Convertible bonds offer investors the option to convert their debt into a predetermined number of equity shares, providing potential upside through stock price appreciation. Non-convertible bonds, in contrast, provide fixed interest payments without conversion rights, making them a more stable and predictable income source. Explore the key differences to determine which bond type aligns best with your investment strategy.

Main Difference

Convertible bonds offer investors the option to convert the bond into a predetermined number of company shares, blending features of debt and equity. Non-convertible bonds cannot be converted into shares and provide fixed interest payments until maturity. Convertible bonds typically have lower interest rates due to the conversion feature's added value. Non-convertible bonds generally offer higher yields to compensate for the lack of equity conversion opportunities.

Connection

Convertible bonds and non-convertible bonds are connected as two primary types of debt securities issued by corporations to raise capital, differing mainly in their conversion features. Convertible bonds offer investors the option to convert the bond into a predetermined number of the issuing company's equity shares, combining debt and equity characteristics. Non-convertible bonds, on the other hand, provide fixed interest payments without any option to convert into equity, generally carrying higher interest rates due to the absence of conversion rights.

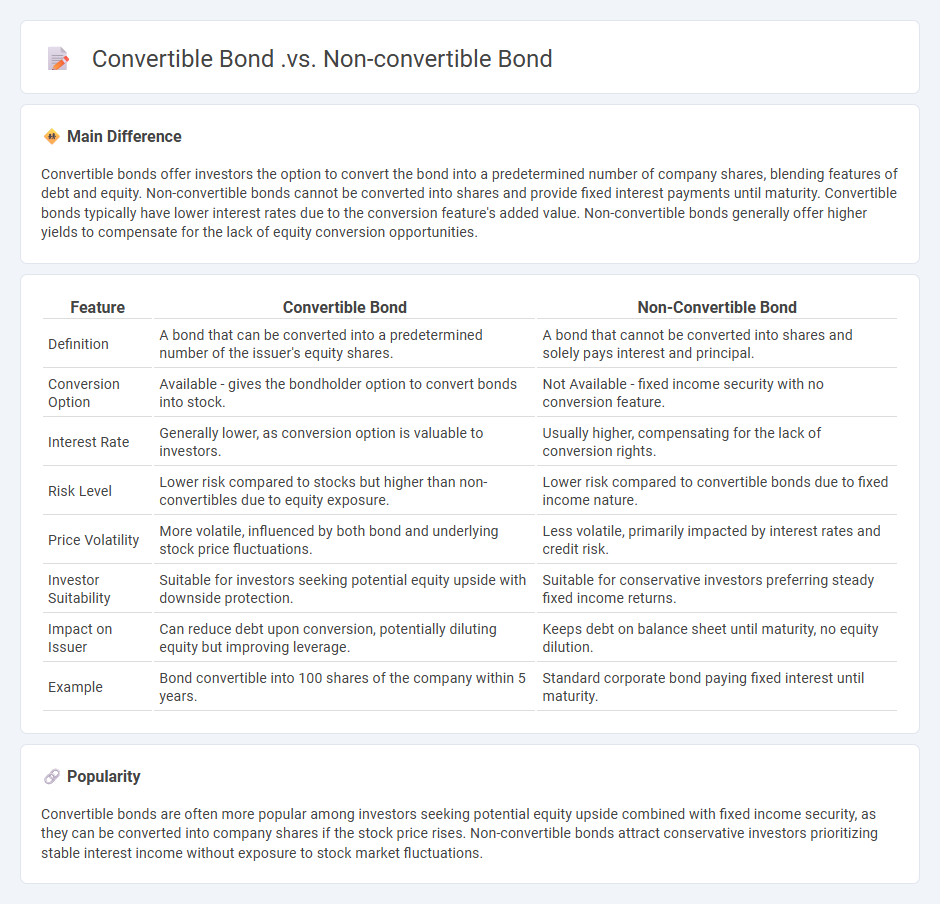

Comparison Table

| Feature | Convertible Bond | Non-Convertible Bond |

|---|---|---|

| Definition | A bond that can be converted into a predetermined number of the issuer's equity shares. | A bond that cannot be converted into shares and solely pays interest and principal. |

| Conversion Option | Available - gives the bondholder option to convert bonds into stock. | Not Available - fixed income security with no conversion feature. |

| Interest Rate | Generally lower, as conversion option is valuable to investors. | Usually higher, compensating for the lack of conversion rights. |

| Risk Level | Lower risk compared to stocks but higher than non-convertibles due to equity exposure. | Lower risk compared to convertible bonds due to fixed income nature. |

| Price Volatility | More volatile, influenced by both bond and underlying stock price fluctuations. | Less volatile, primarily impacted by interest rates and credit risk. |

| Investor Suitability | Suitable for investors seeking potential equity upside with downside protection. | Suitable for conservative investors preferring steady fixed income returns. |

| Impact on Issuer | Can reduce debt upon conversion, potentially diluting equity but improving leverage. | Keeps debt on balance sheet until maturity, no equity dilution. |

| Example | Bond convertible into 100 shares of the company within 5 years. | Standard corporate bond paying fixed interest until maturity. |

