differ in valuation basis; mark-to-market reflects current market prices, providing timely financial insights, while historical cost records assets at original purchase price. This connection impacts financial reporting accuracy, risk assessment, and investment decisions by balancing real-time market fluctuations against stable, historical data. Understanding their interplay is crucial for analysts evaluating asset performance and company financial health under varying market conditions.

Comparison Table

| Aspect | Mark-to-Market (Fair Value Accounting) | Historical Cost Accounting |

|---|---|---|

| Definition | Valuation method that records assets and liabilities at their current market value | Valuation method that records assets and liabilities at their original purchase price |

| Purpose | Reflects the real-time value reflecting current market conditions | Captures the initial cost of acquisition, focusing on transaction price |

| Volatility | Can introduce significant volatility in financial statements due to market fluctuations | Generally provides stable values with less fluctuation over time |

| Use Cases | Commonly used for financial instruments, investment portfolios, and derivatives | Typically used for fixed assets, inventory, and long-term investments |

| Advantages | Offers relevant and timely information for investors and management | Simple to apply and reduces complexity in record keeping |

| Disadvantages | Subject to market manipulation and may not represent true intrinsic value in illiquid markets | May not reflect the current economic value, leading to outdated information |

| Impact on Financial Statements | Can cause fluctuations in earnings and asset values based on market changes | Results in consistent asset values; gains or losses recognized only upon sale or impairment |

| Regulatory Standards | Mandated under IFRS and GAAP for certain asset classes | Still accepted for many asset types; used alongside mark-to-market where appropriate |

Fair Value

Fair value represents the estimated price at which an asset or liability can be exchanged between knowledgeable, willing parties in an arm's length transaction. It reflects market conditions as of the measurement date, incorporating factors such as current market trends, supply and demand, and the intrinsic value of the asset. Accounting standards like IFRS 13 and ASC 820 provide guidelines for determining fair value, ensuring consistency and transparency in financial reporting. Fair value measurement is essential for accurate asset valuation, investment analysis, and risk management in finance.

Book Value

Book value represents the net asset value of a company calculated by subtracting total liabilities from total assets, as reported on the balance sheet. It reflects the historical cost of assets minus accumulated depreciation and amortization, providing a conservative estimate of a company's intrinsic worth. Investors use book value to assess whether a stock is undervalued or overvalued by comparing it with the market value. This metric is crucial in fundamental analysis and valuation models like the price-to-book (P/B) ratio.

Asset Valuation

Asset valuation determines the current worth of tangible and intangible assets using methods like discounted cash flow (DCF), comparable company analysis, and market value assessments. Accurate valuation incorporates factors such as market conditions, asset liquidity, future income potential, and risk profiles. Financial institutions, investors, and corporate entities rely on valuation to make informed decisions regarding mergers, acquisitions, and investment portfolios. Regulatory frameworks and accounting standards, including IFRS and GAAP, guide consistent and transparent valuation practices.

Financial Reporting

Financial reporting involves the preparation and presentation of financial statements, including the balance sheet, income statement, and cash flow statement, to provide stakeholders with accurate insights into a company's financial health. It adheres to established accounting standards such as IFRS or GAAP, ensuring consistency and comparability across reporting periods. Key metrics like revenue, net income, earnings per share, and liquidity ratios are essential for evaluating business performance and investment decisions. Timely and transparent financial reporting supports regulatory compliance and fosters investor confidence in capital markets.

Income Statement Impact

An income statement impact in finance refers to how various financial transactions affect a company's profitability during a specific accounting period. Revenue recognition, expense recording, and cost of goods sold directly influence the net income reported on the income statement. Changes in depreciation, interest expenses, and tax provisions also significantly alter the financial performance metrics. Accurate income statement impact analysis enables stakeholders to assess operational efficiency and make informed strategic decisions.

Source and External Links

## Set 1What Is Mark-To-Market Accounting And Historical Cost Accounting And Their Differences - This webpage discusses the differences between mark-to-market and historical cost accounting, highlighting their uses and impacts on financial statements.

## Set 2Historical Cost Principle: How It Works & Why It Matters - This article explains how historical cost accounting is used for fixed assets, contrasting it with mark-to-market accounting used for liquid assets.

## Set 3What is Mark to Market (MTM) & How it Works? - This blog post describes mark-to-market accounting, its differences with historical cost accounting, and its applications in financial markets.

FAQs

What is mark-to-market accounting?

Mark-to-market accounting measures assets and liabilities at their current market value rather than historical cost to provide a realistic appraisal of a company's financial situation.

What is historical cost accounting?

Historical cost accounting records assets and liabilities at their original purchase price, reflecting their actual transaction value rather than current market value.

How does mark-to-market differ from historical cost?

Mark-to-market values assets based on current market prices, reflecting real-time fair value fluctuations, while historical cost records assets at their original purchase price without accounting for market changes.

What are the advantages of mark-to-market accounting?

Mark-to-market accounting provides real-time asset and liability valuation, enhances transparency, improves risk management, and enables more accurate financial reporting aligned with current market conditions.

What are the disadvantages of using historical cost?

Historical cost undervalues assets during inflation, ignores current market conditions, limits relevance for decision-making, and fails to reflect true economic value.

When is mark-to-market accounting required?

Mark-to-market accounting is required for publicly traded companies and financial institutions to value assets and liabilities at their current market price for accurate financial reporting.

How does each method impact financial statements?

The cash method records revenues and expenses only when cash is received or paid, affecting cash flow statements and potentially understating liabilities and receivables on the balance sheet. The accrual method records revenues when earned and expenses when incurred, providing a more accurate reflection of financial position on the income statement and balance sheet by recognizing accounts receivable and payable.