Commercial paper refers to short-term unsecured promissory notes issued by corporations to meet immediate financing needs, typically maturing within 270 days. Treasury bills are short-term government securities backed by the U.S. Treasury, known for their low risk and maturities ranging from a few days to one year. Explore the differences in risk, issuance, and returns to understand which suits your investment strategy better.

Main Difference

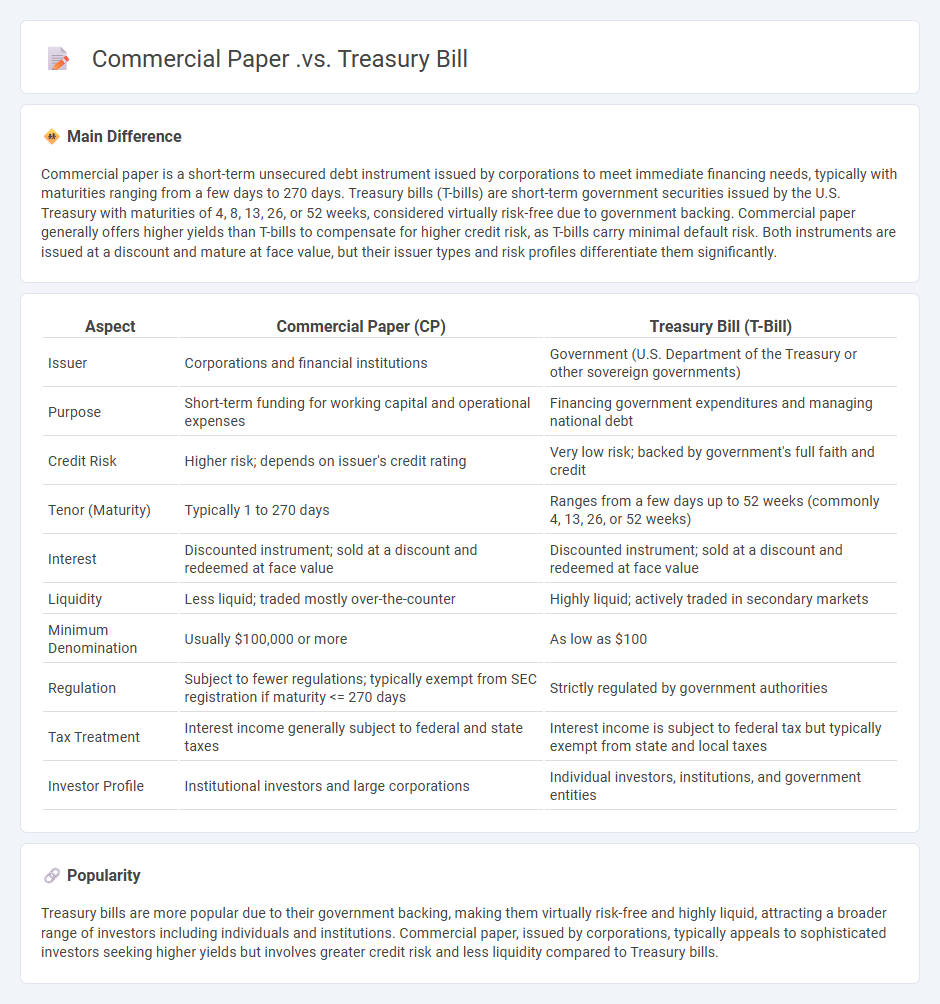

Commercial paper is a short-term unsecured debt instrument issued by corporations to meet immediate financing needs, typically with maturities ranging from a few days to 270 days. Treasury bills (T-bills) are short-term government securities issued by the U.S. Treasury with maturities of 4, 8, 13, 26, or 52 weeks, considered virtually risk-free due to government backing. Commercial paper generally offers higher yields than T-bills to compensate for higher credit risk, as T-bills carry minimal default risk. Both instruments are issued at a discount and mature at face value, but their issuer types and risk profiles differentiate them significantly.

Connection

Commercial paper and Treasury bills are both short-term debt instruments used by corporations and governments respectively to raise funds quickly and efficiently. Treasury bills, issued by the government, are considered low-risk with maturities ranging from a few days to one year, while commercial paper is issued by corporations with maturities typically up to 270 days, offering higher yields due to increased risk. Both instruments play crucial roles in money market operations by providing liquidity and funding for working capital needs.

