The Modigliani-Miller Theorem establishes that under perfect market conditions, a firm's value is unaffected by its capital structure, emphasizing the irrelevance of debt or equity financing. In contrast, the Pecking Order Theory suggests that companies prioritize financing sources based on asymmetric information, preferring internal funds, then debt, and finally equity as a last resort. Explore deeper to understand how these fundamental financial theories influence capital structure decisions in real-world markets.

Main Difference

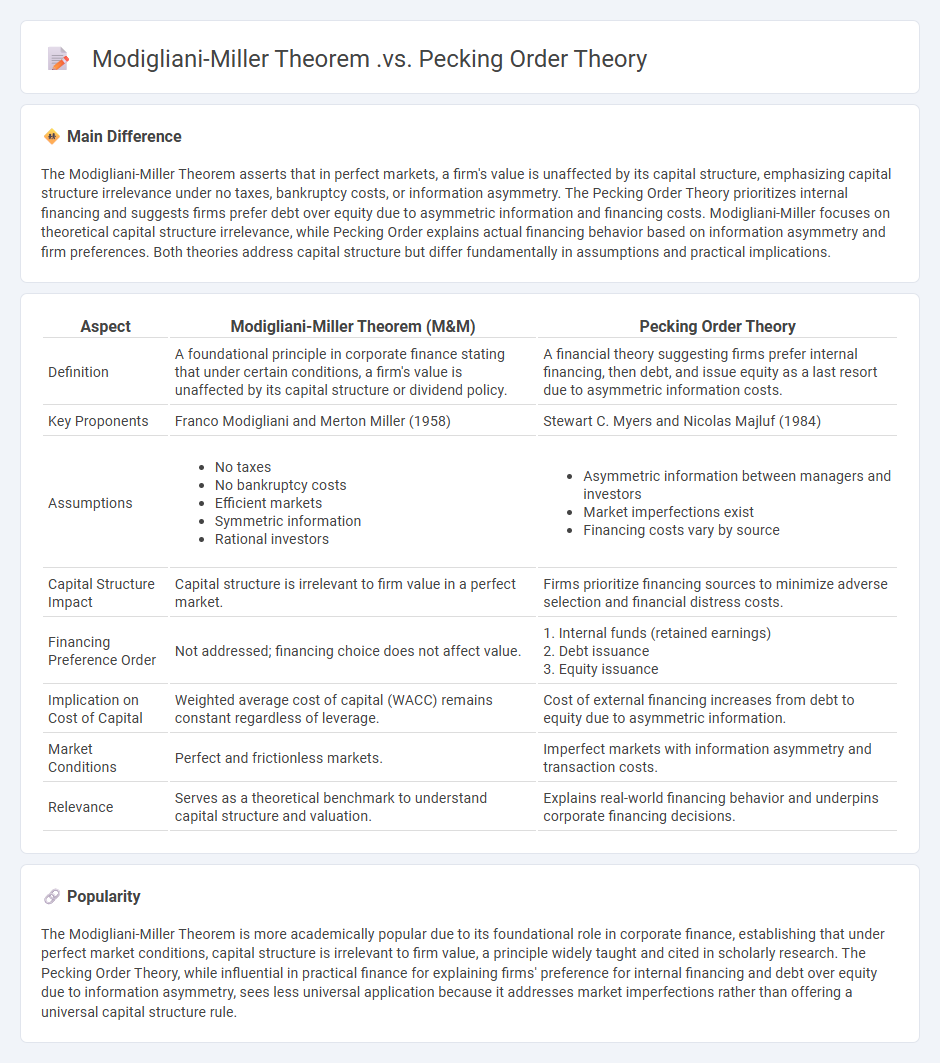

The Modigliani-Miller Theorem asserts that in perfect markets, a firm's value is unaffected by its capital structure, emphasizing capital structure irrelevance under no taxes, bankruptcy costs, or information asymmetry. The Pecking Order Theory prioritizes internal financing and suggests firms prefer debt over equity due to asymmetric information and financing costs. Modigliani-Miller focuses on theoretical capital structure irrelevance, while Pecking Order explains actual financing behavior based on information asymmetry and firm preferences. Both theories address capital structure but differ fundamentally in assumptions and practical implications.

Connection

The Modigliani-Miller Theorem establishes that under perfect market conditions, a firm's capital structure does not affect its value, emphasizing the irrelevance of financing decisions. Pecking Order Theory, contrastingly, explains real-world deviations by suggesting firms prioritize internal financing, then debt, and issue equity as a last resort due to asymmetric information and transaction costs. The connection lies in Pecking Order Theory addressing practical limitations ignored by Modigliani-Miller, bridging theoretical capital structure irrelevance with observed financing behavior.

