Chief Legal Officers (CLOs) and Chief Data Officers (CDOs) hold distinct roles within organizations, focusing respectively on legal compliance and data management. CLOs ensure adherence to laws and regulations while mitigating legal risks, whereas CDOs oversee data strategy, governance, and analytics to drive business value. Explore deeper insights into how these C-suite positions impact corporate strategy and operational efficiency.

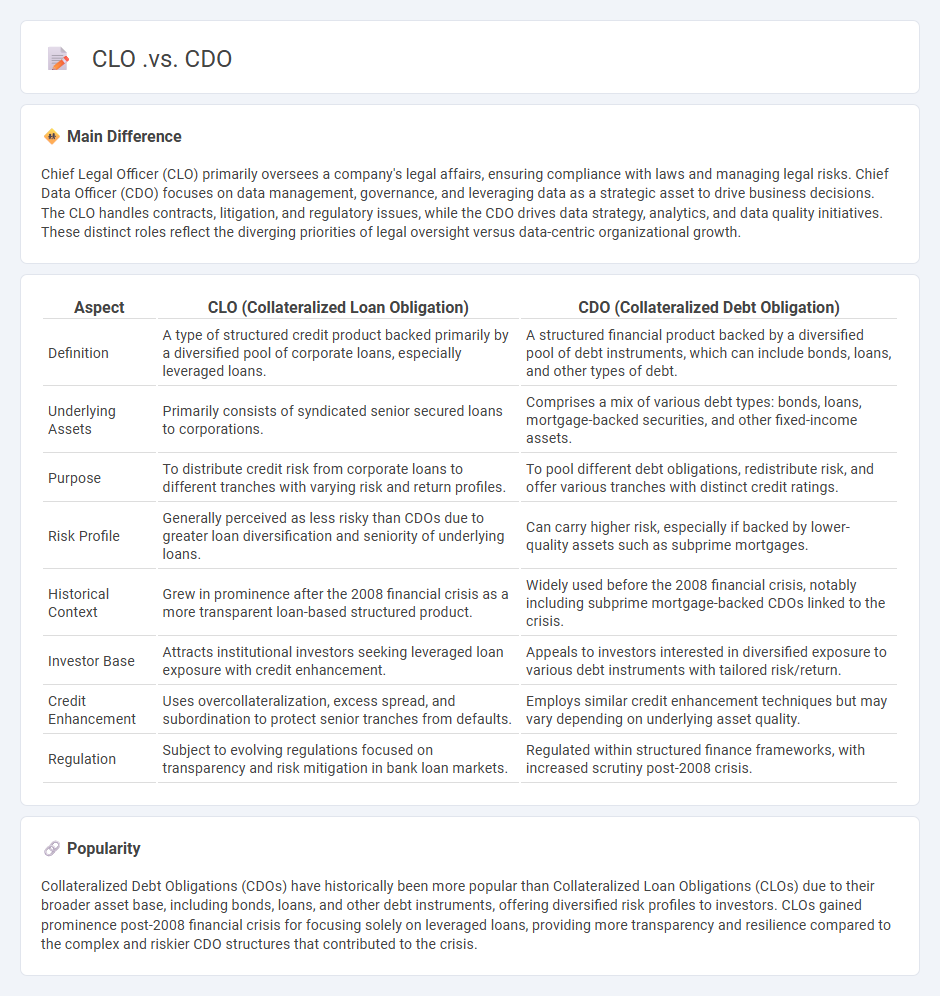

Main Difference

Chief Legal Officer (CLO) primarily oversees a company's legal affairs, ensuring compliance with laws and managing legal risks. Chief Data Officer (CDO) focuses on data management, governance, and leveraging data as a strategic asset to drive business decisions. The CLO handles contracts, litigation, and regulatory issues, while the CDO drives data strategy, analytics, and data quality initiatives. These distinct roles reflect the diverging priorities of legal oversight versus data-centric organizational growth.

Connection

Chief Legal Officers (CLOs) and Chief Data Officers (CDOs) collaborate strategically to ensure data governance complies with legal standards and regulatory requirements. CLOs provide guidance on data privacy laws, risk management, and intellectual property rights, which informs the CDO's data strategy and compliance frameworks. This connection enhances organizational data integrity, security, and ethical use of information assets.

Comparison Table

| Aspect | CLO (Collateralized Loan Obligation) | CDO (Collateralized Debt Obligation) |

|---|---|---|

| Definition | A type of structured credit product backed primarily by a diversified pool of corporate loans, especially leveraged loans. | A structured financial product backed by a diversified pool of debt instruments, which can include bonds, loans, and other types of debt. |

| Underlying Assets | Primarily consists of syndicated senior secured loans to corporations. | Comprises a mix of various debt types: bonds, loans, mortgage-backed securities, and other fixed-income assets. |

| Purpose | To distribute credit risk from corporate loans to different tranches with varying risk and return profiles. | To pool different debt obligations, redistribute risk, and offer various tranches with distinct credit ratings. |

| Risk Profile | Generally perceived as less risky than CDOs due to greater loan diversification and seniority of underlying loans. | Can carry higher risk, especially if backed by lower-quality assets such as subprime mortgages. |

| Historical Context | Grew in prominence after the 2008 financial crisis as a more transparent loan-based structured product. | Widely used before the 2008 financial crisis, notably including subprime mortgage-backed CDOs linked to the crisis. |

| Investor Base | Attracts institutional investors seeking leveraged loan exposure with credit enhancement. | Appeals to investors interested in diversified exposure to various debt instruments with tailored risk/return. |

| Credit Enhancement | Uses overcollateralization, excess spread, and subordination to protect senior tranches from defaults. | Employs similar credit enhancement techniques but may vary depending on underlying asset quality. |

| Regulation | Subject to evolving regulations focused on transparency and risk mitigation in bank loan markets. | Regulated within structured finance frameworks, with increased scrutiny post-2008 crisis. |

