Accrual accounting records revenues and expenses when they are earned or incurred, reflecting a business's financial position over time. Mark-to-market accounting values assets and liabilities based on current market prices, providing real-time assessment of financial status. Explore deeper to understand how each accounting method impacts financial reporting and decision-making.

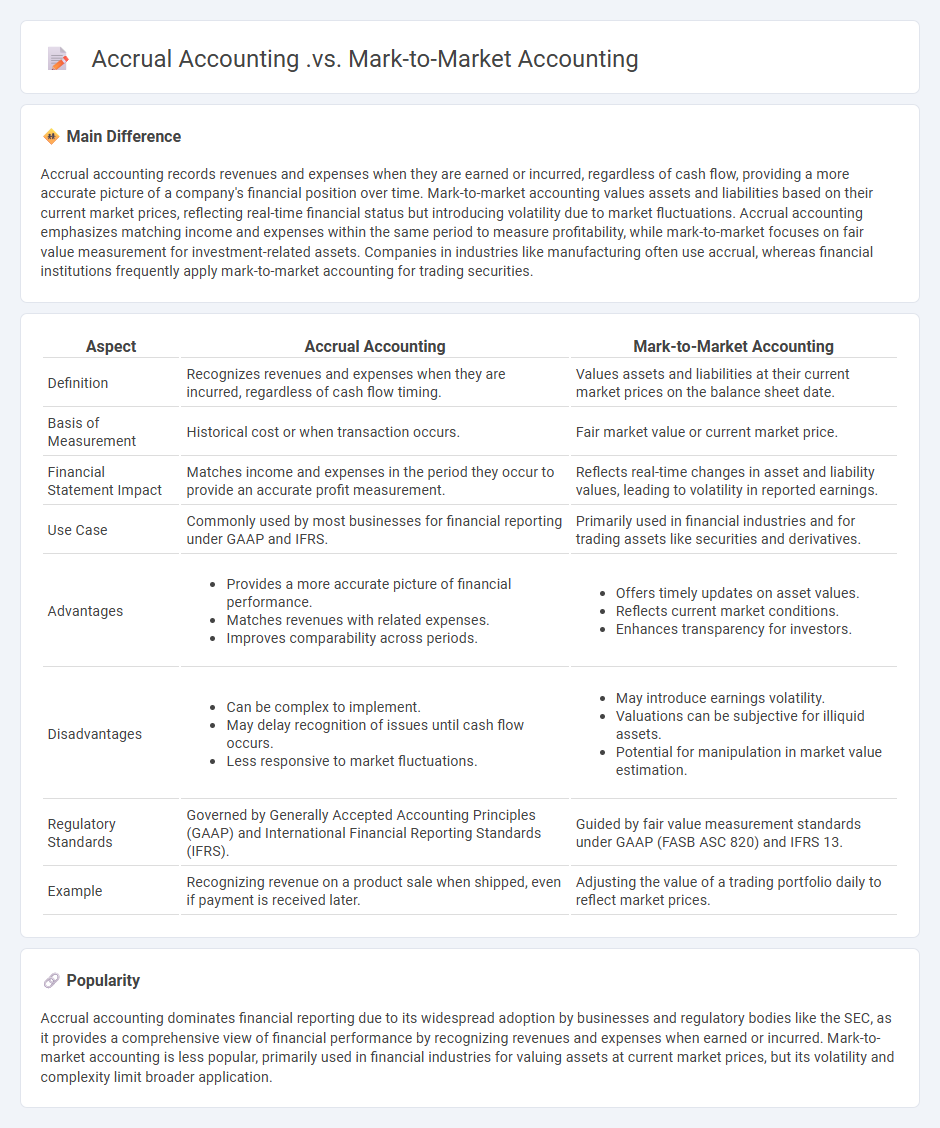

Main Difference

Accrual accounting records revenues and expenses when they are earned or incurred, regardless of cash flow, providing a more accurate picture of a company's financial position over time. Mark-to-market accounting values assets and liabilities based on their current market prices, reflecting real-time financial status but introducing volatility due to market fluctuations. Accrual accounting emphasizes matching income and expenses within the same period to measure profitability, while mark-to-market focuses on fair value measurement for investment-related assets. Companies in industries like manufacturing often use accrual, whereas financial institutions frequently apply mark-to-market accounting for trading securities.

Connection

Accrual accounting records revenues and expenses when they are incurred, matching financial events to the period they relate to, while mark-to-market accounting values assets and liabilities based on current market prices, providing real-time financial status. Both methods enhance financial reporting accuracy by reflecting economic reality: accrual accounting ensures timing alignment, and mark-to-market captures fluctuating asset values. Their connection lies in improving transparency and relevancy in financial statements, supporting better decision-making for investors and regulators.

