Rehypothecation involves a borrower using assets pledged by the borrower as collateral for additional loans, whereas hypothecation refers to the original pledging of assets to secure a loan without transferring ownership. Both practices impact liquidity and risk management in financial markets, particularly within securities lending and margin trading. Explore further to understand the implications and legal frameworks surrounding rehypothecation and hypothecation.

Main Difference

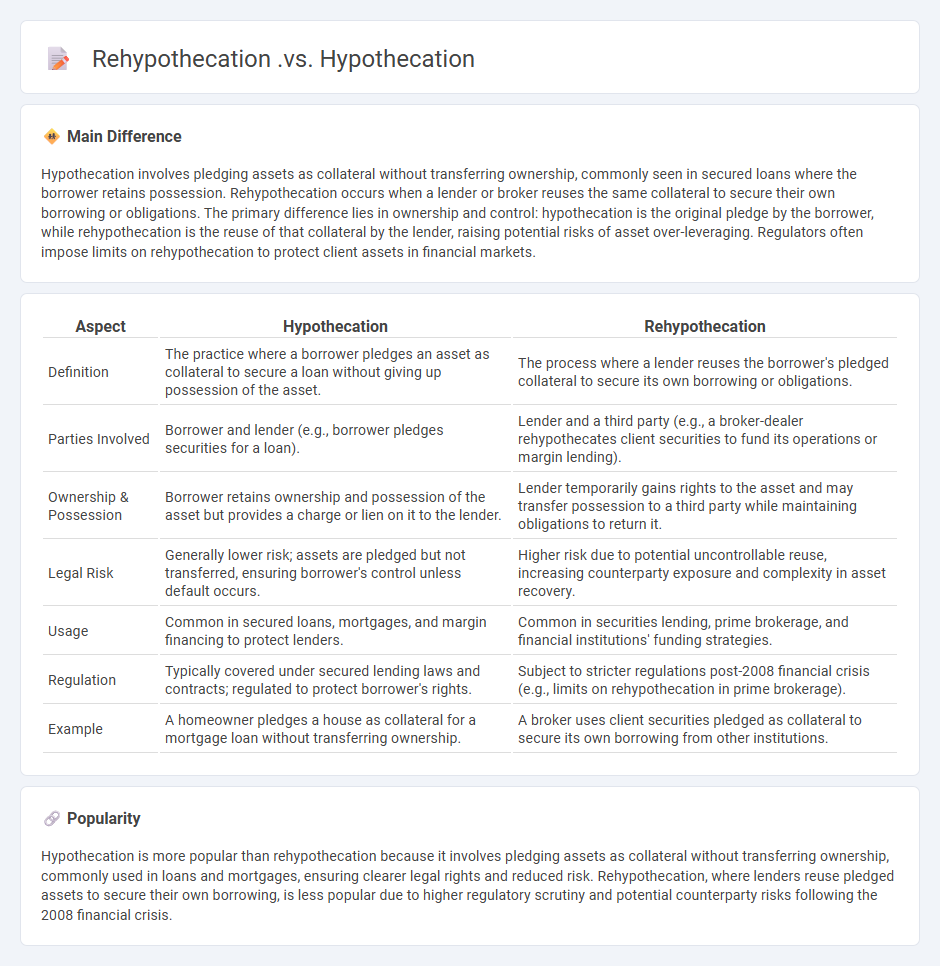

Hypothecation involves pledging assets as collateral without transferring ownership, commonly seen in secured loans where the borrower retains possession. Rehypothecation occurs when a lender or broker reuses the same collateral to secure their own borrowing or obligations. The primary difference lies in ownership and control: hypothecation is the original pledge by the borrower, while rehypothecation is the reuse of that collateral by the lender, raising potential risks of asset over-leveraging. Regulators often impose limits on rehypothecation to protect client assets in financial markets.

Connection

Rehypothecation involves the reuse of collateral that was originally pledged through hypothecation by a borrower to secure a loan or credit. Hypothecation establishes the initial lien or claim on assets without transferring ownership, while rehypothecation allows the lender to pledge that same collateral to another party, increasing liquidity in financial markets. This interconnected process facilitates efficient capital flow but also introduces risks related to asset over-leveraging and counterparty exposure.

