Yield curve twist refers to changes in the slope or curvature of the yield curve where short-term and long-term interest rates move in opposite directions, indicating shifts in market expectations for economic growth or inflation. Yield curve shift involves a parallel movement of the entire curve up or down, reflecting uniform changes in interest rate levels across all maturities due to monetary policy or systemic risk factors. Explore deeper insights into how these yield curve dynamics impact investment strategies and economic forecasting.

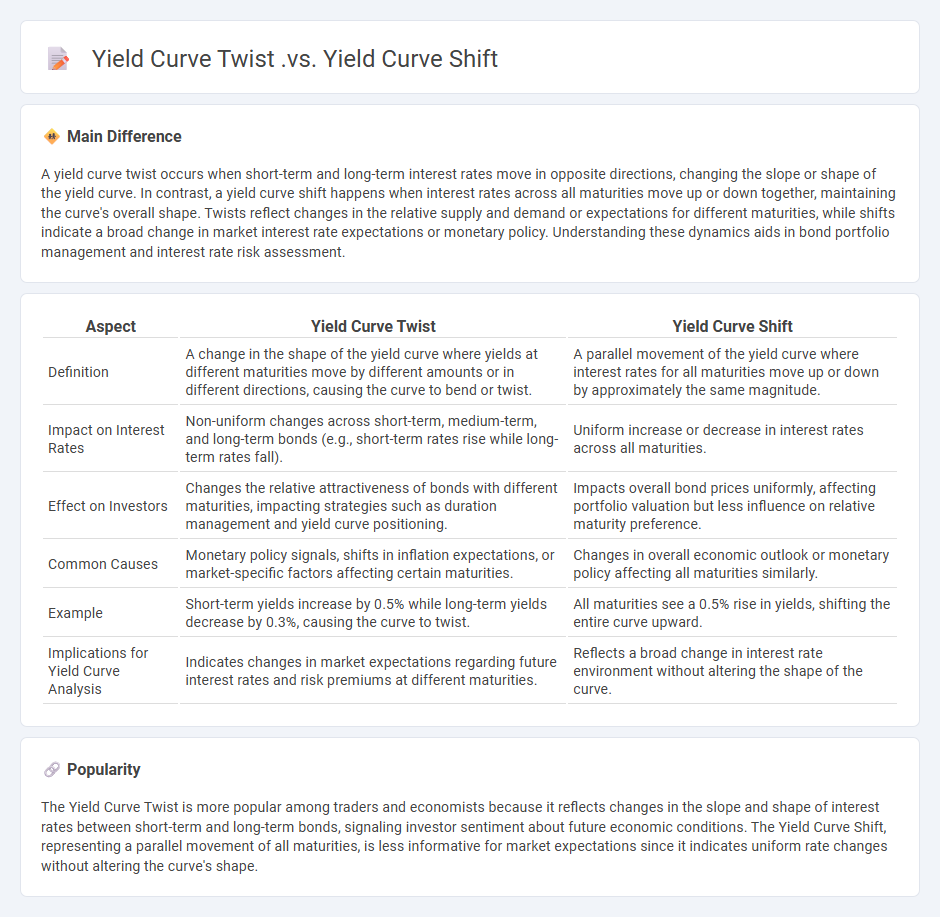

Main Difference

A yield curve twist occurs when short-term and long-term interest rates move in opposite directions, changing the slope or shape of the yield curve. In contrast, a yield curve shift happens when interest rates across all maturities move up or down together, maintaining the curve's overall shape. Twists reflect changes in the relative supply and demand or expectations for different maturities, while shifts indicate a broad change in market interest rate expectations or monetary policy. Understanding these dynamics aids in bond portfolio management and interest rate risk assessment.

Connection

Yield curve twist and yield curve shift both describe movements in the yield curve representing interest rates across different maturities. Yield curve twist occurs when short-term and long-term interest rates move in opposite directions, changing the curve's slope or shape, while yield curve shift involves parallel movements of interest rates across all maturities. These phenomena influence fixed-income markets by affecting bond prices, portfolio strategies, and interest rate risk management.

Comparison Table

| Aspect | Yield Curve Twist | Yield Curve Shift |

|---|---|---|

| Definition | A change in the shape of the yield curve where yields at different maturities move by different amounts or in different directions, causing the curve to bend or twist. | A parallel movement of the yield curve where interest rates for all maturities move up or down by approximately the same magnitude. |

| Impact on Interest Rates | Non-uniform changes across short-term, medium-term, and long-term bonds (e.g., short-term rates rise while long-term rates fall). | Uniform increase or decrease in interest rates across all maturities. |

| Effect on Investors | Changes the relative attractiveness of bonds with different maturities, impacting strategies such as duration management and yield curve positioning. | Impacts overall bond prices uniformly, affecting portfolio valuation but less influence on relative maturity preference. |

| Common Causes | Monetary policy signals, shifts in inflation expectations, or market-specific factors affecting certain maturities. | Changes in overall economic outlook or monetary policy affecting all maturities similarly. |

| Example | Short-term yields increase by 0.5% while long-term yields decrease by 0.3%, causing the curve to twist. | All maturities see a 0.5% rise in yields, shifting the entire curve upward. |

| Implications for Yield Curve Analysis | Indicates changes in market expectations regarding future interest rates and risk premiums at different maturities. | Reflects a broad change in interest rate environment without altering the shape of the curve. |