Collateralized Loan Obligation (CLO)

Collateralized Loan Obligation (CLO) is a structured financial product backed by a diversified pool of corporate loans, primarily leveraged loans extended to non-investment grade companies. CLOs are divided into tranches with varying risk and return profiles, attracting investors seeking different levels of yield and credit risk. By actively managing the portfolio, CLO managers aim to maximize returns while mitigating defaults, supported by cash flow waterfalls prioritizing senior debt payments. The global CLO market exceeded $1 trillion in assets under management as of 2023, reflecting its significance in corporate credit financing and investor portfolios.

Collateralized Debt Obligation (CDO)

Collateralized Debt Obligations (CDOs) are structured financial products that pool various debt instruments, such as bonds and loans, into tranches with different risk levels and returns. These securities redistribute credit risk by slicing the pooled assets into senior, mezzanine, and equity tranches, catering to investors with varying risk appetites. CDOs played a significant role in the 2008 financial crisis due to their complexity and the underestimation of default correlations within subprime mortgage assets. Modern regulatory frameworks like Basel III impose stricter capital requirements on banks holding CDOs to mitigate systemic risk.

Underlying Assets

Underlying assets in finance refer to the fundamental financial instruments or securities upon which derivative contracts like options, futures, or swaps are based. These assets can include stocks, bonds, commodities, currencies, or market indexes that determine the value and payoff of the derivative. Accurate valuation of underlying assets is crucial for risk management and pricing strategies in financial markets. Market fluctuations in the price of underlying assets directly impact the performance and risk exposure of related derivative instruments.

Risk Tranches

Risk tranches are segments of debt or credit instruments divided based on varying risk levels and repayment priorities, commonly used in structured finance products like collateralized debt obligations (CDOs) and mortgage-backed securities (MBS). Senior tranches typically hold the highest credit rating, often AAA, and receive priority on cash flows, while mezzanine and equity tranches carry higher risk but offer greater potential returns. The structuring of risk tranches allows investors to select exposure aligned with their risk tolerance and investment objectives. These tranches facilitate risk distribution and capital efficiency in financial markets by allocating losses in a predetermined hierarchy.

Portfolio Diversification

Portfolio diversification involves spreading investments across various asset classes such as stocks, bonds, real estate, and commodities to reduce risk and enhance returns. According to Modern Portfolio Theory, diversification lowers the portfolio's overall volatility by minimizing exposure to individual asset risks. Studies by Vanguard demonstrate that a well-diversified portfolio can improve risk-adjusted returns by up to 20%. Asset allocation strategies typically emphasize the inclusion of uncorrelated assets to optimize the risk-return profile.

Source and External Links

CLOs vs. CDOs: Understanding the Difference - This video discusses the differences between CLOs and CDOs, highlighting their distinct risk profiles due to underlying collateral and historical performance.

CLOs vs. CDOs: Understanding the Difference - This blog post distinguishes between CLOs and CDOs, emphasizing transparency and asset quality differences that impact investor risk.

CLOs Versus CDOs: What's the Difference? - This article highlights the low default rates of CLOs compared to CDOs, showcasing CLOs as a more stable investment option.

FAQs

What is a CLO?

A CLO (Collateralized Loan Obligation) is a structured financial product that pools diversified corporate loans and issues tranches of debt securities with varying risk and return profiles to investors.

What is a CDO?

A Chief Data Officer (CDO) is an executive responsible for overseeing data management, governance, and strategy to ensure data assets deliver business value.

How are CLOs different from CDOs?

CLOs (Collateralized Loan Obligations) primarily pool corporate loans, mainly leveraged loans, while CDOs (Collateralized Debt Obligations) encompass a broader range of debt instruments, including mortgages, bonds, and loans; CLOs focus on senior secured loans with higher credit quality and typically have more stable cash flows compared to the diverse and riskier assets in CDOs.

What assets back CLOs and CDOs?

Collateralized Loan Obligations (CLOs) are backed primarily by diversified pools of syndicated senior secured loans, usually issued by below-investment-grade corporate borrowers. Collateralized Debt Obligations (CDOs) are backed by varied asset classes including corporate bonds, mortgage-backed securities, asset-backed securities, or a mix of debt instruments.

How do CLOs and CDOs generate returns?

CLOs generate returns by pooling leveraged loans and collecting interest payments, then distributing cash flows to tranches based on priority; CDOs generate returns by bundling various debt instruments, managing cash flows from underlying assets, and distributing payments to tranches, profiting from interest spreads and credit enhancements.

Who invests in CLOs vs. CDOs?

Hedge funds, insurance companies, and pension funds primarily invest in Collateralized Loan Obligations (CLOs), while structured finance investors, including banks and specialized asset managers, typically buy Collateralized Debt Obligations (CDOs).

What risks are associated with CLOs and CDOs?

Risks associated with CLOs and CDOs include credit risk, market risk, liquidity risk, and complexity risk due to their layered debt structures and reliance on underlying asset performance.