Comparison Table

| Aspect | Hypothecation | Rehypothecation |

|---|---|---|

| Definition | The practice where a borrower pledges an asset as collateral to secure a loan without giving up possession of the asset. | The process where a lender reuses the borrower's pledged collateral to secure its own borrowing or obligations. |

| Parties Involved | Borrower and lender (e.g., borrower pledges securities for a loan). | Lender and a third party (e.g., a broker-dealer rehypothecates client securities to fund its operations or margin lending). |

| Ownership & Possession | Borrower retains ownership and possession of the asset but provides a charge or lien on it to the lender. | Lender temporarily gains rights to the asset and may transfer possession to a third party while maintaining obligations to return it. |

| Legal Risk | Generally lower risk; assets are pledged but not transferred, ensuring borrower's control unless default occurs. | Higher risk due to potential uncontrollable reuse, increasing counterparty exposure and complexity in asset recovery. |

| Usage | Common in secured loans, mortgages, and margin financing to protect lenders. | Common in securities lending, prime brokerage, and financial institutions' funding strategies. |

| Regulation | Typically covered under secured lending laws and contracts; regulated to protect borrower's rights. | Subject to stricter regulations post-2008 financial crisis (e.g., limits on rehypothecation in prime brokerage). |

| Example | A homeowner pledges a house as collateral for a mortgage loan without transferring ownership. | A broker uses client securities pledged as collateral to secure its own borrowing from other institutions. |

Collateral

Collateral in finance refers to an asset pledged by a borrower to secure a loan, reducing the lender's risk in case of default. Common forms of collateral include real estate, vehicles, inventory, and accounts receivable, each varying in liquidity and market value. Lending institutions evaluate collateral based on its market worth and ease of liquidation to determine loan eligibility and terms. Proper use of collateral facilitates lower interest rates and higher loan amounts, benefiting both borrowers and lenders.

Ownership Rights

Ownership rights in finance refer to the legal entitlements that confer control, use, and benefits over assets or property. These rights enable owners to transfer, sell, lease, or use an asset to generate income or secure financing. Common examples include shareholders' equity in corporations, where ownership rights grant voting power and dividend claims proportional to shareholding. Clear ownership rights are crucial for efficient capital markets, as they reduce disputes and enhance asset liquidity.

Risk Exposure

Risk exposure in finance refers to the potential for financial loss due to various market, credit, operational, or liquidity risks. It quantifies the degree to which an entity is vulnerable to adverse events affecting asset values or cash flows. Financial institutions measure risk exposure through value-at-risk (VaR), stress testing, and scenario analysis to manage capital reserves and ensure regulatory compliance. Accurate assessment of risk exposure supports informed decision-making and strategic risk mitigation in portfolio management.

Reuse of Assets

Asset reuse in finance involves reallocating existing financial resources or physical assets to maximize value and reduce costs. This practice enhances capital efficiency by extending the useful life of assets such as equipment, technology, or intellectual property. Financial institutions leverage asset reuse strategies to improve liquidity and support sustainable investment models. Data from Deloitte indicates that enterprises implementing asset reuse report a 20-30% reduction in operational expenditures.

Counterparty

A counterparty in finance refers to the other party involved in a financial transaction or contract, such as a swap, derivative, or loan agreement. Counterparty risk is the potential that this party may default on its contractual obligations, causing financial loss. Financial institutions use credit assessments, collateral requirements, and netting arrangements to mitigate counterparty risk. Regulators require robust risk management practices to ensure market stability and reduce systemic exposure.

Source and External Links

Rehypothecation - eCapital - Hypothecation is the initial act where a client pledges collateral to a broker to secure a loan, retaining ownership but granting the broker rights in case of default; rehypothecation is when the broker reuses that collateral to secure its own financing or obligations.

Avoiding the Risks of Rehypothecation in Personal Finance | Hexn - Hypothecation occurs when a borrower pledges an asset as collateral for a loan while rehypothecation happens when the broker uses that pledged collateral to secure their own loans, effectively further pledging the asset beyond the original agreement.

Concepts: Rehypothecation - News & Insights - First Digital - Hypothecation is the initial collateral pledge by a client, whereas rehypothecation involves the broker or custodian re-using that pledged asset to back their own loans or trading, often offering clients reduced borrowing costs in exchange for this right.

FAQs

What is hypothecation?

Hypothecation is the practice of pledging an asset as collateral to secure a loan without transferring its ownership or possession to the lender.

What is rehypothecation?

Rehypothecation is the practice where financial institutions use clients' collateral pledged for loans to secure their own borrowing or investment activities.

How do hypothecation and rehypothecation differ?

Hypothecation involves pledging an asset as collateral without transferring ownership, while rehypothecation allows the lender to reuse the pledged collateral for their own borrowing or trading purposes.

What assets are involved in hypothecation?

Hypothecation involves movable assets such as machinery, vehicles, stock, and accounts receivable used as collateral for loans without transferring ownership.

Why do financial institutions use rehypothecation?

Financial institutions use rehypothecation to increase liquidity, reduce funding costs, and optimize collateral management by reusing client assets for securing their own borrowing or trading activities.

What are the risks of rehypothecation for clients?

Rehypothecation risks for clients include loss of asset control, increased exposure to creditors if the intermediary defaults, reduced transparency of asset holdings, potential delays in asset recovery, and amplified counterparty risk.

How are investor protections different for hypothecation and rehypothecation?

Investor protections for hypothecation ensure that the investor's assets remain legally owned by them and are only used as collateral without transfer of ownership, while rehypothecation allows the lender to reuse the collateral for their own purposes, exposing investors to higher risks and potential loss of control over their assets.