Securitization transforms illiquid assets into tradable securities, enhancing liquidity and risk distribution in financial markets. Credit derivatives, such as credit default swaps, enable the transfer and management of credit risk without altering asset ownership. Explore the key differences and applications of securitization and credit derivatives for a deeper understanding of financial risk management.

Main Difference

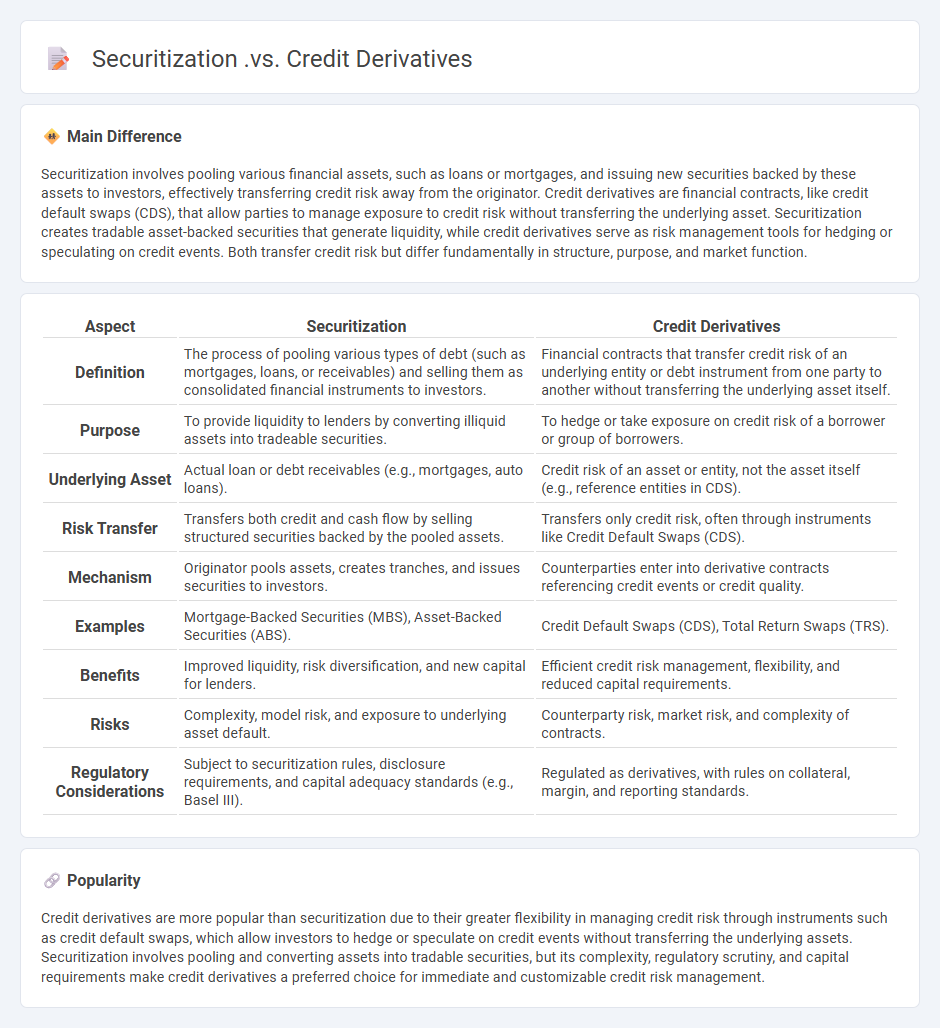

Securitization involves pooling various financial assets, such as loans or mortgages, and issuing new securities backed by these assets to investors, effectively transferring credit risk away from the originator. Credit derivatives are financial contracts, like credit default swaps (CDS), that allow parties to manage exposure to credit risk without transferring the underlying asset. Securitization creates tradable asset-backed securities that generate liquidity, while credit derivatives serve as risk management tools for hedging or speculating on credit events. Both transfer credit risk but differ fundamentally in structure, purpose, and market function.

Connection

Securitization and credit derivatives are interconnected financial tools that manage credit risk and enhance liquidity. Securitization transforms illiquid assets, such as loans or mortgages, into tradable securities, while credit derivatives like credit default swaps allow investors to transfer or hedge credit exposure linked to these underlying securities. This connection enables more efficient risk distribution and capital allocation across financial markets.

Comparison Table

| Aspect | Securitization | Credit Derivatives |

|---|---|---|

| Definition | The process of pooling various types of debt (such as mortgages, loans, or receivables) and selling them as consolidated financial instruments to investors. | Financial contracts that transfer credit risk of an underlying entity or debt instrument from one party to another without transferring the underlying asset itself. |

| Purpose | To provide liquidity to lenders by converting illiquid assets into tradeable securities. | To hedge or take exposure on credit risk of a borrower or group of borrowers. |

| Underlying Asset | Actual loan or debt receivables (e.g., mortgages, auto loans). | Credit risk of an asset or entity, not the asset itself (e.g., reference entities in CDS). |

| Risk Transfer | Transfers both credit and cash flow by selling structured securities backed by the pooled assets. | Transfers only credit risk, often through instruments like Credit Default Swaps (CDS). |

| Mechanism | Originator pools assets, creates tranches, and issues securities to investors. | Counterparties enter into derivative contracts referencing credit events or credit quality. |

| Examples | Mortgage-Backed Securities (MBS), Asset-Backed Securities (ABS). | Credit Default Swaps (CDS), Total Return Swaps (TRS). |

| Benefits | Improved liquidity, risk diversification, and new capital for lenders. | Efficient credit risk management, flexibility, and reduced capital requirements. |

| Risks | Complexity, model risk, and exposure to underlying asset default. | Counterparty risk, market risk, and complexity of contracts. |

| Regulatory Considerations | Subject to securitization rules, disclosure requirements, and capital adequacy standards (e.g., Basel III). | Regulated as derivatives, with rules on collateral, margin, and reporting standards. |