Comparison Table

| Aspect | Accrual Accounting | Mark-to-Market Accounting |

|---|---|---|

| Definition | Recognizes revenues and expenses when they are incurred, regardless of cash flow timing. | Values assets and liabilities at their current market prices on the balance sheet date. |

| Basis of Measurement | Historical cost or when transaction occurs. | Fair market value or current market price. |

| Financial Statement Impact | Matches income and expenses in the period they occur to provide an accurate profit measurement. | Reflects real-time changes in asset and liability values, leading to volatility in reported earnings. |

| Use Case | Commonly used by most businesses for financial reporting under GAAP and IFRS. | Primarily used in financial industries and for trading assets like securities and derivatives. |

| Advantages |

|

|

| Disadvantages |

|

|

| Regulatory Standards | Governed by Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS). | Guided by fair value measurement standards under GAAP (FASB ASC 820) and IFRS 13. |

| Example | Recognizing revenue on a product sale when shipped, even if payment is received later. | Adjusting the value of a trading portfolio daily to reflect market prices. |

Revenue Recognition

Revenue recognition in finance involves recording income when it is earned and realizable, aligning with the accounting standards like IFRS 15 and ASC 606. Companies recognize revenue based on the transfer of control of goods or services to customers, ensuring accurate financial reporting and compliance. Timely and precise revenue recognition impacts financial statements, influencing investor decisions and regulatory assessments. Advanced ERP systems and automated accounting software enhance accuracy and efficiency in revenue recognition processes.

Fair Value Measurement

Fair value measurement in finance refers to the process of estimating the price at which an asset or liability could be exchanged between knowledgeable, willing parties in an orderly transaction. This measurement is governed by standards such as the Financial Accounting Standards Board's (FASB) Accounting Standards Codification (ASC) Topic 820, which defines fair value and establishes a framework for measuring it. Fair value is determined using market-based inputs prioritized in a three-level hierarchy: Level 1 inputs are quoted prices in active markets, Level 2 inputs include observable data such as quoted prices for similar assets, and Level 3 inputs rely on unobservable data using valuation techniques. Accurate fair value measurement enhances financial reporting transparency and supports investor decision-making.

Matching Principle

The Matching Principle in finance mandates that expenses be recorded in the same period as the revenues they help generate, ensuring accurate profit measurement. This accrual accounting concept aligns costs with related income, providing a clearer picture of financial performance. It is essential for preparing financial statements that comply with Generally Accepted Accounting Principles (GAAP). Companies use this principle to enhance the reliability and consistency of their financial reports.

Realized vs. Unrealized Gains

Realized gains occur when an asset is sold for a profit, locking in the financial benefit and triggering a taxable event based on capital gains tax rates. Unrealized gains represent the increase in value of an investment still held, reflecting potential profit without tax implications until the asset is sold. Investors track unrealized gains to assess portfolio performance but must focus on realized gains to understand actual cash flow and tax liabilities. Accurate differentiation between realized and unrealized gains is essential for effective financial planning and compliance with tax regulations.

Period-End Adjustments

Period-end adjustments ensure financial statements accurately reflect an organization's financial position by recording accrued expenses, prepaid revenues, depreciation, and inventory changes. These adjustments comply with Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) to match revenues and expenses to the correct accounting period. Common examples include adjusting entries for accrued salaries, utilities, and unearned revenues recognized during the period. Accurate period-end adjustments enhance financial analysis, decision-making, and regulatory compliance in accounting and finance.

Source and External Links

Mark-to-market accounting - Mark-to-market accounting values assets or liabilities based on current market prices, reflecting real-time value changes, whereas accrual accounting records revenues and expenses when they are earned or incurred, not necessarily when cash changes hands.

Making Sense of Mark to Market - Accrual accounting typically uses historical cost (contractual values) while mark-to-market (fair value) accounting reflects current market prices, capturing interest rate and credit risks in asset valuations.

Understanding Accrual, MTM and Yield Curve - Accrual accounting recognizes income as it accrues over time, whereas mark-to-market accounting updates asset values to current market prices periodically, affecting reported net asset values.

FAQs

What is accrual accounting?

Accrual accounting is a financial reporting method where revenues and expenses are recorded when they are earned or incurred, regardless of when cash is exchanged.

What is mark-to-market accounting?

Mark-to-market accounting is a financial method that records the value of assets and liabilities at their current market price rather than at historical cost.

How do accrual accounting and mark-to-market accounting differ?

Accrual accounting records revenues and expenses when they are earned or incurred regardless of cash flow, while mark-to-market accounting values assets and liabilities at their current market prices to reflect real-time financial status.

What are the main benefits of accrual accounting?

Accrual accounting improves financial accuracy by recognizing revenues and expenses when they occur, enhances decision-making through timely financial information, ensures compliance with accounting standards, and provides a clearer picture of a company's financial health.

What are the main benefits of mark-to-market accounting?

Mark-to-market accounting provides real-time asset valuation, enhances financial transparency, improves risk management, and ensures timely reflection of market conditions in financial statements.

When is accrual accounting preferred over mark-to-market accounting?

Accrual accounting is preferred over mark-to-market accounting when recognizing revenues and expenses that are earned or incurred but not yet realized in cash, such as in long-term contracts, subscription services, or when matching costs to the period they generate revenue.

What industries commonly use mark-to-market accounting?

The finance, banking, insurance, and investment management industries commonly use mark-to-market accounting.