Arbitrage Pricing Theory (APT) and the Capital Asset Pricing Model (CAPM) are prominent frameworks used to determine asset prices and expected returns in financial markets. APT relies on multiple macroeconomic factors to explain asset returns, offering a multifactor approach compared to CAPM's single-factor model based solely on market risk. Explore the differences and applications of APT and CAPM to understand their impact on investment strategies and risk assessment.

Main Difference

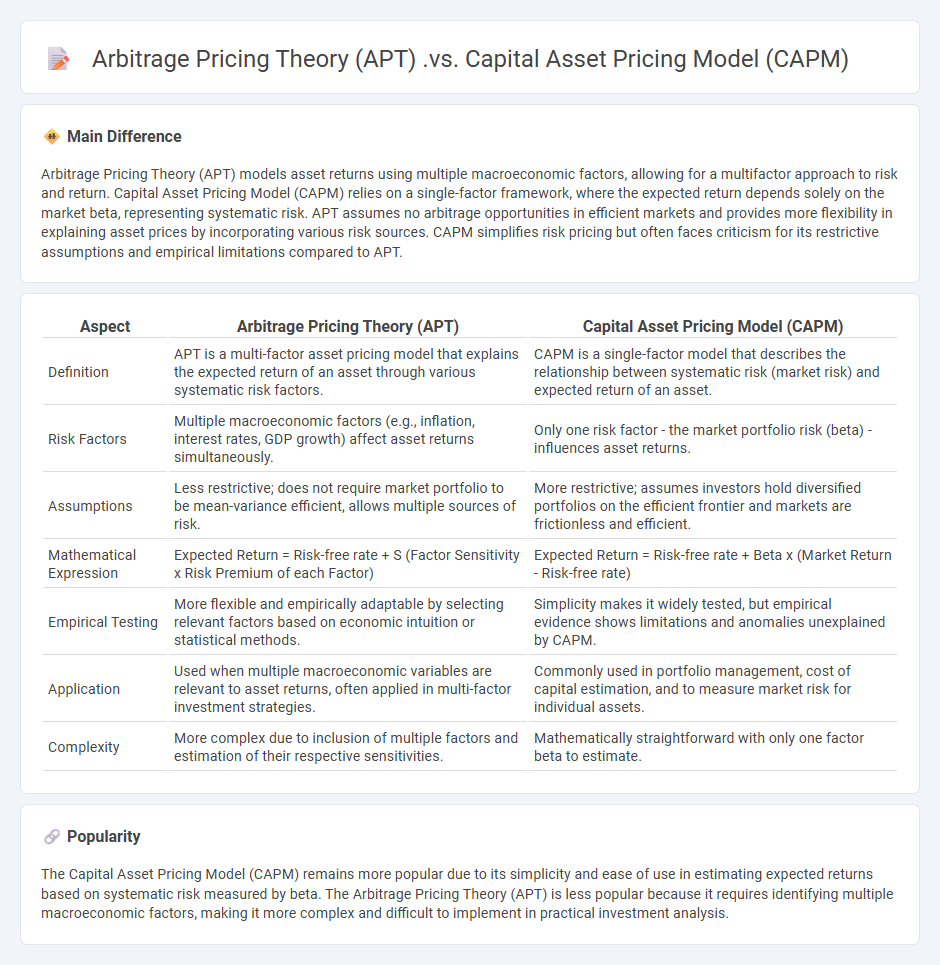

Arbitrage Pricing Theory (APT) models asset returns using multiple macroeconomic factors, allowing for a multifactor approach to risk and return. Capital Asset Pricing Model (CAPM) relies on a single-factor framework, where the expected return depends solely on the market beta, representing systematic risk. APT assumes no arbitrage opportunities in efficient markets and provides more flexibility in explaining asset prices by incorporating various risk sources. CAPM simplifies risk pricing but often faces criticism for its restrictive assumptions and empirical limitations compared to APT.

Connection

Arbitrage Pricing Theory (APT) and Capital Asset Pricing Model (CAPM) are connected through their role in asset pricing, as both models explain expected returns based on risk factors. CAPM relies on a single systematic risk factor, the market portfolio, while APT extends this by incorporating multiple macroeconomic factors influencing asset returns. Both frameworks assume no arbitrage opportunities, linking expected returns to risk, but APT offers greater flexibility by accommodating multiple sources of systematic risk.

Comparison Table

| Aspect | Arbitrage Pricing Theory (APT) | Capital Asset Pricing Model (CAPM) |

|---|---|---|

| Definition | APT is a multi-factor asset pricing model that explains the expected return of an asset through various systematic risk factors. | CAPM is a single-factor model that describes the relationship between systematic risk (market risk) and expected return of an asset. |

| Risk Factors | Multiple macroeconomic factors (e.g., inflation, interest rates, GDP growth) affect asset returns simultaneously. | Only one risk factor - the market portfolio risk (beta) - influences asset returns. |

| Assumptions | Less restrictive; does not require market portfolio to be mean-variance efficient, allows multiple sources of risk. | More restrictive; assumes investors hold diversified portfolios on the efficient frontier and markets are frictionless and efficient. |

| Mathematical Expression | Expected Return = Risk-free rate + S (Factor Sensitivity x Risk Premium of each Factor) | Expected Return = Risk-free rate + Beta x (Market Return - Risk-free rate) |

| Empirical Testing | More flexible and empirically adaptable by selecting relevant factors based on economic intuition or statistical methods. | Simplicity makes it widely tested, but empirical evidence shows limitations and anomalies unexplained by CAPM. |

| Application | Used when multiple macroeconomic variables are relevant to asset returns, often applied in multi-factor investment strategies. | Commonly used in portfolio management, cost of capital estimation, and to measure market risk for individual assets. |

| Complexity | More complex due to inclusion of multiple factors and estimation of their respective sensitivities. | Mathematically straightforward with only one factor beta to estimate. |

