Gordon's Growth Model calculates a stock's intrinsic value based on a constant dividend growth rate, emphasizing future dividend payments to equity investors. The Dividend Discount Model (DDM) expands on this by accommodating varying dividend growth phases, offering flexibility for companies with non-constant dividend patterns. Explore the nuances and applications of both models to enhance your investment valuation strategies.

Main Difference

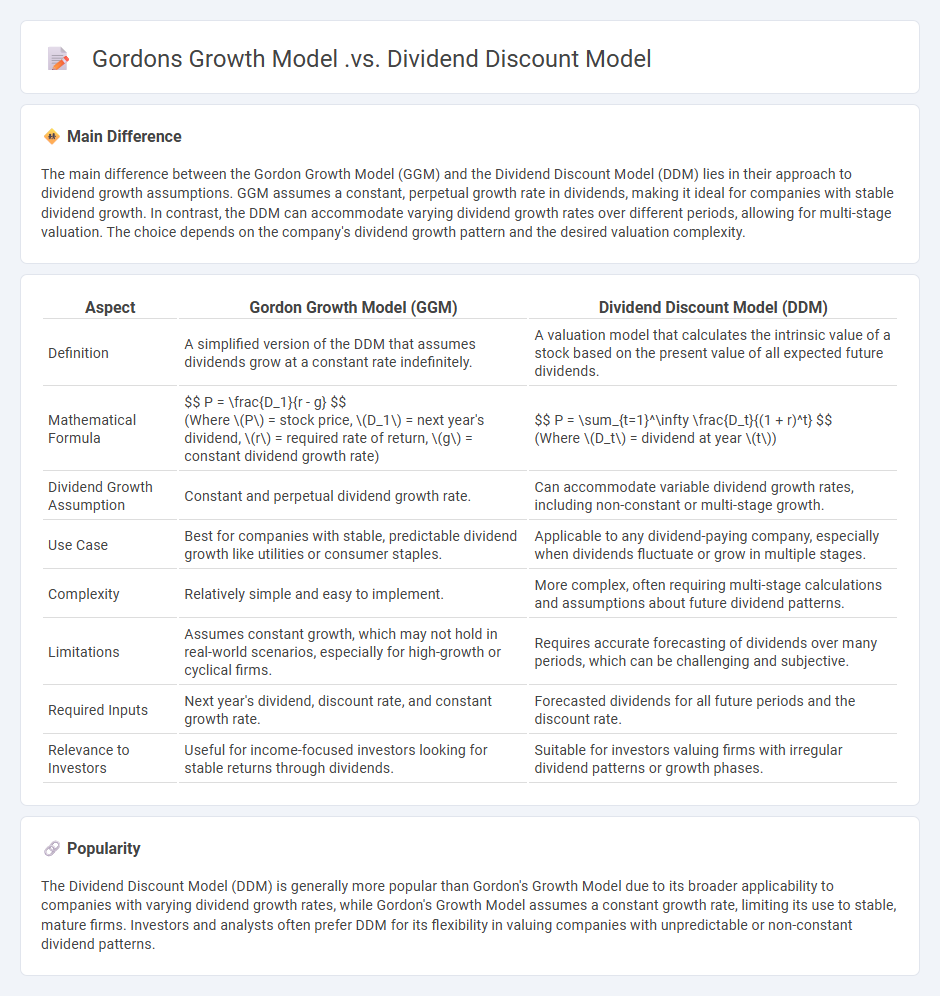

The main difference between the Gordon Growth Model (GGM) and the Dividend Discount Model (DDM) lies in their approach to dividend growth assumptions. GGM assumes a constant, perpetual growth rate in dividends, making it ideal for companies with stable dividend growth. In contrast, the DDM can accommodate varying dividend growth rates over different periods, allowing for multi-stage valuation. The choice depends on the company's dividend growth pattern and the desired valuation complexity.

Connection

Gordon Growth Model (GGM) is a specific form of the Dividend Discount Model (DDM) that assumes a constant dividend growth rate indefinitely. Both models value a stock based on the present value of expected future dividends, but GGM simplifies calculations by incorporating a steady growth rate, expressed as Price = Dividend per share / (Discount rate - Growth rate). This connection enables investors to estimate intrinsic stock value efficiently when dividends follow a predictable growth pattern.

Comparison Table

| Aspect | Gordon Growth Model (GGM) | Dividend Discount Model (DDM) |

|---|---|---|

| Definition | A simplified version of the DDM that assumes dividends grow at a constant rate indefinitely. | A valuation model that calculates the intrinsic value of a stock based on the present value of all expected future dividends. |

| Mathematical Formula | $$ P = \frac{D_1}{r - g} $$ (Where \(P\) = stock price, \(D_1\) = next year's dividend, \(r\) = required rate of return, \(g\) = constant dividend growth rate) |

$$ P = \sum_{t=1}^\infty \frac{D_t}{(1 + r)^t} $$ (Where \(D_t\) = dividend at year \(t\)) |

| Dividend Growth Assumption | Constant and perpetual dividend growth rate. | Can accommodate variable dividend growth rates, including non-constant or multi-stage growth. |

| Use Case | Best for companies with stable, predictable dividend growth like utilities or consumer staples. | Applicable to any dividend-paying company, especially when dividends fluctuate or grow in multiple stages. |

| Complexity | Relatively simple and easy to implement. | More complex, often requiring multi-stage calculations and assumptions about future dividend patterns. |

| Limitations | Assumes constant growth, which may not hold in real-world scenarios, especially for high-growth or cyclical firms. | Requires accurate forecasting of dividends over many periods, which can be challenging and subjective. |

| Required Inputs | Next year's dividend, discount rate, and constant growth rate. | Forecasted dividends for all future periods and the discount rate. |

| Relevance to Investors | Useful for income-focused investors looking for stable returns through dividends. | Suitable for investors valuing firms with irregular dividend patterns or growth phases. |

