Government Investment Corporations (GIC) and Mortgage-Backed Securities (MBS) represent distinct financial instruments with unique risk profiles and investment strategies. GICs are typically low-risk, government-guaranteed fixed-income investments, while MBS involve pools of mortgage loans offering higher yields but with greater exposure to market fluctuations. Explore the differences and benefits of GICs and MBS to make informed investment choices.

Main Difference

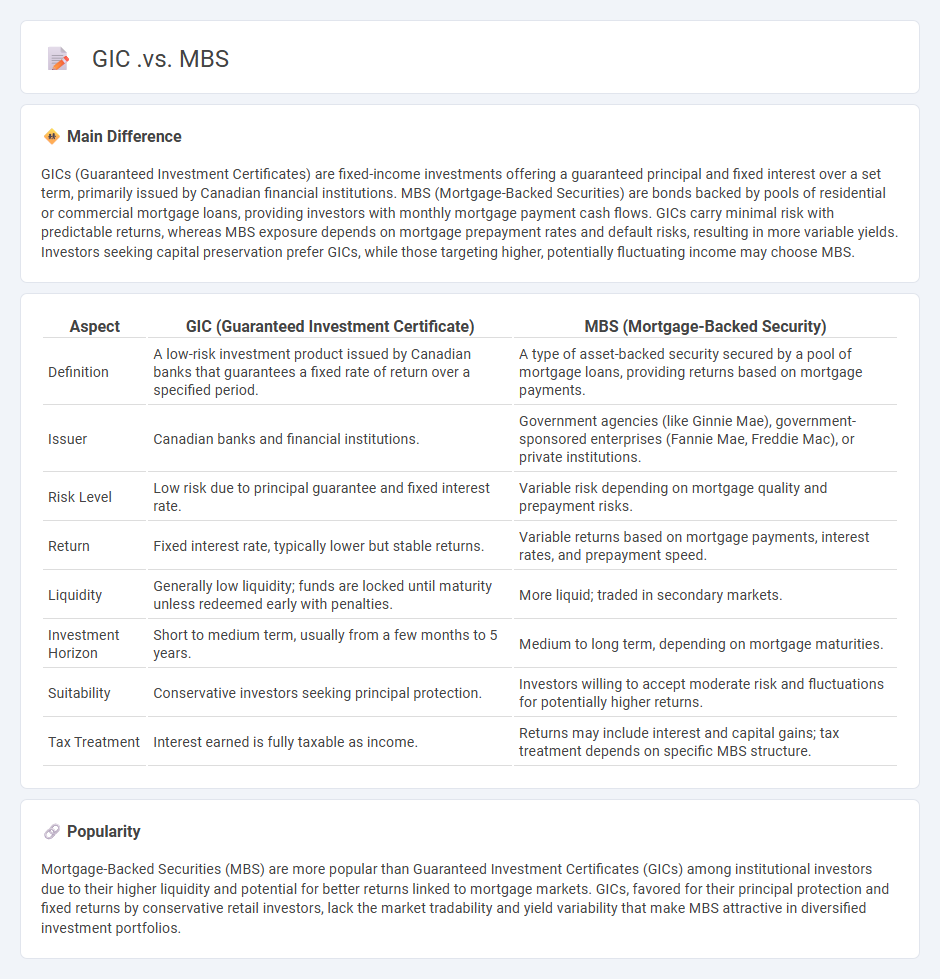

GICs (Guaranteed Investment Certificates) are fixed-income investments offering a guaranteed principal and fixed interest over a set term, primarily issued by Canadian financial institutions. MBS (Mortgage-Backed Securities) are bonds backed by pools of residential or commercial mortgage loans, providing investors with monthly mortgage payment cash flows. GICs carry minimal risk with predictable returns, whereas MBS exposure depends on mortgage prepayment rates and default risks, resulting in more variable yields. Investors seeking capital preservation prefer GICs, while those targeting higher, potentially fluctuating income may choose MBS.

Connection

GIC (Government Investment Corporation) invests significantly in MBS (Mortgage-Backed Securities) as part of its diversified portfolio to generate stable, long-term returns. MBS provide GIC with exposure to the U.S. housing market and fixed-income assets, enhancing yield while managing credit risk. This connection underscores GIC's strategic allocation to securitized assets to optimize portfolio performance and risk-adjusted returns.