Multi-factor Model (APT)

The Arbitrage Pricing Theory (APT) is a multi-factor financial model used to determine the expected return on assets by considering various macroeconomic factors such as inflation, interest rates, and GDP growth. Unlike the Capital Asset Pricing Model (CAPM), APT does not rely on a single market factor but incorporates multiple systematic risk factors to explain asset price movements. Empirical studies demonstrate that APT can more accurately capture the sensitivities of asset returns to different economic variables, enhancing portfolio management and risk assessment. Practical applications include factor investing strategies where identifying significant risk factors helps optimize diversification and improve performance forecasting.

Single-factor Model (CAPM)

The Single-factor Model, commonly known as the Capital Asset Pricing Model (CAPM), explains the relationship between systematic risk and expected return for assets, particularly stocks. It quantifies expected return as the sum of the risk-free rate and the asset's beta times the market risk premium, where beta measures sensitivity to market movements. Developed by William Sharpe in 1964, CAPM remains foundational in asset pricing and portfolio management. Financial institutions and analysts utilize CAPM for estimating cost of capital and optimizing portfolio risk-return trade-offs.

Systematic Risk Factors

Systematic risk factors refer to broad economic forces that impact the entire financial market, affecting asset prices and investment returns across various sectors. Key systematic risks include interest rate fluctuations, inflation rates, GDP growth, and geopolitical events, which cannot be mitigated through diversification. The Capital Asset Pricing Model (CAPM) quantifies systematic risk using beta, measuring an asset's sensitivity to market movements. Investors must consider these factors when constructing portfolios to manage exposure to market-wide uncertainties effectively.

Beta Coefficient

Beta coefficient measures a stock's volatility relative to the overall market, indicating its systematic risk. A beta of 1 implies the stock moves in line with the market, while a beta greater than 1 suggests higher volatility and risk. Investors use beta to assess expected return adjustments in the Capital Asset Pricing Model (CAPM). For example, a beta of 1.2 indicates the stock theoretically changes 20% more than market movement, informing portfolio risk management.

Real-world Portfolio Diversification

Real-world portfolio diversification reduces risk by allocating investments across various asset classes, including stocks, bonds, real estate, and commodities. Diversification leverages the low correlation between asset returns to mitigate losses from market volatility, enhancing risk-adjusted returns. Empirical data from the CFA Institute indicates well-diversified portfolios historically achieve higher Sharpe ratios compared to concentrated investments. Effective diversification strategies incorporate global equities, emerging markets, and alternative investments to optimize portfolio performance in dynamic economic environments.

Source and External Links

Arbitrage Pricing Theory (APT) - CMA Glossary - APT is a multifactor model that determines an asset's fair value by considering multiple macroeconomic factors and their risk premiums, offering more flexibility than CAPM which relies on a single market index.

Describe The Differences Between CAPM and APT | PDF - CAPM uses market risk alone to estimate expected return as a linear function, while APT models expected returns as a linear function of numerous unknown risk factors, making APT more practical and reliable for asset pricing under varied risks.

Arbitrage Pricing Theory - Defintion, Formula, Example - APT is a multifactor pricing theory that assumes markets can temporarily misprice assets, allowing arbitrageurs to profit until prices revert to equilibrium; it is more flexible but also more complex and time-consuming to apply than CAPM.

FAQs

What is Arbitrage Pricing Theory?

Arbitrage Pricing Theory (APT) is a financial model that explains asset returns through multiple macroeconomic factors, identifying mispriced securities by comparing expected returns against factor sensitivities.

What is the Capital Asset Pricing Model?

The Capital Asset Pricing Model (CAPM) is a financial model that calculates an asset's expected return based on its systematic risk measured by beta, the risk-free rate, and the market risk premium.

How does APT differ from CAPM in assumptions?

APT assumes multiple factors influence asset returns without specifying them, while CAPM relies on a single market factor; APT allows for no arbitrage opportunities and does not require market portfolio efficiency, unlike CAPM which assumes investor rationality, market equilibrium, and a risk-free rate.

What are the main factors considered in APT vs. CAPM?

APT considers multiple macroeconomic factors like inflation, GDP growth, and interest rates, while CAPM focuses solely on market risk measured by beta.

How do risk and return relate in APT and CAPM?

In both APT and CAPM, higher risk corresponds to higher expected return; CAPM links return to a single market beta, while APT relates return to multiple risk factors each with its own risk premium.

Which model is more flexible for asset pricing?

The Arbitrage Pricing Theory (APT) model is more flexible for asset pricing due to its ability to incorporate multiple systematic risk factors.

What are the practical applications of APT and CAPM?

APT models asset returns based on multiple macroeconomic factors for portfolio management and risk assessment; CAPM estimates expected returns using beta for asset pricing, cost of capital, and investment decisions.