Constant Growth Assumption

The Constant Growth Assumption is a key concept in finance used to value stocks through the Gordon Growth Model, which assumes dividends increase at a steady, constant rate indefinitely. This model is widely applied for companies with stable earnings and predictable dividend growth, reflecting long-term investor expectations. The formula calculates a stock's intrinsic value by dividing the expected dividend next year by the difference between the required rate of return and the constant growth rate. Financial analysts rely on this assumption to simplify valuation and forecast future cash flows in equity markets.

Valuation Formula

The valuation formula in finance calculates the present value of expected future cash flows to determine an asset's worth. Common methods include discounted cash flow (DCF) analysis, which uses a discount rate to account for time value of money and risk. Market-based valuations use multiples like price-to-earnings (P/E) ratios derived from comparable companies. Accurate application of valuation formulas supports investment decisions, mergers, and financial reporting.

Required Rate of Return

The Required Rate of Return (RRR) represents the minimum annual percentage an investor expects from an investment to compensate for its risk and opportunity cost. Commonly used in finance, RRR guides decisions in capital budgeting, stock valuation, and bond pricing by determining if potential returns justify the investment risk. The Capital Asset Pricing Model (CAPM) often calculates RRR as the risk-free rate plus the asset's beta multiplied by the equity market risk premium. Firms typically set RRR based on their cost of equity or weighted average cost of capital (WACC) to evaluate project feasibility and investor expectations.

Dividend Projection

Dividend projection estimates future dividend payments based on a company's historical payout ratios, earnings growth, and cash flow trends. Analysts use dividend discount models (DDM) to forecast stock value by discounting expected dividends to present value, factoring in company profitability and market conditions. Reliable dividend projections depend on stable earnings, low payout ratio volatility, and effective capital allocation by firms in sectors like utilities and consumer staples. Investors prioritize dividend forecasts to assess income potential and evaluate long-term stock performance stability.

Applicability

Applicability in finance refers to the relevance and suitability of financial models, theories, and tools to real-world scenarios such as investment analysis, risk management, and portfolio optimization. Financial institutions rely on the applicability of quantitative methods like discounted cash flow (DCF) valuation and the Capital Asset Pricing Model (CAPM) to make data-driven decisions. Regulatory frameworks such as Basel III demonstrate applicability by setting capital requirements that ensure banking sector stability. The adoption of blockchain technology illustrates the growing applicability of decentralized finance (DeFi) platforms in enhancing transaction transparency and security.

Source and External Links

Dividend Discount Model - The Dividend Discount Model (DDM) is a valuation method that calculates a stock's intrinsic value by summing future dividend payments, discounted back to their present value.

Gordon Growth Model - The Gordon Growth Model assumes a constant growth rate in dividend payments and estimates stock value by dividing the next year's dividend by the difference between the required rate of return and the growth rate.

Dividend Discount Model vs. Gordon Growth Model - Both models estimate stock intrinsic value, but the Gordon Growth Model simplifies the DDM by assuming a perpetual constant growth rate, making it more suitable for mature companies.

FAQs

What is the Gordon Growth Model?

The Gordon Growth Model calculates a stock's intrinsic value by dividing the expected next dividend by the difference between the discount rate and the dividend growth rate.

What is the Dividend Discount Model?

The Dividend Discount Model (DDM) calculates a stock's intrinsic value by discounting expected future dividends to their present value using a required rate of return.

How does the Gordon Growth Model differ from the Dividend Discount Model?

The Gordon Growth Model is a specific type of Dividend Discount Model that assumes dividends grow at a constant rate indefinitely, while the Dividend Discount Model can accommodate varying dividend growth rates or different dividend patterns.

What are the assumptions of the Gordon Growth Model?

The Gordon Growth Model assumes a constant dividend growth rate, a stable required rate of return greater than the growth rate, perpetual firm life, and dividends growing at a steady, predictable rate indefinitely.

When should you use the Dividend Discount Model over the Gordon Growth Model?

Use the Dividend Discount Model when valuing stocks with variable or unpredictable dividend growth rates; use the Gordon Growth Model specifically for stocks with constant, perpetually growing dividends at a stable rate.

What are the limitations of both models?

Limitations of Model A include high computational cost and limited scalability; Model B suffers from lower accuracy in complex scenarios and longer training times.

How do growth rates affect valuation in each model?

Higher growth rates increase valuation in Discounted Cash Flow (DCF) models by boosting projected cash flows and Terminal Value; in the Gordon Growth Model, valuation rises as the expected growth rate approaches but remains below the discount rate; in comparables multiples, faster growth can justify higher multiples, leading to increased valuation.