Systematic risk refers to the overall market risk that affects all securities and cannot be eliminated through diversification, including factors such as economic recessions, interest rate changes, and geopolitical events. Idiosyncratic risk, also known as unsystematic risk, is specific to a particular company or industry and can be mitigated through portfolio diversification. Explore the key differences and implications of systematic versus idiosyncratic risk for effective investment strategies.

Main Difference

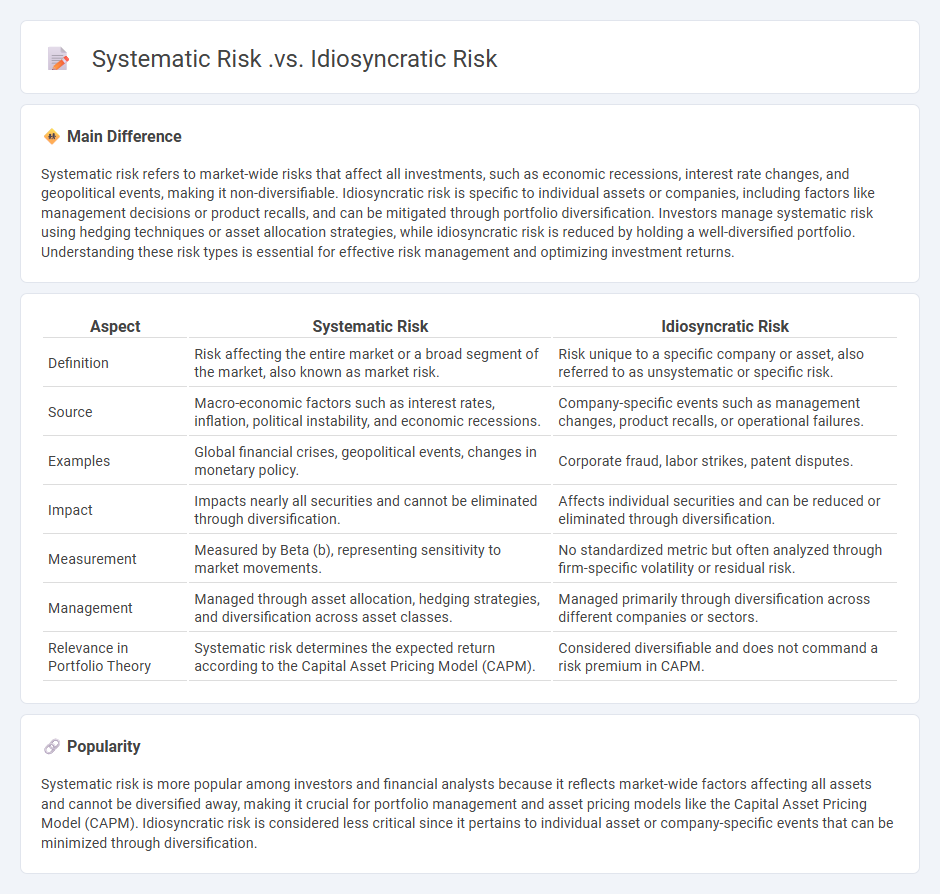

Systematic risk refers to market-wide risks that affect all investments, such as economic recessions, interest rate changes, and geopolitical events, making it non-diversifiable. Idiosyncratic risk is specific to individual assets or companies, including factors like management decisions or product recalls, and can be mitigated through portfolio diversification. Investors manage systematic risk using hedging techniques or asset allocation strategies, while idiosyncratic risk is reduced by holding a well-diversified portfolio. Understanding these risk types is essential for effective risk management and optimizing investment returns.

Connection

Systematic risk affects the entire market and cannot be eliminated through diversification, while idiosyncratic risk is specific to individual assets and can be mitigated by portfolio diversification. Both types of risk influence an investor's overall risk exposure, with systematic risk driven by macroeconomic factors such as interest rates, inflation, and geopolitical events. Understanding the relationship between these risks helps in constructing optimized portfolios that balance market-wide uncertainties with asset-specific volatility.