Comparison Table

| Aspect | Modigliani-Miller Theorem (M&M) | Pecking Order Theory |

|---|---|---|

| Definition | A foundational principle in corporate finance stating that under certain conditions, a firm's value is unaffected by its capital structure or dividend policy. | A financial theory suggesting firms prefer internal financing, then debt, and issue equity as a last resort due to asymmetric information costs. |

| Key Proponents | Franco Modigliani and Merton Miller (1958) | Stewart C. Myers and Nicolas Majluf (1984) |

| Assumptions |

|

|

| Capital Structure Impact | Capital structure is irrelevant to firm value in a perfect market. | Firms prioritize financing sources to minimize adverse selection and financial distress costs. |

| Financing Preference Order | Not addressed; financing choice does not affect value. |

1. Internal funds (retained earnings) 2. Debt issuance 3. Equity issuance |

| Implication on Cost of Capital | Weighted average cost of capital (WACC) remains constant regardless of leverage. | Cost of external financing increases from debt to equity due to asymmetric information. |

| Market Conditions | Perfect and frictionless markets. | Imperfect markets with information asymmetry and transaction costs. |

| Relevance | Serves as a theoretical benchmark to understand capital structure and valuation. | Explains real-world financing behavior and underpins corporate financing decisions. |

Capital Structure Irrelevance

Capital structure irrelevance, formulated by Modigliani and Miller in 1958, asserts that a firm's value is unaffected by its financing mix of debt and equity under perfect market conditions. This theory assumes no taxes, bankruptcy costs, or asymmetric information, implying that leverage does not impact the overall cost of capital. Empirical evidence shows deviations in real markets where tax shields on debt and agency costs influence firm valuation. The Modigliani-Miller theorem remains foundational in corporate finance for understanding financing decisions and market efficiency.

Information Asymmetry

Information asymmetry in finance occurs when one party in a financial transaction possesses more or better information than the other, leading to imbalanced decision-making and potential market inefficiencies. It frequently impacts stock markets, where insiders may have knowledge of corporate earnings or mergers unavailable to general investors, influencing stock prices and trading behavior. This phenomenon contributes to adverse selection and moral hazard problems in lending and insurance markets, increasing risks and costs for lenders and underwriters. Regulatory frameworks like the Securities Act and disclosure requirements aim to reduce information asymmetry by promoting transparency and equal access to financial information.

Debt vs Equity Financing

Debt financing involves borrowing funds that must be repaid with interest, often through loans or bonds, providing businesses with capital while maintaining ownership control. Equity financing entails raising capital by selling shares of the company, diluting ownership but avoiding repayment obligations and interest expenses. Companies weigh debt-to-equity ratios to balance risk and return, with debt offering tax advantages through interest deductions, while equity reduces financial leverage and bankruptcy risk. Effective capital structure management optimizes cost of capital and supports sustainable growth in competitive financial markets.

Cost of Capital

Cost of capital represents the minimum return a company must earn on its investments to satisfy its investors and maintain its market value. It includes the cost of debt, calculated as the effective interest rate on borrowed funds, and the cost of equity, estimated using models like the Capital Asset Pricing Model (CAPM). Accurately determining the weighted average cost of capital (WACC) is essential for investment appraisal, capital budgeting, and financial decision-making. Firms with high risk typically face a higher cost of capital, affecting their ability to fund growth projects.

Signaling Effects

Signaling effects in finance describe how a company's financial decisions convey information to investors beyond the raw data presented in financial statements. For example, issuing debt signals management's confidence in future cash flows, as creditors require solid repayment assurance. Dividend announcements often serve as positive signals, indicating stable earnings and financial health, influencing stock prices accordingly. Empirical studies, such as those by Ross (1977), highlight the importance of signaling in capital structure decisions and market perceptions.

Source and External Links

Here are three links with brief descriptions comparing the Modigliani-Miller Theorem and the Pecking Order Theory:M&M Theorem - Overview, Assumptions, Propositions - This page provides an overview of the Modigliani-Miller theorem, which suggests that capital structure does not affect a company's value in efficient markets.

Pecking Order Theory - This theory proposes that firms prioritize internal financing over external financing, starting with debt and then equity, which contrasts with the Modigliani-Miller approach.

Optimum Capital Structure - This article discusses various capital structure theories, including the Pecking Order Theory and Modigliani-Miller theorem, highlighting their differences in explaining how companies choose financing options.

FAQs

What is the Modigliani-Miller Theorem?

The Modigliani-Miller Theorem states that in a perfect market without taxes, bankruptcy costs, or asymmetric information, a firm's value is unaffected by its capital structure, meaning the mix of debt and equity does not influence its overall market value.

What is the Pecking Order Theory?

The Pecking Order Theory is a corporate finance principle stating firms prioritize internal financing first, debt second, and equity issuance last to minimize asymmetric information costs.

How do the Modigliani-Miller Theorem and Pecking Order Theory differ in capital structure explanation?

The Modigliani-Miller Theorem states capital structure is irrelevant to firm value under perfect market conditions, while the Pecking Order Theory explains firms prioritize internal financing, then debt, and lastly equity due to asymmetric information and financing costs.

What are the key assumptions of the Modigliani-Miller Theorem?

The Modigliani-Miller Theorem assumes no taxes, no bankruptcy costs, symmetric information, efficient markets, and no transaction costs.

What are the main predictions of the Pecking Order Theory?

The Pecking Order Theory predicts that firms prioritize internal financing first, debt second, and equity issuance last due to asymmetric information and cost differences.

How do market imperfections impact both theories?

Market imperfections cause deviations in supply and demand curves, leading to inefficiencies in both classical and neoclassical economic theories by preventing optimal resource allocation and price equilibrium.

Which theory better explains real-world corporate financing decisions?

The Trade-Off Theory better explains real-world corporate financing decisions by balancing the benefits of debt tax shields with the costs of financial distress.