Yield Curve Twist

A yield curve twist occurs when interest rates change unevenly across different maturities, leading to a shift in the shape of the yield curve without a parallel shift in all maturities. This phenomenon can indicate changing market expectations about economic growth, inflation, or monetary policy. For example, short-term rates might rise while long-term rates fall, flattening the curve, or the opposite can happen, steepening it. Traders and investors analyze yield curve twists to adjust bond portfolios and assess risk in fixed income markets.

Yield Curve Shift

Yield curve shift refers to changes in the interest rates across different maturities on the yield curve, impacting bond prices and investment strategies. A parallel shift moves the entire yield curve up or down by the same number of basis points, affecting fixed-income securities uniformly. Non-parallel shifts, such as steepening or flattening, reflect changes in the spread between short-term and long-term interest rates, signaling evolving economic expectations. Traders and portfolio managers analyze yield curve shifts to assess market sentiment, manage interest rate risk, and optimize asset allocation.

Interest Rate Movements

Interest rate movements significantly impact financial markets, influencing bond prices, stock valuations, and borrowing costs. Central banks' monetary policies often drive these changes by adjusting benchmark rates to control inflation and stimulate economic growth. Investors closely monitor yield curves and economic indicators to predict future rate shifts and manage portfolio risks effectively. Understanding interest rate fluctuations is crucial for corporate finance decisions, including capital budgeting and debt management strategies.

Monetary Policy Impact

Monetary policy directly influences inflation rates, interest rates, and economic growth by controlling the money supply and credit availability. Central banks use tools such as open market operations, discount rates, and reserve requirements to stabilize currency value and promote employment. Changes in monetary policy affect borrowing costs for consumers and businesses, impacting investment and spending decisions. Empirical studies show that timely policy adjustments can mitigate economic recessions and manage inflation expectations effectively.

Duration Risk

Duration risk refers to the sensitivity of a bond or fixed-income portfolio's price to changes in interest rates, measured by the bond's duration. It quantifies the weighted average time until cash flows are received, with longer duration indicating higher price volatility when interest rates fluctuate. Investors managing duration risk aim to minimize losses by matching the duration of assets and liabilities or using hedging strategies such as interest rate swaps. Key metrics used to analyze duration risk include Macaulay Duration, Modified Duration, and Effective Duration, all critical for optimizing portfolio risk exposure in bond markets.

Source and External Links

Pivoting Powell And Yield Curve Twists: How To Dance To The ... - A yield curve shift is typically a parallel movement of yields across maturities, while a yield curve twist involves a change in the slope, such as flattening or steepening, altering the yield difference between short and long maturities without moving all yields uniformly.

Yield Curve Shifts Create Trading Opportunities - CME Group - A yield curve shift refers to a parallel move across all maturities, whereas a twist denotes a change in the slope of the curve, affecting the relative yields of different maturities and is considered a non-parallel shift.

Yield Curve Strategies - CFA, FRM, and Actuarial Exams Study Notes - While a yield curve shift (parallel shift) means uniform rise or fall in rates across maturities, a twist is a non-parallel shift leading to either flattening or steepening of the curve, reflecting differing movements in short-term versus long-term rates.

FAQs

What is a yield curve?

A yield curve is a graph that plots interest rates of bonds having equal credit quality but differing maturity dates, typically illustrating the relationship between short-term and long-term Treasury securities.

What is a yield curve shift?

A yield curve shift refers to a simultaneous change in interest rates across all maturities on the yield curve, causing the entire curve to move up or down.

What is a yield curve twist?

A yield curve twist refers to a change in the slope or shape of the yield curve where short-term and long-term interest rates move in opposite directions, altering the spread between different maturities.

How does a yield curve shift affect interest rates?

A yield curve shift directly changes interest rates across different maturities, causing short-term and long-term rates to rise or fall depending on the shift's direction and shape.

How does a yield curve twist change market expectations?

A yield curve twist alters market expectations by signaling divergent changes in short-term and long-term interest rates, reflecting shifts in economic growth prospects and inflation outlooks.

What causes yield curve twists and shifts?

Yield curve twists occur due to changes in interest rate expectations or differing impacts on short-term versus long-term bonds, while yield curve shifts result from uniform changes in interest rates across all maturities caused by factors like monetary policy adjustments or shifts in inflation expectations.

Why are yield curve movements important for investors?

Yield curve movements are important for investors because they signal changes in interest rates, economic growth expectations, and inflation trends, directly impacting bond pricing, portfolio risk, and investment strategy decisions.