Comparison Table

| Aspect | Commercial Paper (CP) | Treasury Bill (T-Bill) |

|---|---|---|

| Issuer | Corporations and financial institutions | Government (U.S. Department of the Treasury or other sovereign governments) |

| Purpose | Short-term funding for working capital and operational expenses | Financing government expenditures and managing national debt |

| Credit Risk | Higher risk; depends on issuer's credit rating | Very low risk; backed by government's full faith and credit |

| Tenor (Maturity) | Typically 1 to 270 days | Ranges from a few days up to 52 weeks (commonly 4, 13, 26, or 52 weeks) |

| Interest | Discounted instrument; sold at a discount and redeemed at face value | Discounted instrument; sold at a discount and redeemed at face value |

| Liquidity | Less liquid; traded mostly over-the-counter | Highly liquid; actively traded in secondary markets |

| Minimum Denomination | Usually $100,000 or more | As low as $100 |

| Regulation | Subject to fewer regulations; typically exempt from SEC registration if maturity <= 270 days | Strictly regulated by government authorities |

| Tax Treatment | Interest income generally subject to federal and state taxes | Interest income is subject to federal tax but typically exempt from state and local taxes |

| Investor Profile | Institutional investors and large corporations | Individual investors, institutions, and government entities |

Maturity Period

The maturity period in finance refers to the length of time until a financial instrument, such as a bond or loan, reaches its due date for repayment. It defines when the principal amount must be repaid to the investor or lender. Common maturity periods range from short-term (under one year) to long-term (over ten years), influencing interest rates and investment risk. Understanding the maturity period is crucial for cash flow planning and interest rate risk management in portfolio strategies.

Issuer Type

Issuer type in finance categorizes entities that offer securities to investors, primarily including corporations, governments, and financial institutions. Corporate issuers issue stocks and bonds to raise capital for business operations and expansion. Government issuers release sovereign bonds or treasury bills to finance public projects and manage national debt. Financial institutions, such as banks, may issue debt instruments like certificates of deposit or commercial paper to support liquidity and lending activities.

Risk Level

Risk level in finance measures the potential variability or uncertainty of returns on an investment, reflecting the probability of losing some or all of the original capital. It is quantified using metrics such as standard deviation, beta, and Value at Risk (VaR), which assess the volatility and exposure to market fluctuations. Higher risk levels typically demand greater expected returns to compensate investors for the uncertainty and potential losses. Understanding risk levels is crucial for portfolio management, asset allocation, and aligning investments with an investor's risk tolerance and financial goals.

Liquidity

Liquidity in finance refers to the ease with which an asset can be converted into cash without significantly affecting its market price. High liquidity assets include cash, money market instruments, and publicly traded stocks, as they can be quickly sold with minimal price impact. Companies and investors prioritize liquidity to meet short-term obligations and manage financial stability effectively. Market liquidity also plays a crucial role in determining the efficiency and risk of financial markets.

Interest Rate

Interest rate represents the cost of borrowing money or the return on investment, typically expressed as a percentage annually. Central banks, such as the Federal Reserve, influence interest rates to control inflation and stimulate economic growth. Fixed and variable interest rates impact loans like mortgages, credit cards, and bonds differently, affecting personal and corporate finance decisions. Understanding the prime rate, LIBOR, and yield curves is essential for analyzing market trends and investment opportunities.

Source and External Links

Here are three sets of answers comparing commercial paper and Treasury bills:Commercial Paper Definition - Commercial paper is issued by corporations with strong credit, offering slightly higher yields than Treasury bills due to higher default risk and lower liquidity.

Application - Treasury Bills and Commercial Papers - Commercial papers are issued by large corporations as an alternative to bank loans, offering terms less than 270 days and yields higher than T-bills due to higher default risk.

Differences Between Commercial Paper And Treasury Bill - Commercial papers have a higher likelihood of default compared to Treasury bills, which are issued by governments and generally considered safer investments.

FAQs

What is commercial paper?

Commercial paper is an unsecured, short-term debt instrument issued by corporations to finance payroll, accounts payable, and inventories, typically maturing within 270 days.

What is a treasury bill?

A treasury bill is a short-term government debt security with maturities ranging from a few days to one year, issued at a discount and redeemed at face value.

What is the difference between commercial paper and treasury bill?

Commercial paper is an unsecured short-term debt instrument issued by corporations to finance working capital, typically with maturities up to 270 days, while treasury bills are short-term government securities issued by the U.S. Treasury with maturities of 4, 13, 26, or 52 weeks, considered virtually risk-free.

Who issues commercial paper and treasury bills?

Corporations and financial institutions issue commercial paper, while governments issue treasury bills.

What is the maturity period of commercial paper vs treasury bill?

The maturity period of commercial paper ranges from 1 to 270 days, while treasury bills have maturities of 91, 182, or 364 days.

Are commercial papers riskier than treasury bills?

Commercial papers generally carry higher credit risk than Treasury bills because they are unsecured corporate short-term debt, whereas Treasury bills are government-backed and considered virtually risk-free.

How are commercial papers and treasury bills used in the financial market?

Commercial papers provide short-term unsecured funding for corporations, while treasury bills serve as low-risk government debt instruments for managing liquidity and financing public expenditures.