Comparison Table

| Aspect | Systematic Risk | Idiosyncratic Risk |

|---|---|---|

| Definition | Risk affecting the entire market or a broad segment of the market, also known as market risk. | Risk unique to a specific company or asset, also referred to as unsystematic or specific risk. |

| Source | Macro-economic factors such as interest rates, inflation, political instability, and economic recessions. | Company-specific events such as management changes, product recalls, or operational failures. |

| Examples | Global financial crises, geopolitical events, changes in monetary policy. | Corporate fraud, labor strikes, patent disputes. |

| Impact | Impacts nearly all securities and cannot be eliminated through diversification. | Affects individual securities and can be reduced or eliminated through diversification. |

| Measurement | Measured by Beta (b), representing sensitivity to market movements. | No standardized metric but often analyzed through firm-specific volatility or residual risk. |

| Management | Managed through asset allocation, hedging strategies, and diversification across asset classes. | Managed primarily through diversification across different companies or sectors. |

| Relevance in Portfolio Theory | Systematic risk determines the expected return according to the Capital Asset Pricing Model (CAPM). | Considered diversifiable and does not command a risk premium in CAPM. |

Systematic Risk

Systematic risk refers to the inherent uncertainty affecting the entire financial market or a broad segment, influenced by macroeconomic factors such as inflation, interest rates, recessions, and geopolitical events. It cannot be eliminated through diversification, as it impacts nearly all assets simultaneously. Investors often manage systematic risk using hedging strategies or asset allocation to mitigate potential losses during market downturns. Key indicators like the beta coefficient measure a security's sensitivity to systematic risk compared to the overall market.

Idiosyncratic Risk

Idiosyncratic risk refers to the risk unique to a specific asset or company, which cannot be eliminated through diversification. It contrasts with systematic risk, which affects the entire market or a large segment of it. Investors mitigate idiosyncratic risk by holding a well-diversified portfolio, as the unsystematic fluctuations cancel out across assets. Examples include management changes, product recalls, or regulatory impacts affecting a single firm rather than the broader economy.

Diversification

Diversification in finance involves spreading investments across various asset classes, such as stocks, bonds, real estate, and commodities, to reduce risk and enhance portfolio stability. According to Modern Portfolio Theory introduced by Harry Markowitz, diversification helps minimize unsystematic risk by allocating capital among uncorrelated or negatively correlated assets. Empirical studies show diversified portfolios tend to deliver more consistent returns and lower volatility over time compared to concentrated holdings. Mutual funds and exchange-traded funds (ETFs) are common vehicles that provide investors with easy access to diversified investment strategies.

Market Factors

Market factors in finance refer to external and internal elements that influence the supply, demand, and pricing of financial assets such as stocks, bonds, and commodities. Key factors include interest rates set by central banks, inflation rates impacting purchasing power, and geopolitical events that trigger market volatility. Investor sentiment and economic indicators like GDP growth also shape market trends and asset valuations. Understanding these variables helps investors and analysts forecast market movements and make informed financial decisions.

Portfolio Management

Portfolio management involves the strategic allocation of financial assets such as stocks, bonds, and alternative investments to meet specific investment goals. It requires continuous analysis of market trends, risk tolerance, and asset performance to optimize returns. Effective portfolio management balances diversification and risk, employing techniques like asset allocation, rebalancing, and performance metrics such as the Sharpe ratio. Leading frameworks include Modern Portfolio Theory and the Capital Asset Pricing Model, which guide decision-making in maximizing return per unit of risk.

Source and External Links

Idiosyncratic vs. Systemic Risk. What's the Difference and Why Does ... - Systematic risk affects many securities or the entire market and cannot be diversified away, while idiosyncratic risk only affects a specific security and can be mitigated through diversification.

Idiosyncratic Risk | Definition + Examples - Wall Street Prep - Idiosyncratic risk is diversifiable risk unique to a specific company or sub-sector, whereas systematic risk is non-diversifiable and linked to the broader market or economy.

Idiosyncratic Risk - Definition, Types, Examples - Idiosyncratic (unsystematic) risk is company-specific and can be reduced by diversification; systematic risk affects the entire market or asset class and cannot be avoided by diversification.

FAQs

What is systematic risk?

Systematic risk is the inherent risk affecting the entire market or a broad segment, driven by macroeconomic factors like interest rates, inflation, and geopolitical events, and cannot be eliminated through diversification.

What is idiosyncratic risk?

Idiosyncratic risk is the risk specific to an individual asset or company, unrelated to the overall market movements, and can be reduced through diversification.

How do systematic and idiosyncratic risks differ?

Systematic risk affects the entire market or economy, such as interest rate changes or recessions, while idiosyncratic risk is specific to a single company or industry and can be mitigated through diversification.

What are examples of systematic risk?

Examples of systematic risk include interest rate fluctuations, inflation, recessions, political instability, and global pandemics.

What are examples of idiosyncratic risk?

Examples of idiosyncratic risk include company-specific factors such as management changes, product recalls, labor strikes, regulatory challenges, and competitive disadvantages.

Can idiosyncratic risk be diversified away?

Idiosyncratic risk can be diversified away through a well-diversified portfolio.

Why is understanding both risks important for investors?

Understanding both market risk and credit risk is important for investors to make informed decisions, diversify portfolios effectively, and minimize potential financial losses.