Asset Pooling

Asset pooling in finance refers to the aggregation of various financial assets, such as loans, mortgages, or bonds, into a single collective investment vehicle. This technique enhances diversification and risk management by spreading exposure across multiple underlying assets. Common examples include mortgage-backed securities (MBS) and collateralized debt obligations (CDOs), which enable investors to access a broad range of credit products while optimizing returns. Regulatory frameworks and credit rating agencies often evaluate pooled assets to ensure transparency and risk assessment accuracy.

Risk Transfer

Risk transfer in finance involves shifting potential financial losses from one party to another through mechanisms such as insurance policies, derivatives, or hedging strategies. Companies frequently use risk transfer to mitigate exposure to market volatility, credit defaults, or operational hazards, effectively stabilizing cash flows and protecting asset values. Instruments like credit default swaps and options are common tools enabling efficient risk allocation between risk-averse and risk-seeking entities. Regulatory frameworks often encourage transparent risk transfer practices to enhance systemic stability and reduce financial contagion.

Tranching

Tranching in finance refers to the process of dividing a pool of financial assets, such as mortgages or bonds, into different segments called tranches that vary by risk, return, and maturity. Each tranche is structured to target specific investor preferences, ranging from senior tranches with lower risk and lower returns to junior tranches with higher risk and higher potential yields. This technique is commonly used in structured finance products like collateralized debt obligations (CDOs) and mortgage-backed securities (MBS). By creating tranches, issuers can tailor investment opportunities to a diverse range of risk appetites and optimize capital allocation.

Synthetic Exposure

Synthetic exposure in finance refers to gaining market exposure to an asset without directly owning it, typically achieved through derivatives such as options, futures, or swaps. This strategy allows investors to replicate the payoff of an asset by using instruments like total return swaps or options contracts, managing risk and capital more efficiently. By creating synthetic positions, market participants can hedge existing exposures, speculate on price movements, or access otherwise illiquid markets. Major financial institutions and hedge funds utilize synthetic exposure to optimize portfolio performance and implement complex investment strategies.

Credit Default Swap

Credit Default Swaps (CDS) are financial derivatives that enable investors to hedge or speculate on the credit risk of a borrower, typically corporate or sovereign entities. They function as insurance contracts where the buyer pays periodic premiums to the seller in exchange for compensation if the borrower defaults or undergoes a credit event. The global CDS market size reached approximately $10 trillion in notional value by 2023, reflecting its significance in risk management and capital structure strategies. CDS pricing depends on factors such as the reference entity's credit rating, default probability, and market liquidity.

Source and External Links

Back to basics: What Is Securitization? - Securitization involves pooling assets to transfer credit risk and tailor risk-return profiles for investors, unlike conventional debt, and can include true sale or synthetic securitization where only credit risk is transferred.

Securitisation, credit risk and lending standards revisited - Securitisation allows banks to transfer credit risk to investors, affecting lending standards and monitoring incentives, and may contribute to financial stability challenges.

SECURITIZATION AND DERIVATIVES - Credit derivatives like credit default swaps (CDS) differ from securitization; CDS transfer default risk on debt without transferring ownership and act like insurance but are unregulated OTC derivatives allowing speculation beyond ownership.

FAQs

What is securitization?

Securitization is the financial process of pooling various types of debt, such as mortgages or loans, and transforming them into tradable securities to raise capital and distribute risk.

What are credit derivatives?

Credit derivatives are financial contracts that transfer credit risk of an underlying entity between parties without transferring the underlying asset.

How does securitization differ from credit derivatives?

Securitization involves pooling financial assets to create tradable securities backed by those assets, while credit derivatives are financial contracts that transfer credit risk between parties without transferring the underlying assets.

What assets are typically securitized?

Typical securitized assets include residential mortgages, commercial mortgages, auto loans, credit card receivables, student loans, and equipment leases.

What are the main types of credit derivatives?

The main types of credit derivatives are credit default swaps (CDS), total return swaps (TRS), credit-linked notes (CLN), and collateralized debt obligations (CDO).

What risks do securitization and credit derivatives address?

Securitization and credit derivatives address credit risk, liquidity risk, and market risk by transferring or mitigating potential losses from defaulted loans and improving capital efficiency.

How do securitization and credit derivatives impact financial markets?

Securitization enhances liquidity by converting illiquid assets into tradable securities, while credit derivatives transfer and manage credit risk, both improving market efficiency and risk distribution in financial markets.