Delta hedging focuses on neutralizing the directional risk of an option position by offsetting changes in the underlying asset's price, maintaining a delta close to zero. Gamma hedging manages the curvature risk by stabilizing the delta exposure against large price movements, ensuring more precise protection in volatile markets. Explore the detailed dynamics and strategies behind Delta and Gamma hedging to enhance your options trading risk management.

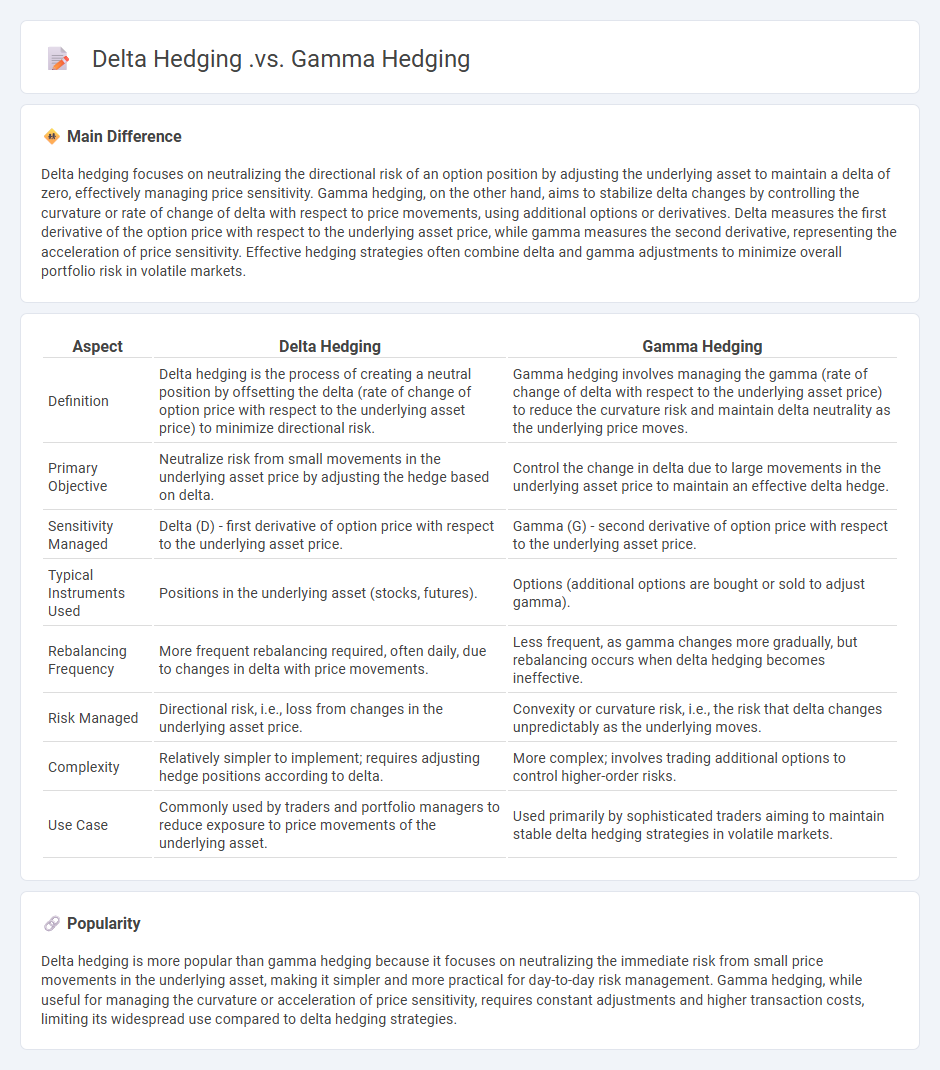

Main Difference

Delta hedging focuses on neutralizing the directional risk of an option position by adjusting the underlying asset to maintain a delta of zero, effectively managing price sensitivity. Gamma hedging, on the other hand, aims to stabilize delta changes by controlling the curvature or rate of change of delta with respect to price movements, using additional options or derivatives. Delta measures the first derivative of the option price with respect to the underlying asset price, while gamma measures the second derivative, representing the acceleration of price sensitivity. Effective hedging strategies often combine delta and gamma adjustments to minimize overall portfolio risk in volatile markets.

Connection

Delta hedging and gamma hedging are interrelated risk management strategies used in options trading to protect against price movements of the underlying asset. Delta hedging focuses on neutralizing the portfolio's sensitivity to small price changes by adjusting positions to maintain a delta close to zero, while gamma hedging targets the rate of change of delta, managing the curvature of the option's value in response to underlying price fluctuations. Effective gamma hedging supports delta hedging by stabilizing delta over time, reducing the frequency of rebalancing needed to maintain a delta-neutral position.

