The Capital Asset Pricing Model (CAPM) explains asset returns based on market risk represented by beta, emphasizing a single systematic factor. Arbitrage Pricing Theory (APT) expands this view by incorporating multiple macroeconomic factors to determine expected returns, allowing for a more flexible risk assessment. Explore the key differences and practical applications of CAPM and APT for improved investment decisions.

Main Difference

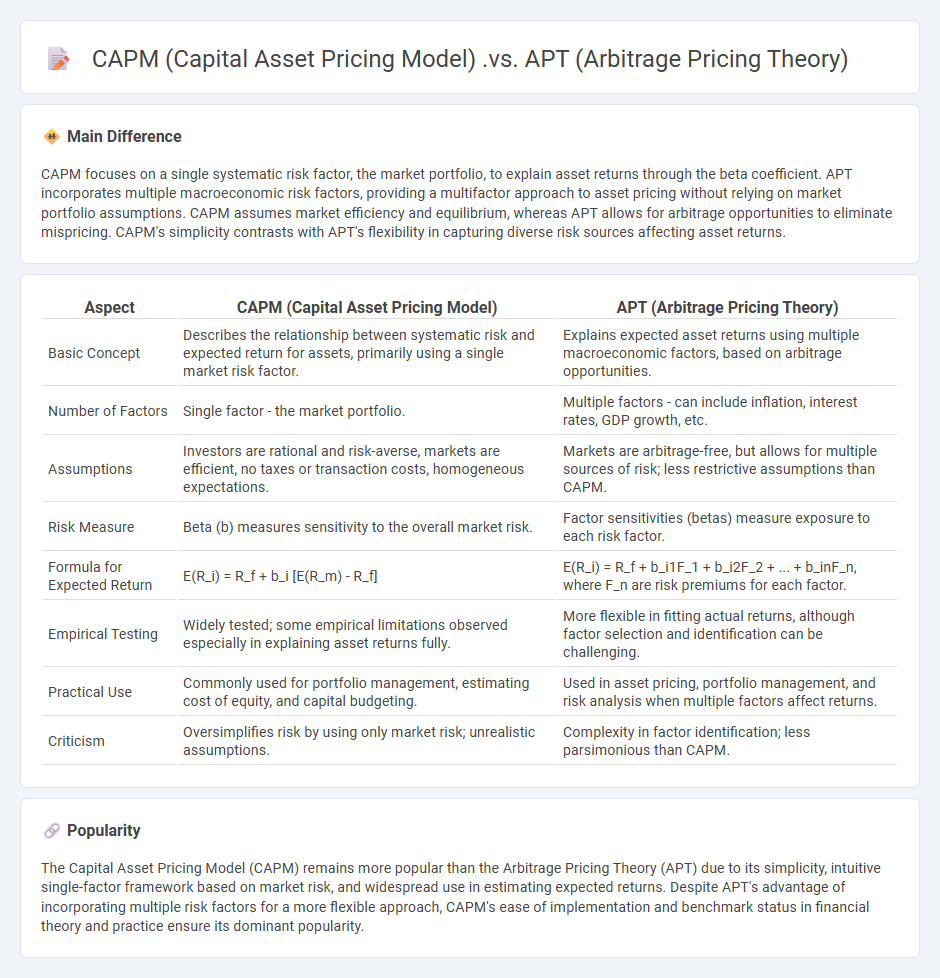

CAPM focuses on a single systematic risk factor, the market portfolio, to explain asset returns through the beta coefficient. APT incorporates multiple macroeconomic risk factors, providing a multifactor approach to asset pricing without relying on market portfolio assumptions. CAPM assumes market efficiency and equilibrium, whereas APT allows for arbitrage opportunities to eliminate mispricing. CAPM's simplicity contrasts with APT's flexibility in capturing diverse risk sources affecting asset returns.

Connection

CAPM (Capital Asset Pricing Model) and APT (Arbitrage Pricing Theory) are connected through their common goal of explaining asset returns based on risk factors. CAPM relies on a single market risk factor, using beta to measure an asset's sensitivity to market movements and determine expected returns. In contrast, APT extends this framework by incorporating multiple macroeconomic factors, offering a more flexible multi-factor model that captures diverse sources of systematic risk beyond the market portfolio.

