M1 Money Supply includes the most liquid forms of money such as cash, checking accounts, and other assets easily accessible for spending. M2 Money Supply encompasses M1 plus near-money assets like savings accounts, time deposits, and retail money market funds that represent less immediate liquidity. Explore deeper to understand the impact of these money supply measures on economic policy and financial markets.

Main Difference

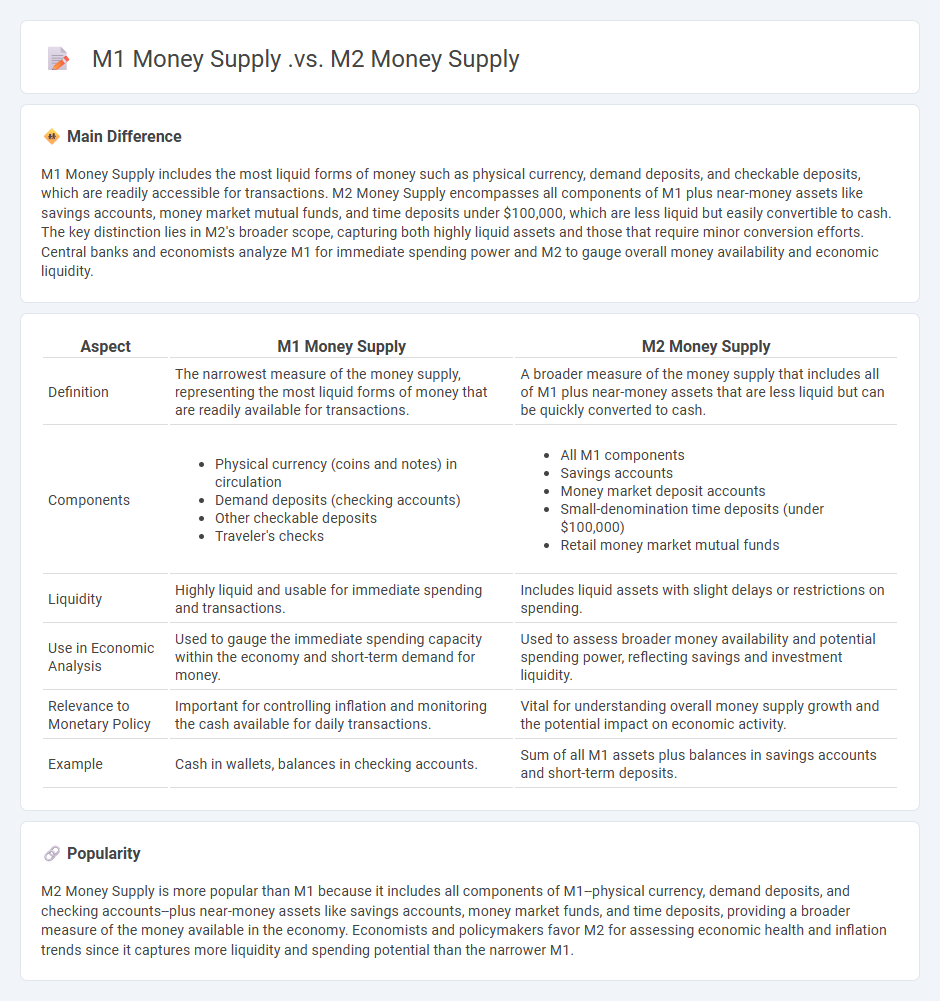

M1 Money Supply includes the most liquid forms of money such as physical currency, demand deposits, and checkable deposits, which are readily accessible for transactions. M2 Money Supply encompasses all components of M1 plus near-money assets like savings accounts, money market mutual funds, and time deposits under $100,000, which are less liquid but easily convertible to cash. The key distinction lies in M2's broader scope, capturing both highly liquid assets and those that require minor conversion efforts. Central banks and economists analyze M1 for immediate spending power and M2 to gauge overall money availability and economic liquidity.

Connection

M1 Money Supply includes the most liquid forms of money such as cash, checking deposits, and other assets that can be quickly converted to currency for transactions. M2 Money Supply encompasses all of M1 along with less liquid assets like savings deposits, time deposits, and retail money market mutual funds, representing a broader measure of the money available in the economy. The connection lies in M1 forming the core liquidity component of M2, linking immediate transaction money with near-money assets that support longer-term economic activities.