Comparison Table

| Aspect | Delta Hedging | Gamma Hedging |

|---|---|---|

| Definition | Delta hedging is the process of creating a neutral position by offsetting the delta (rate of change of option price with respect to the underlying asset price) to minimize directional risk. | Gamma hedging involves managing the gamma (rate of change of delta with respect to the underlying asset price) to reduce the curvature risk and maintain delta neutrality as the underlying price moves. |

| Primary Objective | Neutralize risk from small movements in the underlying asset price by adjusting the hedge based on delta. | Control the change in delta due to large movements in the underlying asset price to maintain an effective delta hedge. |

| Sensitivity Managed | Delta (D) - first derivative of option price with respect to the underlying asset price. | Gamma (G) - second derivative of option price with respect to the underlying asset price. |

| Typical Instruments Used | Positions in the underlying asset (stocks, futures). | Options (additional options are bought or sold to adjust gamma). |

| Rebalancing Frequency | More frequent rebalancing required, often daily, due to changes in delta with price movements. | Less frequent, as gamma changes more gradually, but rebalancing occurs when delta hedging becomes ineffective. |

| Risk Managed | Directional risk, i.e., loss from changes in the underlying asset price. | Convexity or curvature risk, i.e., the risk that delta changes unpredictably as the underlying moves. |

| Complexity | Relatively simpler to implement; requires adjusting hedge positions according to delta. | More complex; involves trading additional options to control higher-order risks. |

| Use Case | Commonly used by traders and portfolio managers to reduce exposure to price movements of the underlying asset. | Used primarily by sophisticated traders aiming to maintain stable delta hedging strategies in volatile markets. |

Delta Neutral

Delta neutral strategy in finance involves constructing a portfolio where the overall delta, or sensitivity to price changes of the underlying asset, is zero. Traders use options and underlying securities to hedge against price movements, aiming to minimize directional risk. This approach is common in options trading, allowing investors to profit from volatility or time decay rather than price fluctuations. The effectiveness of a delta neutral position depends on continuous adjustments known as rebalancing or hedging.

Gamma Exposure

Gamma exposure measures the sensitivity of an option's delta to changes in the underlying asset's price, crucial for portfolio risk management in finance. It quantifies the rate of change of delta, enabling traders to assess how their option positions will react to price volatility in assets like stocks, indexes, or commodities. High gamma exposure implies rapid shifts in delta, requiring active hedging to mitigate potential losses from sudden market movements. Professional options traders and risk managers utilize gamma exposure metrics to optimize hedging strategies and maintain balanced portfolios.

Option Sensitivity

Option sensitivity measures how the price of an option changes in response to various factors such as the underlying asset's price, volatility, time decay, and interest rates. Key sensitivities include Delta, which indicates the rate of change of the option price relative to the underlying asset price, and Vega, which measures sensitivity to volatility changes. Gamma quantifies the rate of change in Delta, while Theta represents the time decay or the option's value erosion as expiration approaches. Rho measures sensitivity to interest rate fluctuations, making these Greeks essential for risk management and option pricing in financial markets.

Portfolio Adjustment

Portfolio adjustment involves the strategic reallocation of assets within an investment portfolio to optimize returns and manage risk according to market conditions and investor objectives. This process may include buying, selling, or substituting securities such as stocks, bonds, and ETFs to maintain a desired asset allocation or capitalize on emerging opportunities. Portfolio adjustment is essential for responding to changes in economic indicators, interest rates, and geopolitical events that affect asset valuations. Consistent monitoring and timely adjustments enhance portfolio performance and help achieve long-term financial goals.

Risk Mitigation

Risk mitigation in finance involves identifying, assessing, and prioritizing potential financial threats to minimize their impact on investments and operations. Strategies include diversification, hedging with derivatives, and maintaining sufficient liquidity to absorb losses. Regulatory compliance and rigorous credit analysis also play critical roles in reducing exposure to market volatility and credit defaults. Effective risk mitigation enhances portfolio stability, protects capital, and supports sustainable financial growth.

Source and External Links

## Set 1Delta-Gamma Hedging: A 2025 Guide for Advanced Traders - This article discusses delta and gamma hedging as distinct strategies in options trading, with delta hedging suitable for stable markets and gamma hedging for volatile conditions.

## Set 2Greeks - Gamma: a crucial measure to rebalance delta - This article highlights gamma as a crucial measure for rebalancing delta hedges, emphasizing its role in managing the rate of change of delta in relation to the underlying asset.

## Set 3Delta Hedging vs Gamma Hedging - This webpage provides a comparison of delta and gamma hedging, noting that delta hedging neutralizes directional risk, while gamma hedging addresses the rate of change in delta for comprehensive protection.

FAQs

What is delta hedging in trading?

Delta hedging in trading is a risk management strategy that involves adjusting the positions in underlying assets to offset the delta exposure of options, thereby maintaining a neutral market risk stance.

What is gamma hedging and how does it work?

Gamma hedging is a risk management strategy that adjusts a portfolio's exposure to the gamma of options to maintain a stable delta, minimizing the risk from large price movements in the underlying asset.

How does delta hedging differ from gamma hedging?

Delta hedging manages portfolio risk by offsetting changes in an asset's price to maintain a neutral delta, while gamma hedging manages risk related to changes in delta itself by stabilizing the portfolio's gamma exposure.

Why is gamma important for option traders?

Gamma is important for option traders because it measures the rate of change of an option's delta, helping them assess how the option's price sensitivity to the underlying asset's price will evolve, enabling more precise risk management and hedging strategies.

When should you use delta hedging versus gamma hedging?

Use delta hedging to neutralize the first-order price risk from small asset price changes; use gamma hedging to manage the curvature risk by stabilizing delta against larger price movements.

What are the risks of only using delta hedging?

Delta hedging risks include exposure to gamma risk, where large price movements can cause significant hedging errors, increased transaction costs due to frequent rebalancing, vulnerability to volatility changes impacting the option's value, and potential liquidity constraints limiting timely adjustments.

How do delta and gamma interact in a hedge portfolio?

Delta measures the portfolio's sensitivity to small changes in the underlying asset's price, while gamma indicates the rate of change of delta with respect to the underlying price; a hedge portfolio uses gamma to adjust delta dynamically, maintaining effective hedging as the asset price moves.