Conversion Feature

The conversion feature in finance refers to the option embedded in convertible securities, such as bonds or preferred stocks, allowing holders to exchange them for a predetermined number of common shares. This feature provides investors with potential upside participation in the issuing company's stock price appreciation while receiving fixed income until conversion. Convertible bonds often offer lower interest rates compared to non-convertible bonds, reflecting the value of the conversion option. Companies use these instruments to raise capital at a lower cost, balancing debt financing with equity dilution potential.

Maturity

Maturity in finance refers to the date on which a debt instrument, such as a bond or loan, becomes due for repayment of the principal amount. At maturity, the issuer is obligated to pay back the principal to the investor along with any remaining interest. Different financial instruments have varying maturity periods, ranging from short-term (less than one year) to long-term (over ten years). Understanding maturity helps investors manage interest rate risk and liquidity needs effectively.

Interest Rate

Interest rate represents the cost of borrowing money or the return on investment for lending funds, expressed as a percentage of the principal over a specific period. Central banks, such as the Federal Reserve in the United States, manipulate interest rates to influence economic activity, inflation, and unemployment. Fixed interest rates remain constant throughout the loan term, whereas variable interest rates fluctuate based on market conditions or benchmark rates like LIBOR or the federal funds rate. Understanding the impact of interest rates is crucial for managing mortgages, bonds, credit cards, and savings accounts effectively.

Risk Profile

A risk profile in finance categorizes an investor's willingness and ability to take financial risks based on factors like age, income, investment goals, and time horizon. It helps determine the appropriate asset allocation, balancing risk and potential returns by identifying whether the investor is conservative, moderate, or aggressive. Financial advisors use risk profiles to recommend suitable investment strategies, such as equities, bonds, or alternative assets, aligning portfolios with individual risk tolerance. Understanding risk profiles reduces susceptibility to market volatility and aids in long-term wealth accumulation.

Investment Flexibility

Investment flexibility refers to the ability of investors to adapt their portfolio allocation in response to changing market conditions, economic trends, and personal financial goals. This concept is crucial in dynamic financial markets, allowing investors to seize opportunities and mitigate risks by reallocating assets among stocks, bonds, real estate, and alternative investments. Investment products like mutual funds, ETFs, and managed accounts often provide varying degrees of flexibility through features like automatic rebalancing and liquidity options. Financial advisors emphasize flexibility to optimize returns while maintaining risk tolerance and achieving long-term wealth preservation.

Source and External Links

Understanding Convertible and Non-Convertible Debt for ... - Convertible bonds offer an option to convert debt into equity, usually with lower interest rates and potential upside, while non-convertible bonds provide fixed income with higher interest and no equity conversion option.

Preferred Stock vs. Convertible Bonds - Convertible bonds combine features of bonds and stock options, offering lower yields than conventional bonds but with equity upside potential and greater price volatility.

5 Things to Know About Convertible Bonds - Convertible bonds pay lower interest than standard corporate bonds but include a conversion option into stock, offering more downside protection than stocks and diversification benefits during rising interest rates.

FAQs

What is a convertible bond?

A convertible bond is a type of debt security that can be converted into a predetermined number of the issuer's common shares, offering investors both fixed income and the potential for equity participation.

What is a non-convertible bond?

A non-convertible bond is a fixed-income security that cannot be converted into a company's equity shares, offering only regular interest payments and principal repayment at maturity.

How do convertible and non-convertible bonds differ?

Convertible bonds can be exchanged for a predetermined number of the issuer's shares, offering potential equity upside, while non-convertible bonds provide fixed interest payments without conversion rights.

What are the benefits of a convertible bond?

Convertible bonds offer investors fixed income with the potential for equity upside by converting bonds into shares, provide companies lower interest rates compared to regular debt, improve balance sheet flexibility, and reduce dilution risk until conversion.

What are the risks of a non-convertible bond?

Non-convertible bonds carry credit risk, interest rate risk, liquidity risk, and reinvestment risk.

When should investors choose a convertible bond?

Investors should choose a convertible bond when they seek the potential for equity upside with downside protection through fixed income.

How does interest payment compare for both types?

Interest payments on fixed-rate loans remain constant throughout the loan term, while interest payments on variable-rate loans fluctuate based on market interest rates.