Comparison Table

| Aspect | CAPM (Capital Asset Pricing Model) | APT (Arbitrage Pricing Theory) |

|---|---|---|

| Basic Concept | Describes the relationship between systematic risk and expected return for assets, primarily using a single market risk factor. | Explains expected asset returns using multiple macroeconomic factors, based on arbitrage opportunities. |

| Number of Factors | Single factor - the market portfolio. | Multiple factors - can include inflation, interest rates, GDP growth, etc. |

| Assumptions | Investors are rational and risk-averse, markets are efficient, no taxes or transaction costs, homogeneous expectations. | Markets are arbitrage-free, but allows for multiple sources of risk; less restrictive assumptions than CAPM. |

| Risk Measure | Beta (b) measures sensitivity to the overall market risk. | Factor sensitivities (betas) measure exposure to each risk factor. |

| Formula for Expected Return | E(R_i) = R_f + b_i [E(R_m) - R_f] | E(R_i) = R_f + b_i1F_1 + b_i2F_2 + ... + b_inF_n, where F_n are risk premiums for each factor. |

| Empirical Testing | Widely tested; some empirical limitations observed especially in explaining asset returns fully. | More flexible in fitting actual returns, although factor selection and identification can be challenging. |

| Practical Use | Commonly used for portfolio management, estimating cost of equity, and capital budgeting. | Used in asset pricing, portfolio management, and risk analysis when multiple factors affect returns. |

| Criticism | Oversimplifies risk by using only market risk; unrealistic assumptions. | Complexity in factor identification; less parsimonious than CAPM. |

Systematic Risk

Systematic risk refers to the inherent market risk that affects the entire financial system or a large segment of the market, making it unavoidable through diversification. Factors contributing to systematic risk include economic recessions, political instability, interest rate fluctuations, and natural disasters. The Capital Asset Pricing Model (CAPM) quantifies this risk through beta, measuring a security's sensitivity to overall market movements. Investors manage systematic risk primarily through asset allocation strategies and hedging techniques rather than relying solely on diversification.

Single-Factor Model

The Single-Factor Model in finance explains asset returns by relating them to a single common factor, typically the market return. This model underpins the Capital Asset Pricing Model (CAPM), where the key factor is the market portfolio's excess return over the risk-free rate. Empirical studies demonstrate that beta, the sensitivity coefficient, measures systematic risk and helps estimate the expected return of securities. It simplifies portfolio management by focusing on market risk rather than multiple sources of uncertainty.

Multi-Factor Model

The Multi-Factor Model in finance quantifies asset returns by incorporating multiple risk factors beyond the market index, such as size, value, momentum, and volatility. It improves portfolio diversification and risk assessment by explaining variations in asset prices through systematic influences. Prominent examples include the Fama-French Three-Factor Model, which adds size and value factors to the Capital Asset Pricing Model (CAPM). Utilizing these models enhances investment strategies by more accurately capturing sources of expected returns and risks.

Risk Premium

Risk premium in finance represents the expected return above the risk-free rate that investors demand for taking on higher risk investments, such as stocks or corporate bonds. It compensates investors for the uncertainty and potential volatility compared to guaranteed returns from government securities like U.S. Treasury bonds. The size of the risk premium varies across asset classes, industries, and individual securities depending on perceived risk factors including market volatility, credit risk, and economic conditions. Historical data shows average equity risk premiums in U.S. markets range from 4% to 7% annually, reflecting the additional reward investors seek for bearing systematic risk.

Arbitrage Opportunity

Arbitrage opportunity in finance refers to the chance to profit from price differences of identical or similar financial instruments across different markets or exchanges. Traders exploit these inefficiencies by simultaneously buying low in one market and selling high in another, ensuring risk-free gains. The efficient market hypothesis posits that such opportunities are rare and short-lived as market forces quickly correct price discrepancies. High-frequency trading firms and algorithmic systems are primarily responsible for identifying and executing arbitrage strategies in modern financial markets.

Source and External Links

Describe The Differences Between CAPM and APT | PDF - CAPM explains expected returns based solely on market risk as a single factor, while APT uses multiple macroeconomic risk factors, making APT more flexible and practical for pricing single assets compared to CAPM which is suited for portfolios.

Arbitrage Pricing Theory - Defintion, Formula, Example - APT is a multifactor asset pricing model that allows for the expected return of an asset to depend linearly on various macroeconomic factors, whereas CAPM bases expected returns only on market risk, making APT a more complex but customizable alternative to CAPM.

Analysis and Comparison of Capital Asset Pricing Model ... - CAPM relies on strict assumptions including a frictionless market and a single investment period with all investors sharing consensus expectations; APT relaxes these assumptions, requires fewer market participants to eliminate arbitrage, and allows for multiple risk factors.