Comparison Table

| Aspect | M1 Money Supply | M2 Money Supply |

|---|---|---|

| Definition | The narrowest measure of the money supply, representing the most liquid forms of money that are readily available for transactions. | A broader measure of the money supply that includes all of M1 plus near-money assets that are less liquid but can be quickly converted to cash. |

| Components |

|

|

| Liquidity | Highly liquid and usable for immediate spending and transactions. | Includes liquid assets with slight delays or restrictions on spending. |

| Use in Economic Analysis | Used to gauge the immediate spending capacity within the economy and short-term demand for money. | Used to assess broader money availability and potential spending power, reflecting savings and investment liquidity. |

| Relevance to Monetary Policy | Important for controlling inflation and monitoring the cash available for daily transactions. | Vital for understanding overall money supply growth and the potential impact on economic activity. |

| Example | Cash in wallets, balances in checking accounts. | Sum of all M1 assets plus balances in savings accounts and short-term deposits. |

Currency in Circulation

Currency in circulation refers to the total amount of physical money, such as coins and banknotes, that is actively used by the public for transactions outside the central bank and commercial banking system. As of 2024, the global currency in circulation exceeds $6.5 trillion, reflecting its vital role in daily economic activities and cash-based payments. Central banks monitor currency circulation to manage inflation, liquidity, and overall economic stability. This metric is a key indicator of the health of a nation's monetary system and the public's trust in its currency.

Demand Deposits

Demand deposits represent bank account balances accessible by the account holder at any time without prior notice, typically used for everyday transactions. These deposits form a crucial component of the money supply (M1), including checking accounts, NOW accounts, and share draft accounts. In 2023, U.S. commercial banks held approximately $6.5 trillion in demand deposits, reflecting their importance in liquidity and payment systems. Regulatory frameworks by the Federal Reserve and FDIC ensure the safety and availability of these funds for consumers and businesses.

Savings Accounts

Savings accounts provide a secure way to store funds while earning interest, typically ranging from 0.01% to 4.00% annual percentage yield (APY) depending on the financial institution and account type. These accounts offer easy access to money with minimal risk, making them ideal for emergency funds and short-term savings goals. Federal Deposit Insurance Corporation (FDIC) coverage protects deposits up to $250,000 per depositor, per insured bank. Online banks usually offer higher interest rates compared to traditional brick-and-mortar banks due to lower overhead costs.

Time Deposits

Time deposits, also known as certificates of deposit (CDs), are fixed-term financial instruments offered by banks and credit unions that provide a higher interest rate compared to regular savings accounts. These deposits require the investor to lock in a specific amount of money for a predetermined period, typically ranging from one month to five years, in exchange for guaranteed returns. Interest rates on time deposits vary based on the term length and prevailing market conditions, with longer maturities generally yielding higher rates. Early withdrawal penalties apply if funds are accessed before maturity, making them suitable for conservative investors seeking stable income with low risk.

Liquidity

Liquidity in finance refers to the ease with which an asset can be converted into cash without significantly affecting its market price. Cash is considered the most liquid asset, followed by marketable securities and accounts receivable. High liquidity reduces the risk of financial distress by ensuring that obligations can be met promptly. Companies and investors prioritize liquidity to maintain operational stability and capitalize on short-term opportunities.

Source and External Links

Measuring Money: Currency, M1, and M2 | Macroeconomics - M1 money supply includes currency, checkable deposits, and savings, while M2 includes all of M1 plus time deposits, certificates of deposit, and money market funds, making M2 a broader measure than M1.

27.2 Measuring Money: Currency, M1, and M2 - Principles of Economics - M1 is the most liquid form of money including cash, demand deposits, and traveler's checks, whereas M2 consists of M1 plus less liquid items such as savings and time deposits and money market funds.

Reading: Measuring Money: Currency, M1, and M2 | Macroeconomics - M1 emphasizes very liquid assets like cash and checking accounts, while M2 encompasses M1 plus savings accounts, small time deposits, and retail money market funds, reflecting differing degrees of liquidity.

FAQs

What is money supply?

Money supply is the total amount of currency and liquid assets available in an economy at a specific time, including cash, coins, and balances in checking and savings accounts.

What is included in M1 money supply?

M1 money supply includes physical currency (coins and paper money), demand deposits, traveler's checks, and other checkable deposits held by the public.

What is included in M2 money supply?

M2 money supply includes M1 (currency in circulation and checkable deposits), savings deposits, money market deposit accounts, small-denomination time deposits under $100,000, and retail money market mutual fund balances.

How does M1 differ from M2?

M1 refers to physical currency and demand deposits, while M2 includes all M1 components plus savings deposits, money market accounts, and small time deposits.

What are the main uses of M1 vs. M2?

M1 primarily measures the most liquid forms of money such as cash, checking deposits, and traveler's checks, reflecting immediate spending power; M2 includes all of M1 plus near-money assets like savings deposits, money market securities, and time deposits, indicating broader money supply and potential spending capacity.

Why do central banks measure M1 and M2 separately?

Central banks measure M1 and M2 separately to monitor liquidity levels accurately; M1 includes highly liquid forms like cash and checking deposits, while M2 encompasses M1 plus less liquid assets such as savings deposits and money market funds, enabling precise assessment of money supply and economic activity.

How do changes in M1 and M2 affect the economy?

Increases in M1 boost liquidity and consumer spending, stimulating economic growth, while changes in M2 reflect broader money supply shifts influencing inflation and long-term investment.