Comparison Table

| Aspect | GIC (Guaranteed Investment Certificate) | MBS (Mortgage-Backed Security) |

|---|---|---|

| Definition | A low-risk investment product issued by Canadian banks that guarantees a fixed rate of return over a specified period. | A type of asset-backed security secured by a pool of mortgage loans, providing returns based on mortgage payments. |

| Issuer | Canadian banks and financial institutions. | Government agencies (like Ginnie Mae), government-sponsored enterprises (Fannie Mae, Freddie Mac), or private institutions. |

| Risk Level | Low risk due to principal guarantee and fixed interest rate. | Variable risk depending on mortgage quality and prepayment risks. |

| Return | Fixed interest rate, typically lower but stable returns. | Variable returns based on mortgage payments, interest rates, and prepayment speed. |

| Liquidity | Generally low liquidity; funds are locked until maturity unless redeemed early with penalties. | More liquid; traded in secondary markets. |

| Investment Horizon | Short to medium term, usually from a few months to 5 years. | Medium to long term, depending on mortgage maturities. |

| Suitability | Conservative investors seeking principal protection. | Investors willing to accept moderate risk and fluctuations for potentially higher returns. |

| Tax Treatment | Interest earned is fully taxable as income. | Returns may include interest and capital gains; tax treatment depends on specific MBS structure. |

Principal Protection

Principal protection in finance refers to investment strategies designed to safeguard the initial amount of capital invested, minimizing the risk of loss. Common instruments offering principal protection include fixed annuities, government bonds, and structured notes with embedded guarantees. These strategies are particularly popular among risk-averse investors seeking downside protection while maintaining potential for modest returns. Effective principal protection balances security with growth opportunities, often achieved through diversification and capital preservation tactics.

Fixed Income

Fixed income refers to investment securities that provide regular, predetermined interest payments and the return of principal at maturity, such as government and corporate bonds. These instruments offer lower risk compared to equities, making them a key component in diversified investment portfolios. The global fixed income market exceeds $100 trillion, highlighting its critical role in capital markets and economic stability. Key benchmarks include the U.S. Treasury bond yields and investment-grade bond indices like the Bloomberg Barclays U.S. Aggregate Bond Index.

Credit Risk

Credit risk refers to the potential for loss due to a borrower's failure to repay a loan or meet contractual debt obligations. It is a critical component in financial institutions' risk management, influencing lending decisions, interest rates, and capital reserves. Credit risk assessment involves analyzing credit scores, financial statements, and macroeconomic indicators to predict default probabilities. Effective credit risk management mitigates losses and ensures regulatory compliance under frameworks such as Basel III.

Mortgage-backed Securities (MBS)

Mortgage-backed securities (MBS) are financial instruments backed by a pool of home loans, providing investors with periodic payments derived from mortgage principal and interest. These securities enhance liquidity in the housing market by allowing banks to offload mortgage risk and use the proceeds for new loans. Prominent issuers include government-sponsored enterprises like Fannie Mae and Freddie Mac in the United States, whose guarantees significantly influence MBS credit quality. Market performance of MBS is sensitive to interest rate fluctuations and prepayment risks tied to borrower refinancing behavior.

Guaranteed Investment Certificates (GIC)

Guaranteed Investment Certificates (GICs) are fixed-term investments offered primarily by Canadian financial institutions, providing a guaranteed return of principal and interest. They typically range from 30 days to 5 years, with interest rates varying based on term length and market conditions, often outperforming standard savings accounts. Investors benefit from low risk due to Canada Deposit Insurance Corporation (CDIC) coverage up to $100,000 per institution, making GICs a secure option for conservative portfolios. Market trends show growing demand for GICs during economic uncertainty as investors seek capital preservation with predictable returns.

Source and External Links

GICs vs bonds/money markets - GICs offer a guaranteed, typically compounded interest with federal government backing (CDIC), while certain bonds (e.g., strip bonds) often have comparable or sometimes higher yields but with market value fluctuations until maturity; both can be held to maturity for stable returns.

Trying to learn more about Mortgage Backed Securities - Mortgage-backed securities (MBS) can provide higher yields than GICs or bonds, commonly used as a source of monthly income, but they involve different risks and structures linked to pooled mortgage payments.

How to diversify against rising interest rates and inflation - Agency MBS have a lower duration and higher yields compared to government bonds and GICs, with government guarantees and negative correlation to equity markets, offering potentially better performance and portfolio stability during rising interest rate environments.

FAQs

What is a GIC?

A GIC (Guaranteed Investment Certificate) is a Canadian investment that offers a fixed interest rate for a specified term, ensuring the principal amount is protected.

What is an MBS?

An MBS (Mortgage-Backed Security) is a financial asset backed by a pool of residential or commercial mortgage loans, allowing investors to receive periodic payments derived from the underlying mortgage payments.

What is the difference between GIC and MBS?

GIC (Guaranteed Investment Certificate) is a low-risk, fixed-term investment offering guaranteed principal and fixed interest, while MBS (Mortgage-Backed Securities) are asset-backed securities backed by mortgage loans, carrying higher risk and varying returns depending on mortgage performance.

How do GICs generate returns?

GICs generate returns by paying a fixed or variable interest rate over a specified term, allowing investors to earn predictable income through principal preservation and interest accrual.

How do MBS generate returns?

Mortgage-backed securities (MBS) generate returns primarily through the interest and principal payments made by homeowners on the underlying mortgage loans.

What are the risks associated with GICs?

GICs risk low returns compared to inflation, interest rate risk affecting reinvestment rates, liquidity risk due to fixed terms, and credit risk from issuer default, though generally minimal with government-backed GICs.

What are the risks associated with MBS?

Mortgage-backed securities (MBS) carry risks including prepayment risk, interest rate risk, credit/default risk, liquidity risk, and market risk.